Nội dung toàn văn Official Dispatch No.10972/BTC-TCT of August 03, 2009, on value-added tax applicable to goods and services supplied for assuring the operation of vehicles engaged in international transportation

|

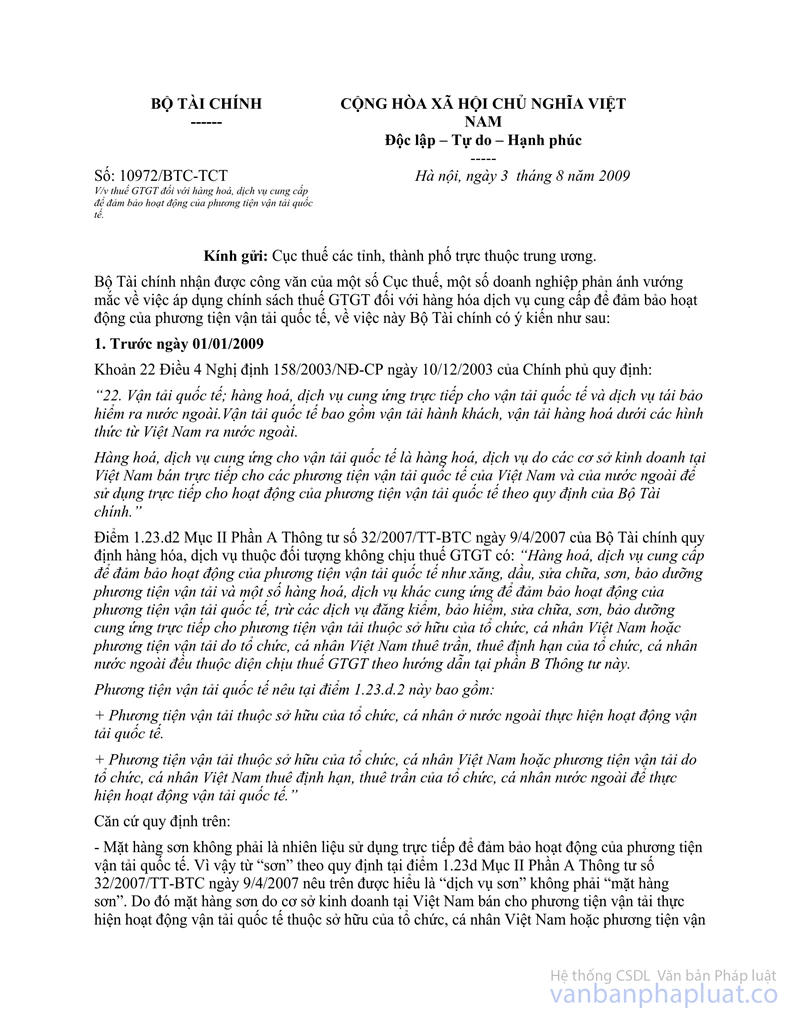

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 10972/BTC-TCT |

Hanoi, August 03, 2009 |

To: Provincial-level Tax Departments

The Ministry of Finance received official letters from several provincial-level Tax Departments and enterprises reflecting problems on the application of policies on value-added tax (VAT) on goods and services supplied for assuring the operation of vehicles engaged in international transportation. Regarding this matter, the Ministry of Finance gives its opinion as follows:

Prior to January 1, 2009:

Clause 22, Article 4 of the Government’s Decree No. 158/2003/ND-CP of December 10, 2003, stipulates:

“22. International transportation; goods and services directly supplied for international transportation and re-insurance services to foreign countries. International transportation includes passenger and cargo transportation from Vietnam to foreign countries in various forms.

Goods and services supplied for international transportation are goods and services directly sold by Vietnam-based business establishments to Vietnamese and foreign vehicles engaged in international transportation for direct use in the operation of these vehicles as prescribed by the Ministry of Finance.

Point 1.23.d2, Section II, Part A of the Ministry of Finance’s Circular No. 32/2007/TT-BTC of April 9, 2007, on non-taxable goods and services specifies: “Goods and services supplied for assuring the operation of vehicles engaged in international transportation, such as petrol and oil, repair, painting and maintenance of vehicles and some other goods and services supplied to ensure the operation of vehicles engaged in international transportation, excluding services of registry, insurance, repair, painting and maintenance directly supplied for vehicles owned by Vietnamese organizations and individuals or bare-boat chartered or time-chartered by Vietnamese organizations and individuals from foreign organizations and individuals, which are all subject to VAT as guided in Part B of this Circular.

Vehicles engaged in international transportation mentioned at this Point 1.23.d.2 include:

+ Vehicles owned by foreign organization or individuals carrying out international transportation activities;

+ Vehicles owned by Vietnamese organizations or individuals or bare-boat chartered or time-chartered by Vietnamese organizations or individuals from foreign organizations and individuals for carrying out international transportation activities.”

Pursuant to the above regulations:

- Paints are not fuels directly used to ensure the operation of vehicles engaged in international transportation. So that, the word “paints” specified at Point 1.23d, Section II, Part A of Circular No. 32/2007/TT-BTC of April 9, 2007, is understood as “painting services” but not the “commodity of paints”. Therefore, paints sold by Vietnam-based organizations and individuals for vehicles engaged in international transportation which are owned by Vietnamese organizations or individuals and vehicles bare-boat chartered or time-chartered by Vietnamese organizations or individuals from foreign organizations or individuals are subject to VAT.

- The services of registry, insurance, repair, painting and maintenance provided directly to vehicles engaged in international transportation which are owned by Vietnamese organizations or individuals and vehicles bare-boat chartered or time-chartered by Vietnamese organizations or individuals from foreign organizations or individuals are subject to VAT.

- In the period from the effective date of Circular No. 32/2007/TT-BTC to January 1, 2009, if business establishments issued non-VAT invoices upon sale of paints or provision of registry, insurance, repair, painting and maintenance services to vehicles engaged in international transportation which are owned by Vietnamese organizations or individuals or vehicles bare-boat chartered or time-chartered by Vietnamese organizations or individuals from foreign organizations or individuals, provincial-level Tax Departments shall guide them to issue new invoices (VAT invoices) in replacement of issued ones and make adjusted declarations according to regulations.

2. From January 1, 2009, application of VAT on goods and services supplied to vehicles engaged in international transportation complies with the Ministry of Finance’s Circular No. 129/2008/TT-BTC of December 26, 2008, providing guidance on value-added tax.

The Ministry of Finance provides the above guidance to provincial-level Tax Departments for compliance.

|

|

FOR THE MINISTER OF FINANCE |