Nội dung toàn văn Circular No.08/2001/TT-BTC, promulgated by the Ministry of Finance, additionally guiding the regulations on enterprise income tax applicable to foreign organizations' branches operating in Vietnam stipulated in the Finance Ministry's Circular No. 99/1998/TT-BTC of July 14, 1998.

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 08/2001/TT-BTC |

Hanoi, January 18, 2001 |

CIRCULAR

ADDITIONALLY GUIDING THE REGULATIONS ON ENTERPRISE INCOME TAX APPLICABLE TO FOREIGN ORGANIZATIONS’ BRANCHES OPERATING IN VIETNAM STIPULATED IN THE FINANCE MINISTRY’S CIRCULAR No. 99/1998/TT-BTC OF JULY 14, 1998

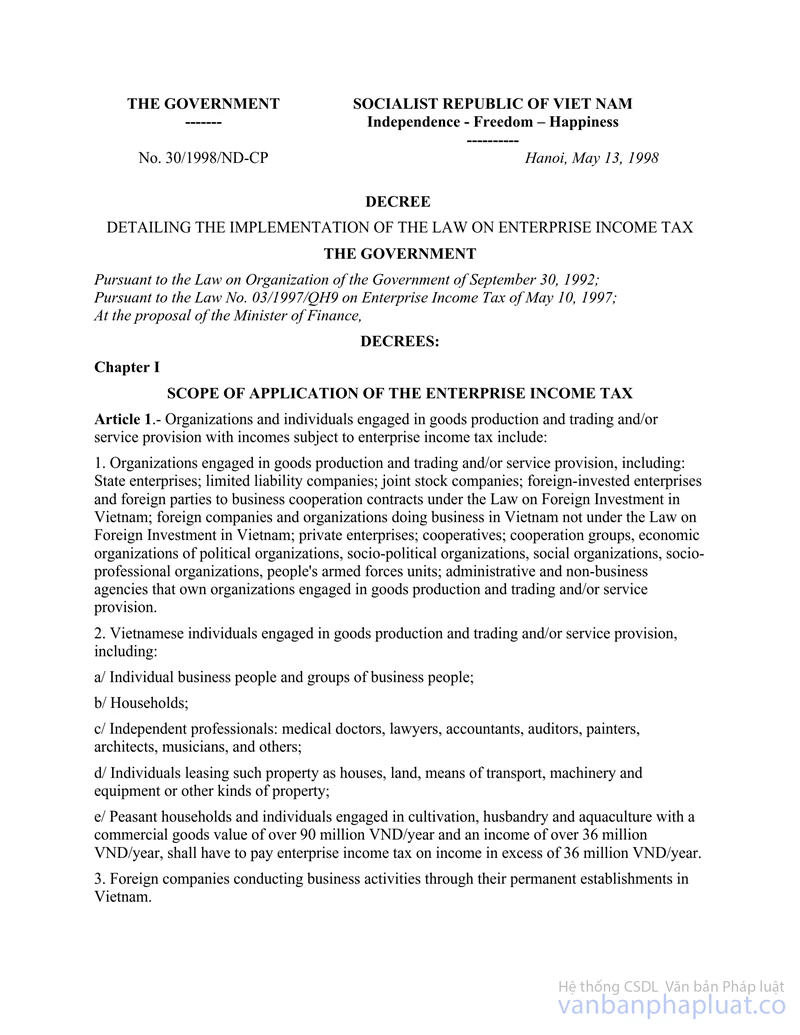

Pursuant to the Governments Decree

No.30/1998/ND-CP of May 13, 1998 detailing the implementation of the Enterprise

Income Tax Law;

Pursuant to the Governments Decree No.13/1999/ND-CP of March 17, 1999 on

organization and operation of foreign credit institutions and their

representative offices in Vietnam;

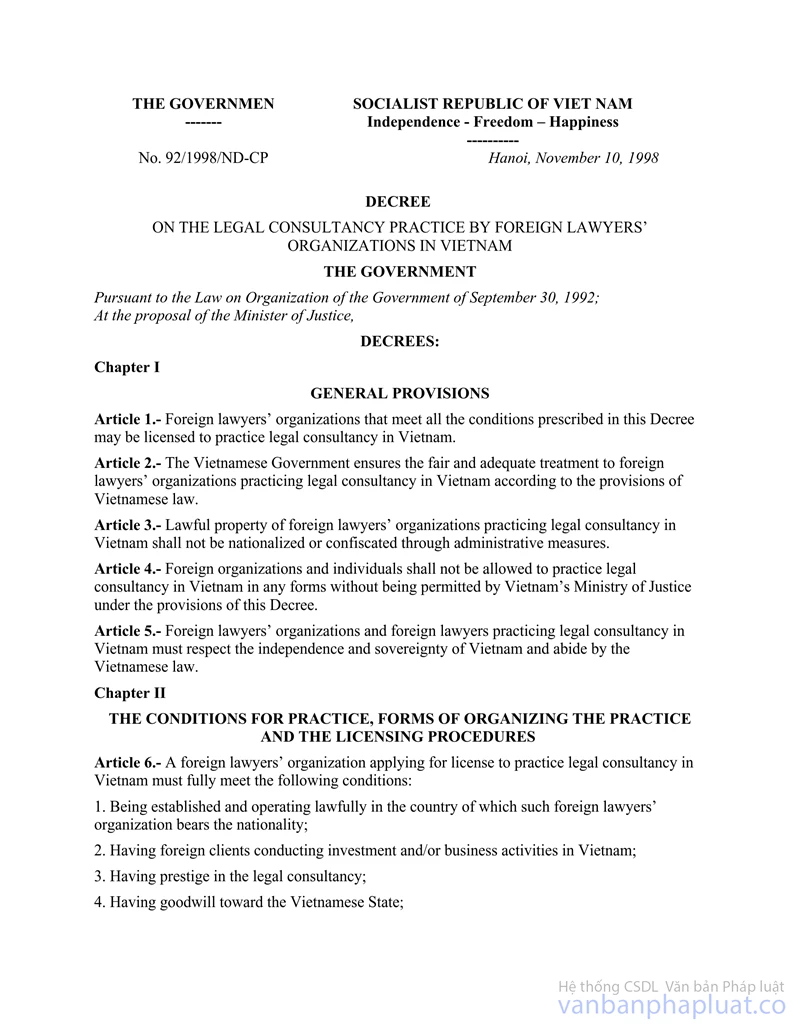

Pursuant to the Governments Decree No.92/1998/ND-CP of November 10, 1998 on

the legal consultancy practice by foreign lawyers organizations in Vietnam;

Pursuant to the Governments Decree No.45/2000/ND-CP of September 6, 2000 on

Vietnam-based representative offices and branches of foreign traders and

foreign tourist enterprises in Vietnam;

The Finance Ministry hereby additionally guides the enterprise income tax as

follows:

I. GENERAL PROVISIONS

1. This Circular applies to foreign organizations branches operating in Vietnam, including: branches of foreign lawyers organizations, branches of foreign credit institutions, branches of foreign cigarette companies and other branches licensed to conduct business activities in Vietnam according to the provisions of Vietnam laws, hereinafter collectively referred to as the foreign branches.

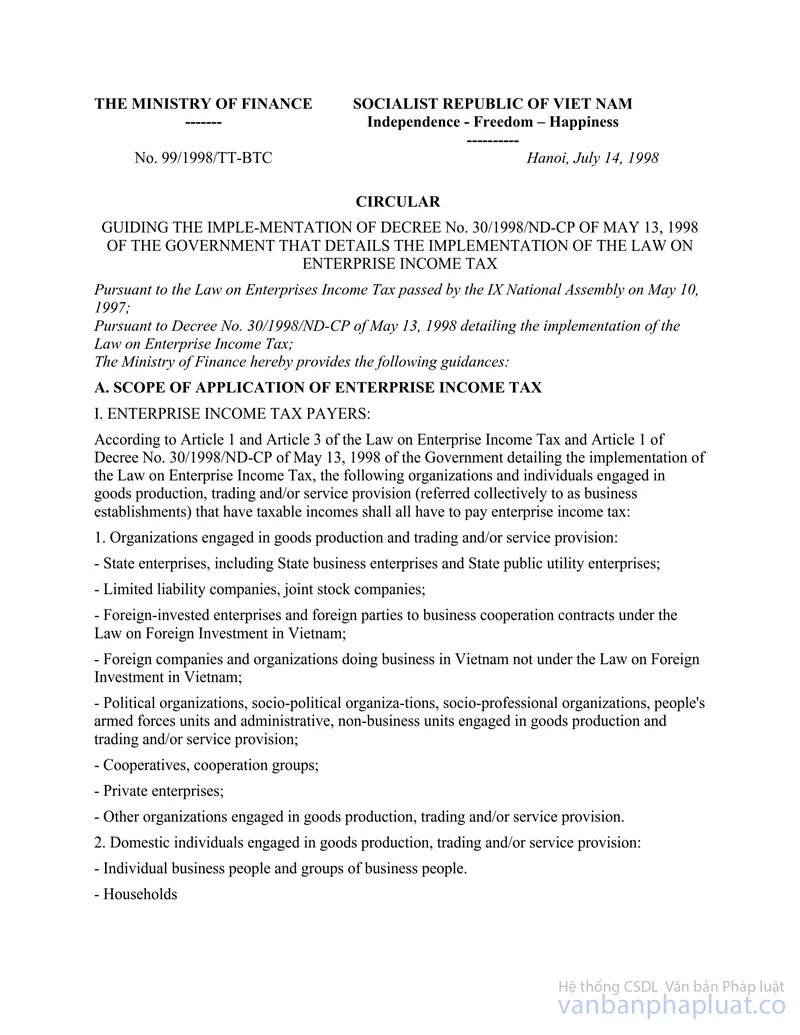

2. Foreign branches shall be enterprise income tax payers under the Enterprise Income Tax Law and the guidance in the Finance Ministrys Circular No. 99/1998/TT-BTC of July 14, 1998.

3. In cases where international treaties, agreements and/or commitments which the Vietnamese State or Government has acceded to or signed with international organizations or foreign States and Governments contain provisions on tax on foreign branches operations different from the guidance in this Circular, the provisions of such international treaties, agreements or commitments shall apply.

II. SPECIFIC CONTENTS ON ENTERPRISE INCOME TAX APPLICABLE TO THE FOREIGN BRANCHES

1. The foreign branches incomes subject to enterprise income tax shall be determined according to the guidance in Part B of the Finance Ministrys Circular No. 99/1998/TT-BTC of July 14, 1998.

The enterprise income tax rate applicable to foreign branches shall be 32%.

2. When determining income subject to enterprise income tax, foreign branches in Vietnam shall be entitled to account their business management expense amounts allocated by their parent foreign organizations according to the actually arising expenses for their business operations, provided that such allocated expense amounts must not exceed the proportion between the turnover generated in Vietnam and the foreign organizations total turnover. The maximum expense amount to be allocated by a foreign organization to its branch in Vietnam shall be determined as follows:

|

Maximum level of business management expense allocated by the foreign organization to its branch in a tax calculation year |

= |

Total turnover of the foreign branch in a tax calculation year |

x |

Total business management expense of the foreign organization in a tax calculation year |

|

Total turnover of the foreign organization in a tax calculation year |

Within 3 months after submitting its enterprise income tax settlement report of a tax calculation year, the foreign branches shall have to produce to the tax authorities their parent foreign organizations financial reports already certified by independent auditing organization and clearly showing such indexes as: total turnover, total business management expense of the foreign organizations and the management expense allocated to their branches, which shall serve as basis for determining business management expense amount to be allocated to the foreign branch in Vietnam.

3. Foreign branches shall not be entitled to account into their expenditures when determining taxable income, the amounts remitted to their headquarters or paid to other branches owned or controlled by the same foreign organizations (except for charge amounts paid for services actually used for business operations of the branches in Vietnam) in form of royalties, charges or any similar payable amounts for the use of invention patents or other rights; or in form of commissions paid for separate services; or in form of interests on the branchs loans. Particularly for branches of foreign credit institutions, the loan interest amounts paid for such foreign credit institutions shall be calculated into their expenditures when determining their taxable incomes.

4. Loan interest payment expenses related to the legal capital or charter capital of a foreign branch shall not be accounted into its reasonable and valid expenditure upon determining the taxable income.

5. Transactions conducted between foreign branches and their headquarters or other branches under the same foreign organizations ownership or control must be

6. In cases where foreign branches fail to fully observe the regime of accounting, invoices and vouchers, the tax authorities shall apply appropriate measures to determine the taxable incomes of such foreign branches, or may apply the method of distributing profits of foreign organizations in a tax calculation year to their branches in Vietnam according to the following formula:

|

Taxable income in a period of the Vietnam-based foreign branch |

= |

Total turnover in a period of the foreign branch |

x |

Total income in a period of the foreign organization |

|

Total turnover in a period of the foreign organization |

In this case, foreign branches shall have to produce to the tax authorities the foreign organizations accounting reports already certified by independent auditing organizations, which shall serve as basis for distributing taxable incomes to foreign branches.

In cases where foreign branches fail to supply documents to serve as basis for distributing taxable incomes to such foreign branches, the tax authorities shall base themselves on the already investigated and gathered documents to set the taxable incomes of the foreign branches.

7. Upon determining the taxable income of a tax calculation year, foreign branches shall be entitled to clear it against losses carried forward from previous years according to the provisions of Article 37 of the Governments Decree No. 30/1998/ND-CP of May 3, 1998 detailing the implementation of the Enterprise Income Tax Law. The loss transfer shall be effected by carrying forward the whole loss amount of any tax calculation year to the subsequent profit-making year and the income of the subsequent years shall be used to make up for such loss amount. The loss transfer duration must not exceed 5 years counted from the year next to the loss-arising year.

8. When transferring their profits abroad, the foreign branches shall not have to pay the tax on transfer of income abroad for the income generated since the 1999 fiscal year.

III. ENTERPRISE INCOME TAX REGISTRATION, DECLARATION, PAYMENT AND FINAL SETTLEMENT

1. Tax registration:

Foreign branches shall have to make enterprise income tax registration with local tax authorities (Tax Departments of the provinces and centrally-run cities) of localities where such branches are located.

2. Tax declaration:

Foreign branches shall have to make and submit written declarations of tax to be temporarily paid for the whole year according to the form prescribed in the Finance Ministrys Circular No. 99/1998/TT-BTC to the tax authorities directly managing them on January 25 every year at the latest.

Declaration bases are production, business and/or service results of the preceding year and business prospects of the following year.

After receiving written declarations, the tax authorities shall check and determine the tax amount temporarily paid for the whole year,

If the foreign branches fail to declare or unclearly declare bases for determining tax amounts to be temporarily paid for the whole year in their written declarations, the tax authorities may request such foreign branches to explain bases for determining tax amounts to be temporarily paid for the whole year. In cases where foreign branches fail to explain or fail to prove the bases inscribed in their declarations at the tax authorities requests, the latter may set tax amounts to be temporarily paid for the whole year.

3. Tax payment:

Foreign branches shall temporarily pay tax for each quarter in full and on time according to the tax authorities tax notices.

The tax payment deadlines inscribed in tax payment notices must not be later than the last day of each quarter.

4. Tax final settlement:

Foreign branches shall have to make tax final settlements with the tax authorities and declare indexes according to the form prescribed in the Finance Ministrys Circular No. 99/1998/TT-BTC of July 14, 1998.

The year for enterprise income tax final settlement shall be the solar calendar year starting on January 1 and ending on December 31 of the same year. In cases where a foreign branch is allowed to apply a fiscal year different from the above-said solar calendar year, it shall also be allowed to make tax final settlement according to such fiscal year.

Foreign branches shall have to submit their production and/or business situation reports, accounting reports already audited by independent auditing organizations licensed to operate in Vietnam and enterprise income tax final settlement reports to the tax authorities directly managing them within 60 days from the end of each fiscal year.

IV. ORGANIZATION OF IMPLEMENTATION

This Circular takes effect 15 days after its signing and applies to the enterprise income tax declaration and final settlement by foreign branches as from the 1999 fiscal year.

In cases where foreign branches had completely made their enterprise income tax final settlements of the 1999 fiscal year under the Finance Ministrys previous guidance (enterprise income tax rate of 25%, not being allowed to apportion management expenses of foreign headquarters and having to pay tax on transfer of profit abroad) before the effective date of this Circular, the readjustment thereof shall not be made, except when foreign branches file written requests to the tax authorities in order to have their 1999 tax obligations determined under the guidance in this Circular.

The following Circulars of the Finance Ministry shall no longer be effective:

+ Circular No. 90-TC/TCT of November 10, 1993 guiding a number of points on tax policies toward joint-venture banks and foreign banks branches in Vietnam;

+ Circular No. 04-TC/TCT of April 23, 1997 guiding a number of points on tax policies toward branches of foreign lawyers organizations operating in Vietnam;

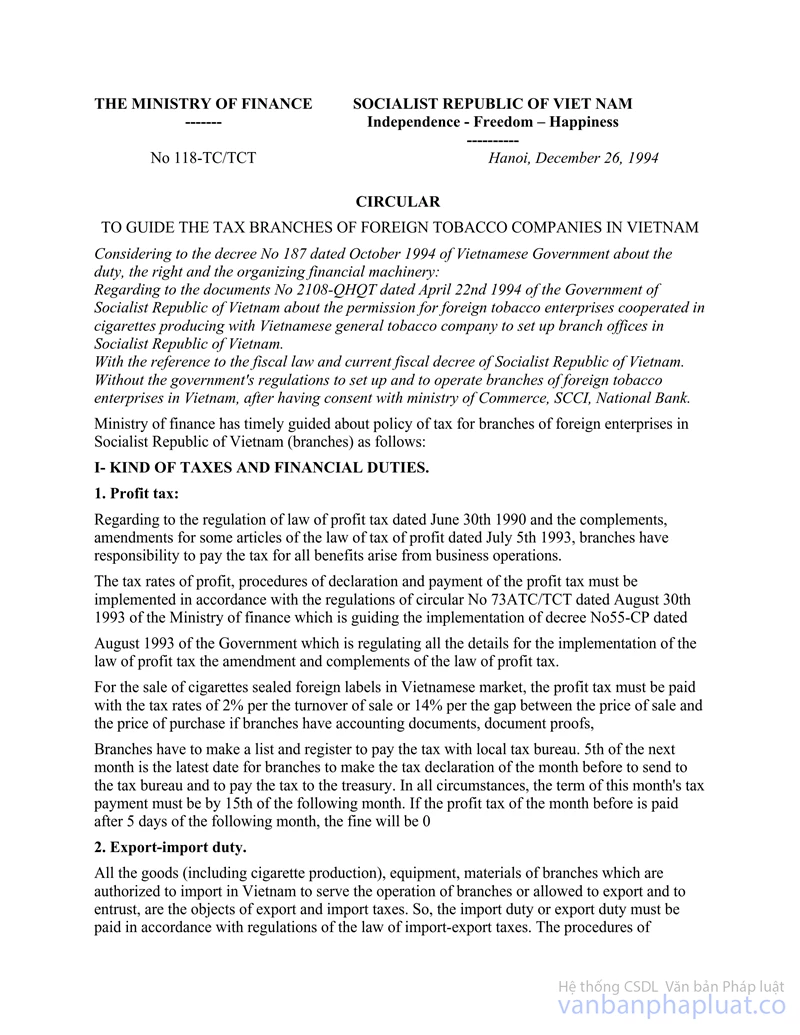

+ Circular No.118-TC/TCT of December 26, 1994 providing guidance on tax for branches of foreign cigarette companies in Vietnam.

|

FOR THE FINANCE MINISTER |