Ordinance No. 14/2004/PL-UBTVQH11 of March 24th, 2004, amending and supplementing a number of articles of the ordinance on income tax on high-income earners đã được thay thế bởi Law No. 04/2007/QH12 of November 21, 2007 on personal income tax và được áp dụng kể từ ngày 01/01/2009.

Nội dung toàn văn Ordinance No. 14/2004/PL-UBTVQH11 of March 24th, 2004, amending and supplementing a number of articles of the ordinance on income tax on high-income earners

|

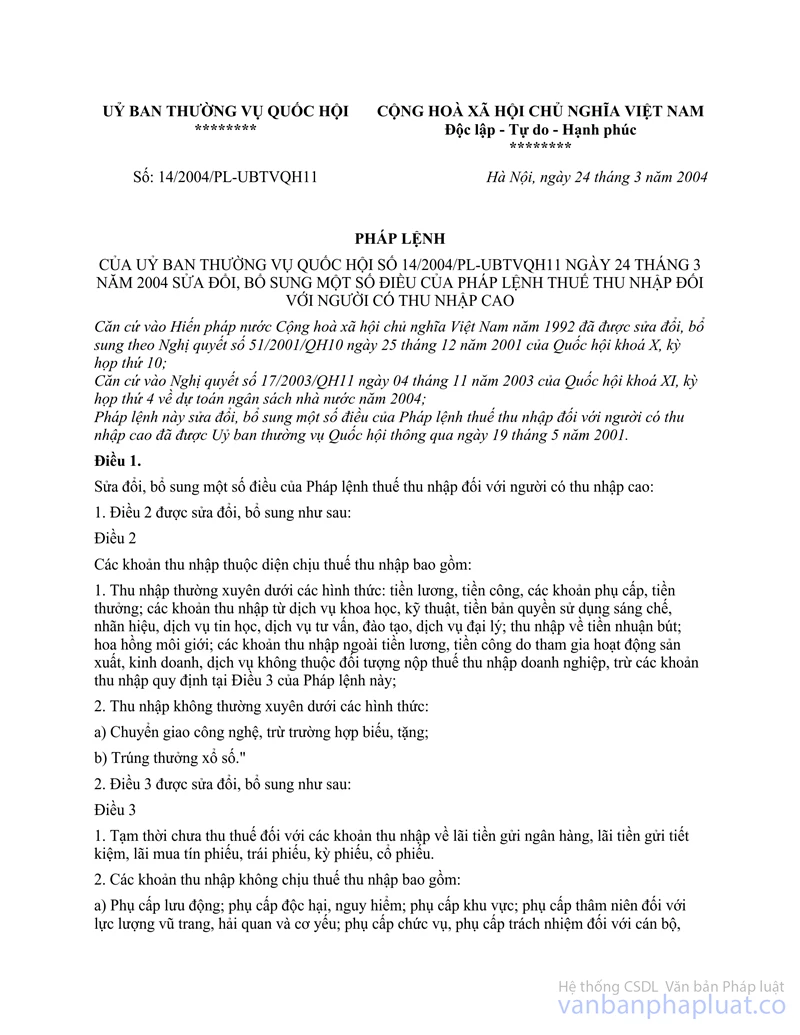

THE STANDING

COMMITTEE OF NATIONAL ASSEMBLY |

SOCIALIST REPUBLIC OF VIET NAM |

|

Hanoi, March 24th, 2004 |

ORDINANCE

AMENDING AND SUPPLEMENTING A NUMBER OF ARTICLES OF THE ORDINANCE ON INCOME TAX ON HIGH-INCOME EARNERS

Pursuant to the 1992

Constitution of the Socialist Republic of Vietnam, which was amended and

supplemented under Resolution No. 51/2001/NQ-QH10 bổ sung điều của Hiến pháp nước cộng hoà xã hội chủ nghĩa Việt Nam năm 1992">51/2001/QH10 of December 25, 2001 of the Xth

National Assembly, the 10th session;

Pursuant to Resolution No.

17/2003/QH11 of November 4, 2003 of the XIth National Assembly, the 4th

session, on the 2004 State budget estimates,

This Ordinance amends and supplements

a number of articles of the Ordinance on Income Tax on High-Income Earners,

which was passed by the National Assembly Standing Committee on May 19, 2001.

Article 1.- To amend and supplement a number of articles of the Ordinance on Income Tax on High-Income Earners as follows:

1. Article 2 is amended and supplemented as follows:

“Article 2.-

Incomes subject to income tax include:

1. Regular incomes in the forms of salaries, wages, allowances and bonuses; incomes from scientific and technical services, copyrights on use of inventions, trademarks, informatics services, consultancy and training services, and agency services; incomes from royalties; brokerages; incomes outside salaries and wages, which are paid for engagement in production, business and/or service activities not subject to enterprise income tax, except for incomes prescribed in Article 3 of this Ordinance;

2. Irregular incomes in the following forms:

a/ Technological transfer, except for cases of donation thereof;

b/ Lottery prizes.”

2. Article 3 is amended and supplemented as follows:

“Article 3.-

1. To temporarily not collect tax on incomes, which are interests on bank deposits, interests on savings, interests on purchased treasury bonds, bonds, bills and shares.

2. Incomes not subject to income tax include:

a/ Allowances for mobile jobs; allowances for hazardous and dangerous jobs; region allowances; seniority allowances for the armed force, customs and cipher personnel; position and responsibility allowances for officials and public employees; special allowances for those working in a number of offshore islands and border areas subject to exceptionally difficult living conditions; job attraction allowances; working-trip allowances; food ration expenses and allowances for a number of particular branches and occupations according to the State-prescribed regime; and other allowances from the State budget;

b/ Pecuniary rewards for technical modifications, inventions and innovations, national and international prizes; pecuniary rewards accompanying the State-conferred titles; and other pecuniary rewards or preferential treatments from the State budget;

c/ Social allowances, insurance indemnities, severance allowances, job-loss allowances, and allowances for transfer to work at production establishments as provided for by law;

d/ Incomes earned by individual business household owners, which are subject to enterprise income tax;

e/ Social insurance and medical insurance premiums paid from salaries and wages according to law provisions.”

3. Article 9 is amended and supplemented as follows:

“Article 9.-

The taxable regular income is the total money amount earned by an individual on a monthly average in a year, which is over VND 5,000,000 for Vietnamese citizens and other individuals settling down in Vietnam; or over VND 8,000,000 for foreigners residing in Vietnam and Vietnamese citizens laboring or working overseas. Particularly for foreigners who are regarded as not residing in Vietnam, their taxable regular income is the total income generated from their work in Vietnam.

Foreigners shall be regarded as residing in Vietnam if they stay in Vietnam for 183 days or more in the period of 12 months as from the date of their arrival in Vietnam; and shall be regarded as not residing in Vietnam if they stay in Vietnam for less than 183 days in the same period.”

4. Article 10 is amended and supplemented as follows:

“Article 10.-

The partially progressive tax rates applicable to regular incomes are prescribed below:

1. For Vietnamese citizens and other individuals settling down in Vietnam:

Calculation unit: VND 1,000

|

Leve l |

Average monthly income/person |

Tax rate (%) |

|

1 |

Up to 5,000 |

0 |

|

2 |

Between over 5,000 and 15,000 |

10 |

|

3 |

Between over 15,000 and 25,000 |

20 |

|

4 |

Between over 25,000 and 40,000 |

30 |

|

5 |

Over 40,000 |

40 |

For singers, circus artists, dancers, footballers and professional athletes, 25% of their incomes shall be deducted when determining their taxable incomes.

2. For foreigners residing in Vietnam and Vietnamese citizens laboring or working overseas:

Calculation unit: VND 1,000

|

Leve l |

Average monthly income/person |

Tax rate (%) |

|

1 |

Up to 8,000 |

0 |

|

2 |

Between over 8,000 and 20,000 |

10 |

|

3 |

Between over 20,000 and 50,000 |

20 |

|

4 |

Between over 50,000 and 80,000 |

30 |

|

5 |

Over 80,000 |

40 |

3. For foreigners who are regarded as not residing in Vietnam, the tax rate of 25% shall apply to their total income amount.”

5. Article 11 is amended as follows:

“Article 11.-

The taxable irregular income prescribed in Clause 2, Article 2 of this Ordinance is the income of over VND 15,000,000 earned each time by an individual.”

6. Article 12 is amended as follows:

“Article 12.-

1. Income from technological transfer, which is over VND 15,000,000 for each transfer, shall be taxed at the rate of 5% of the total income.

2. Income from lottery prizes, which is over VND 15,000,000 for each winning, shall be taxed at the rate of 10% of the total income.”

Article 2.- This Ordinance takes implementation effect as from July 1, 2004.

Article 3.- The Government shall detail and guide the implementation of this Ordinance.

|

ON

BEHALF OF THE NATIONAL ASSEMBLY STANDING COMMITTEE |