Decree of Government No. 152/2004/ND-CP of August 6, 2004 amending and supplementing a number of articles of The Government’s Decree No. 164/2003/ND-CP of December 22, 2003 detailing the implementation of the law on enterprise income tax đã được thay thế bởi Decree of Government No. 24/2007/ND-CP of February 14, 2007 detailing the implementation of The Law On Enterprise Income Tax và được áp dụng kể từ ngày 21/03/2007.

Nội dung toàn văn Decree of Government No. 152/2004/ND-CP of August 6, 2004 amending and supplementing a number of articles of The Government’s Decree No. 164/2003/ND-CP of December 22, 2003 detailing the implementation of the law on enterprise income tax

|

THE GOVERNMENT |

SOCIALIST REPUBLIC OF VIET NAM |

|

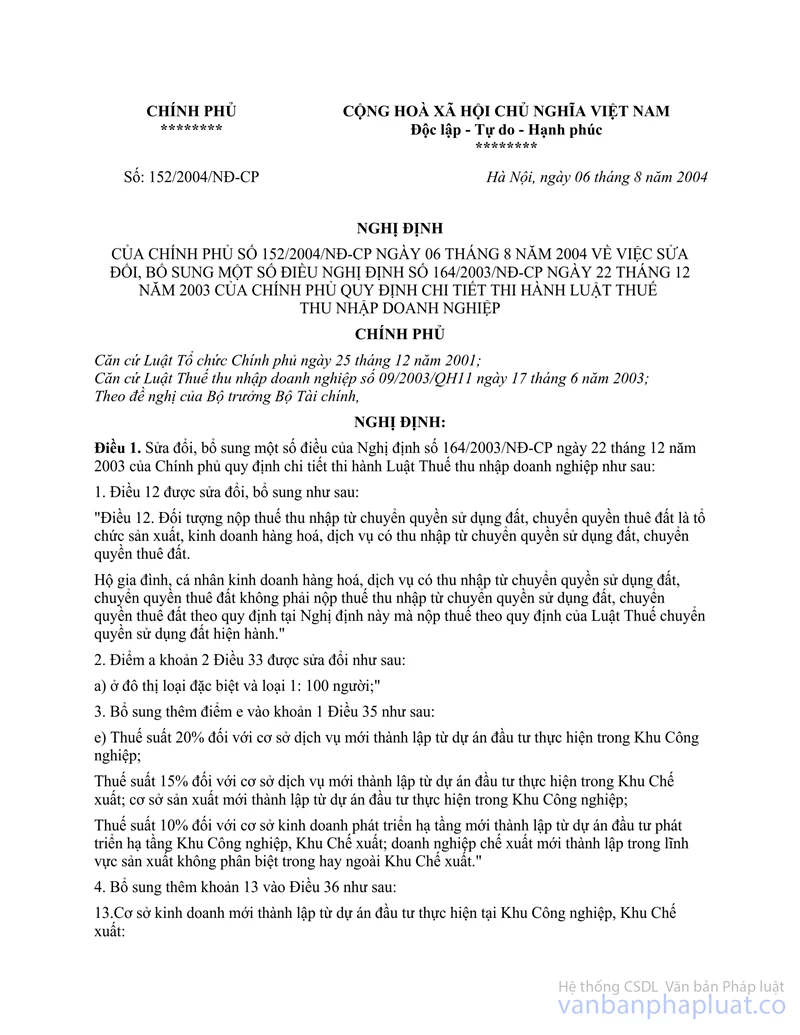

No. 152/2004/ND-CP |

Hanoi, August 6, 2004 |

DECREE

AMENDING AND SUPPLEMENTING A NUMBER OF ARTICLES OF THE GOVERNMENT’S DECREE NO. 164/2003/ND-CP OF DECEMBER 22, 2003 DETAILING THE IMPLEMENTATION OF THE LAW ON ENTERPRISE INCOME TAX

THE GOVERNMENT

Pursuant to the December 25,

2001 Law on Organization of the Government;

Pursuant to June 17, 2003 Enterprise Income Tax Law No. 09/2003/QH11;

At the proposal of the Finance Minister,

DECREES:

Article 1.- To amend and supplement a number of articles of the Government's Decree No. 164/2003/ND-CP of December 22, 2003 detailing the implementation of the Law on Enterprise Income Tax as follows:

1. Article 12 is amended and supplemented as follows:

"Article 12.- Payers of tax on incomes from land use right or land-renting right transfers are organizations producing and/or trading in goods or services and earning incomes from such transfers.

Households and individuals that trade in goods and/or services and earn incomes from land use right or land-renting right transfers shall not have to pay tax on such incomes according to the provisions of this Decree but shall pay tax according to the provisions of the current Law on Land Use Right Transfer Tax.

2. Point a, Clause 2, Article 33 is amended as follows:

"a/ In special-grade and grade-1 urban areas: 100 laborers;"

3. The following Point e is added to Clause 1 of Article 35:

"e/ The tax rate of 20% shall be applicable to service establishments newly set up under investment projects executed in industrial parks;

The tax rate of 15% shall be applicable to service establishments newly set up under investment projects executed in export processing zones; production establishments newly set up under investment projects executed in industrial parks;

The tax rate of 10% shall be applicable to establishments dealing in infrastructure development, which are newly set up under investment projects for development of infrastructures of industrial parks and export processing zones; export processing enterprises newly established in production fields regardless of whether they are located inside or outside export processing zones."

4. The following Clause 13 is added to Article 36:

"13. Business establishments newly set up under investment projects executed in industrial parks or export processing zones shall:

a/ Enjoy tax exemption for 2 years as from the date their taxable incomes are generated and the 50% reduction of payable tax amounts for 6 subsequent years for service establishments newly set up under investment projects executed in industrial parks;

b/ Enjoy tax exemption for 3 years as from the date their taxable incomes are generated and the 50% reduction of payable tax amounts for 7 subsequent years for service establishments newly set up under investment projects executed in export processing zones, production establishments newly set up under investment projects executed in industrial parks;

c/ Enjoy tax exemption for 4 years as from the date their taxable incomes are generated and the 50% reduction of payable tax amounts for 7 subsequent years for establishments dealing in infrastructure development, which are newly set up under investment projects for development of infrastructures of industrial parks and export processing zones; export processing enterprises in production fields regardless of whether they are located inside or outside export processing zones."

5. Article 37 is amended and supplemented as follows:

"Article 37.- Enterprise income tax preferences for economic zones and projects in which investment is particularly encouraged shall be as follows:

1. For business establishments operating in economic zones, the preferential tax rates as well as tax exemption or reduction durations shall be decided by the Prime Minister, but the tax exemption duration shall not exceed 4 years as from the date their taxable incomes are generated and the 50% tax reduction duration shall not exceed 9 subsequent years.

2. Business establishments newly set up under projects in which investment is particularly encouraged; newly set up foreign-invested establishments for medical examination and treatment, education and training or scientific research shall enjoy the preferential tax rate of 10% for 15 years as from the date they commence their business operations, the tax exemption for 4 years as from the date their taxable incomes are generated and the 50% reduction of payable tax amounts for 9 subsequent years. For special cases where greater particular encouragement is needed, the Finance Ministry shall propose to the Prime Minister for decision the preferential tax rate of 10% throughout the period of project execution.

The list of projects in which investment is particularly encouraged shall be prescribed by the Prime Minister for each period."

6. Point 12, Section VI of List A is amended as follows:

"12. Investing in production, processing, provision of hi-tech services in small- and medium-sized industrial parks, industrial clusters."

Article 2.- This Decree takes effect 15 days after its publication in the Official Gazette and applies to the tax calculation period from 2004 on.

The enterprise income tax preferences for investment projects executed in hi-tech parks shall comply with the Prime Minister's Decisions.

In cases where enterprise income tax preference levels stated in investment licenses or investment preference certificates are lower than those provided for in this Decree, business establishments shall enjoy the preferences provided for in this Decree for the remaining preferential duration. For investment projects with the setting up of new business establishments during the period from January 1, 2004 to the effective date of this Decree, if the preferences applicable under the Government's Decree No. 164/2003/ND-CP of December 22, 2003 are higher than those provided for in this Decree, such business establishments shall enjoy the preferences under the Government's Decree No. 164/2003/ND-CP of December 22, 2003 for the remaining preferential duration.

All previous stipulations on enterprise income tax, which are contrary to this Decree, shall be hereby annulled.

Article 3.- The Finance Ministry guides the implementation of this Decree.

Article 4.- The ministers, the heads of the ministerial-level agencies, the heads of the Government-attached agencies and the presidents of the People's Committees of the provinces and centrally-run cities shall have to implement this Decree.

|

|

ON BEHALF OF THE GOVERNMENT |