Nội dung toàn văn Circular No. 06/2010/TT-BTC of January 13, 2010, guiding the determination of turnover for calculation of enterprise income tax on the sale of golf play tickets or golf course membership cards

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 06/2010/TT-BTC |

Hanoi, January 13, 2010 |

CIRCULAR

GUIDING THE DETERMINATION OF TURNOVER FOR CALCULATION OF ENTERPRISE INCOME TAX ON THE SALE OF GOLF PLAY TICKETS OR GOLF COURSE MEMBERSHIP CARDS

Pursuant to June 3, 2008 Law

No. 14/2008/ QH12 on Enterprise Income Tax and the Government's Decree No.

124/2008/ND-CP of December 11, 2008, detailing and guiding a number of articles

of the Law on Enterprise Income Tax;

Pursuant to the Government's Decree No. 118/2008/ND-CP of November 27, 2008,

defining the functions, tasks, powers and organizational structure of the

Ministry of Finance;

The Ministry of Finance additionally guides the determination of turnover for

calculation of enterprise income tax (EIT) on the sale of golf play tickets or

golf course membership cards as follows:

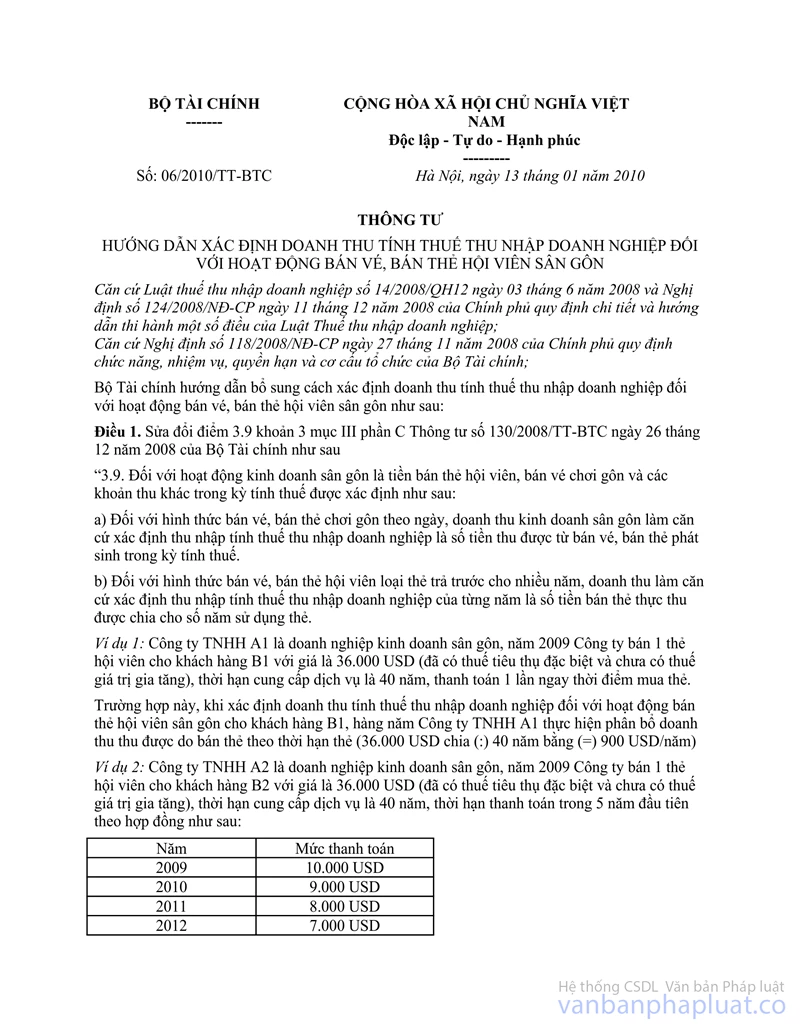

Article 1. To amend Point 3.9, Clause 3, Section III, Part C of the Finance Ministry's Circular No. 130/2008ATT-BTC of December 26, 2008, as follows:

"3.9. For golf course business, taxable turnover is revenues from the sale of membership cards and play tickets and other revenues earned in the tax period which is determined as follows:

a/ For the sale of daily golf play tickets or cards, the turnover from golf course business which is used as a basis for determining EIT calculation income is the revenue from the sale of tickets and cards earned in the tax period.

b/ For the sale of tickets or membership cards which are prepaid for several years, the turnover used as a basis for determining annual EIT calculation income is the outcome of the division between the revenue actually earned from the sale of cards and the number of years of card validity.

Example 1: Limited Liability Company Al is a golf course business enterprise. In 2009, the company sold one membership card to customer B1 at the price of USD 36,000 (inclusive of excise tax and exclusive of value-added tax), the service provision duration is 40 years and lump-sum payment is made right at the time of card purchase.

In this case, when determining turnover for calculation of enterprise income tax on the sale of the golf course membership card to customer B1, annually. Company Al shall divide the turnover earned from the sale of the membership card by the validity duration of the card (USD 36,000 divided by (:) 40 years is equal to (=) USD 900/year).

Example 2: Limited Liability Company A2 is a golf course business enterprise. In 2009, the company sold a membership card to customer B2 at the price of USD 36,000 (inclusive of excise tax and exclusive of value-added tax). The service provision duration is 40 years and payment is paid by installments within the first 5 years under the contract as follows:

|

Year |

Payment level (USD) |

|

2009 |

10,000 |

|

2010 |

9,000 |

|

2011 |

8,000 |

|

2012 |

7,000 |

|

2013 |

2,000 |

In this case, when determining turnover for calculation of enterprise income tax on the sale of the golf course membership card to customer B2, annually, Company A2 shall divide the turnover earned from the sale of the membership card by the validity duration of the card (USD 36.000 divided by (:) 40 years is equal to (=) USD 900/year).

Example 3: Limited Liability Company A3 is a golf course business enterprise. In 2009, the company sold a membership card to customer B3 at the price of USD 36,000 (inclusive of excise tax and exclusive of value-added tax). The service provision duration is 40 years ;and equal payment is made once every five years. Specifically as follows:

|

Year |

Payment level (USD) |

|

2009 |

4,500 |

|

2014 |

4,500 |

|

2019 |

4,500 |

|

2024 |

4,500 |

|

2029 |

4,500 |

|

2034 |

4,500 |

|

2039 |

4,500 |

|

2044 |

4.500 |

|

2049 |

4,500 |

In this case, when determining the turnover for calculation of enterprise income tax on the sale of the golf course membership card to customer B3, annually. Company A3 shall divide the turnover earned from the sale of the membership by the validity duration of the card (USD 36,000 divided by (:) 40 years is equal to (=) USD 900/year)."

Article 2. Organization of implementation and effect

This Circular takes effect on the date of its signing and applies from the 2009 tax period.

Any problems arising in the course of implementation should be reported to the Ministry of Finance for timely guidance and settlement.-

|

|

FOR

THE MINISTER OF FINANCE |