Nội dung toàn văn Official Dispatch No. 4023/TCT-TNCN 2014 exemption of taxes incurred by foreign experts participating in ODA projects

MINISTRY OF FINANCE | SOCIALIST REPUBLIC OF VIETNAM |

No. 4023/TCT-TNCN | Hanoi, September 17, 2014 |

To: Department of Taxation of Vinh Phuc province

In response to Dispatch No. 3390/CT-TNCN dated June 24, 2014 and dispatch No. 3663/CT-TNCN dated July 02, 2014 of Department of Taxation of Vinh Phuc province requesting guidance on requirements for exemption of taxes incurred by experts participating in ODA projects in Vietnam:

1. With regard to effective periods of the contract used as the basis for determination of entities regulated by Decision No. 119/2009/QĐ-TTg

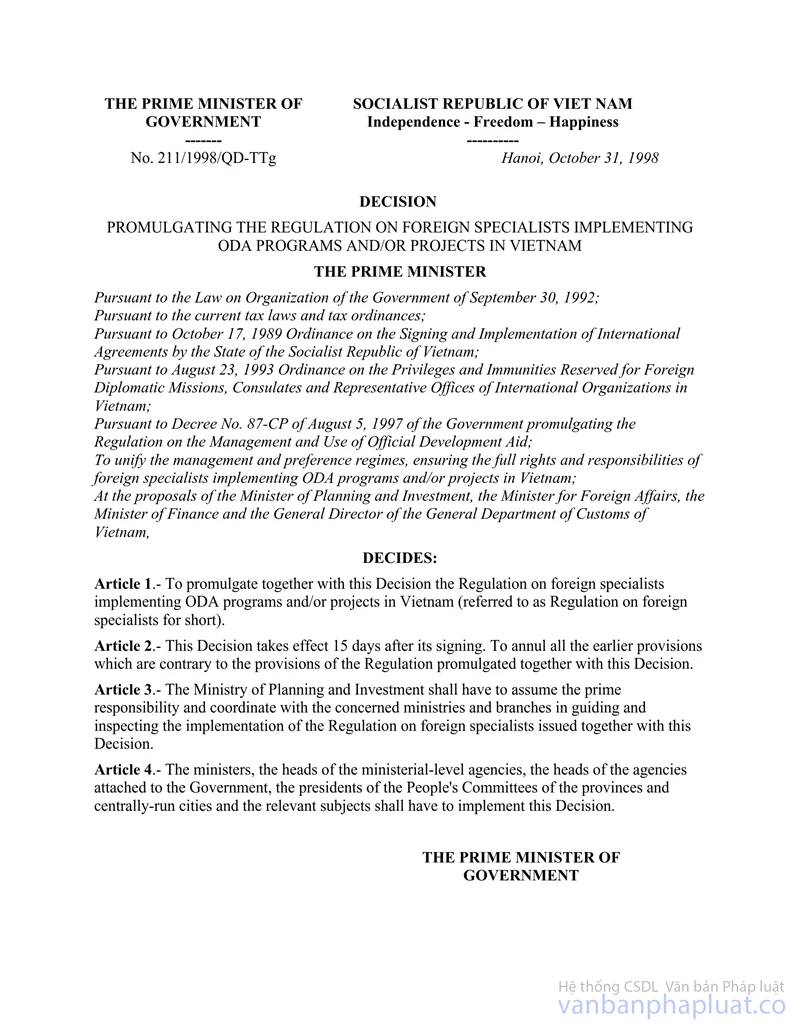

- Article 2 of the Prime Minister’s Decision No. 119/2009/QĐ-TTg dated October 01, 2009 promulgating Regulation on foreign experts participating in ODA projects prescribes that:

“This Decision takes effect on November 20, 2009".

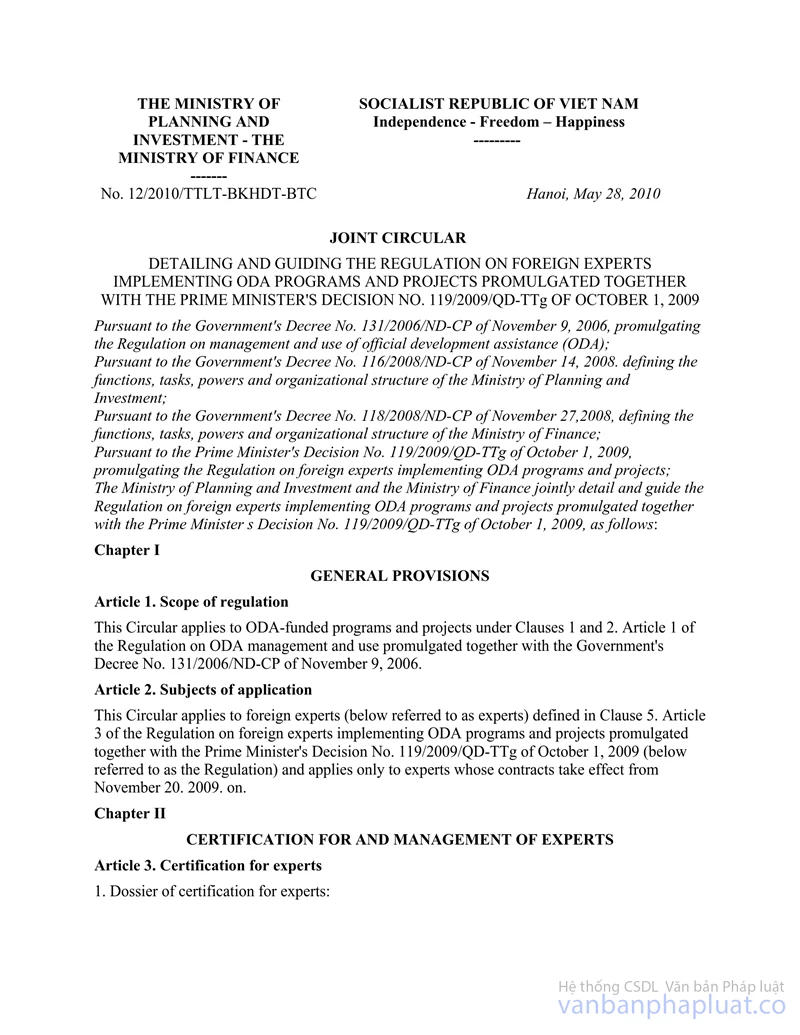

- Article 2 of Circular No. 12/2010/TTLT-BKHĐT-BTC dated May 28, 2010 of the Ministry of Planning and Investment and the Ministry of Finance on guidelines for implementation of Regulation on foreign experts participating in ODA projects prescribes that:

“Article 2. Regulated entities

... only applies to the experts whose contracts take effect from November 20, 2009”

- Article 3 of Circular No. 12/2010/TTLT-BKHĐT-BTC dated May 28, 2010 of the Ministry of Planning and Investment and the Ministry of Finance prescribes that:

“1. Experts profiles:

…

- A copy of the consultancy contract (of an individual expert or group of experts) with the contractor, a Vietnamese authority or foreign authority”.

The documents do not clarify that “their contracts” and “consultancy contracts” in the experts’ profiles include both the Contractor’s consultancy contracts and the consultancy contracts between the experts and the Contractor. Thus, the Ministry of Planning and Investment has issued Dispatch No. 8712/BKH-KTĐN dated December 06, 2010 providing guidance on requirements for tax incentives for foreign experts participating in ODA projects in Vietnam. Pursuant to the guidance provided by the Ministry of Planning and Investment, the Ministry of Finance has issued Dispatch No. 144/BTC-TCT dated January 06, 2011 providing guidance on contracts with foreign experts participating in ODA projects in Vietnam prescribes that: (1) of 144/BTC-TCT prescribes that:

“1. With regard to contracts of experts participating in ODA projects that take effect from November 20, 2009 according to Article 2 of Circular No. 12/2010/TTLT-BKHĐT-BTC dated May 28, 2010:

- The foreign party and the Vietnamese party signs a consultancy contract with the individual expert or group of experts, which enclosed with a decision to approve the result of bidding for consulting services;

- The foreign party and the Vietnamese party signs a contract with the contractor (company), the bidding documents of which enumerate the expert as a counselor, enclosed with the bidding documents approved by a competent authority (including the list of counselors);

- The consultancy contract between the expert and the contractor (company): in this case, if the contractor (company) appoints an expert of the contractor (company) on the list of bidders instead of signing a contract with the expert, the replacement of the contract with the decision on appointment is regulated by the Circular No. 12/2010/TTLT-BKHĐT-BTC dated May 28, 2010.

Pursuant to the aforementioned regulations, the effective date November 20, 2009 is applied to both the consultancy contract between the contractor and the competent authority, and the consultancy contract between the foreign expert and the contractor. Where the contractor appoints a foreign expert on the list of bidders instead of signing a contract with the foreign expert, the contract shall be replaced with a decision on appointment.

2. Addition of experts after November 20, 2009

- Point 2 of Dispatch No. 144/BTC-TCT dated January 06, 2011 of the Ministry of Finance providing guidance on contracts with foreign experts participating in ODA projects prescribes that:

“2. The replacement and addition of experts after November 20, 2009 with regard to consultancy contracts that take effect before November 20, 2009.

...Where the contractor (company) replaces or adds experts after November 20, 2009 with regard to the consultancy contracts that take effect before November 20, 2009, the new experts shall replace the old ones. The new experts must satisfy the criteria in the bidding documents, and such replacement must be approved by a competent authority. If the new experts are eligible for incentives according to Decision No. 211/1998/QĐ-TTg dated October 31, 1998, they shall be eligible for the incentives in Decision No. 119/2009/QĐ-TTg”

The addition of experts mentioned in (2) of Dispatch No. 144/BTC-TCT is applied when new foreign experts are replaced or added for consultancy contracts that take effect before November 20, provided the criteria in bidding documents of the contractor (company) are satisfied, and such replacement is approved by a competent authority. There are no instructions on replacement and addition of foreign experts from November 20, 2009. As a result, the Ministry of Planning and Investment has issued the Dispatch No. 2138/BKHĐT-KTĐN dated April 10, 2014, which prescribes that: “...Additional experts of the additional contract (as in the case of the representative office of Nippon Koei) shall be eligible for personal income tax incentives due to the addition, provided the addition is approved by a competent authority.”

Pursuant to the guidance of the Ministry of Planning and Investment, the Ministry of Finance send the Dispatch No. 7313/BTC-TCT dated June, 02, 2014 to representative office of Nippon Koei in Hanoi, which approves the effective date before November 20, 2009 of the consultancy contract of the contractor. If any appendix to the original contract is made to add new tasks, the tax exemption for additional foreign experts shall be considered as if the contracts take effect from November 20, 2009.

Similar cases shall be handled in accordance with Dispatch No. 2138/BKHĐT-KTĐN dated April 10, 2014 of the Ministry of Planning and Investment.

Pursuant to the aforementioned regulations, since the consultancy between the contractor Nippon Koei – Poyry Infra takes effect before November 20, 2009, the exemption of personal income tax incurred by their foreign experts shall be considered as follows:

- The foreign experts on the list of bidders of the consultancy contract which takes effect before November 20, 2009 are not regulated by the Prime Minister’s Decision No. 119/2009/QĐ-TTg dated October, 01, 2009.

- The new experts added after November 20, 2009 to the consultancy contract that takes effect before November 20, 2009 shall be provided with incentives if they are eligible as prescribed in Decision No. 119/2009/QĐ-TTg.

- The new experts added from November 20, 2009 to the consultancy contract that takes effect from November 20, 2009 shall be eligible for incentives under Decision No. 119/2009/QĐ-TTg if such foreign experts are approved by a competent authority.

Provincial Departments of Taxation shall provide guidance on exemption of taxes incurred by foreign experts participating in ODA projects in Vietnam in accordance with effective regulations and guidance in this Dispatch.

Department of Taxation of Vinh Phuc province is responsible for the implementation of this Dispatch./.

| PP DIRECTOR OF PERSONAL INCOME TAX ADMINISTRATION |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and for reference purposes only. Its copyright is owned by LawSoft and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed