Nội dung toàn văn Decree of Government No. 156/2005/ND-CP, amending and supplementing the decrees which detail the implementation of the Special Consumption Tax Law and the Value Added Tax Law.

|

THE

GOVERNMENT |

SOCIALIST REPUBLIC OF VIET NAM |

|

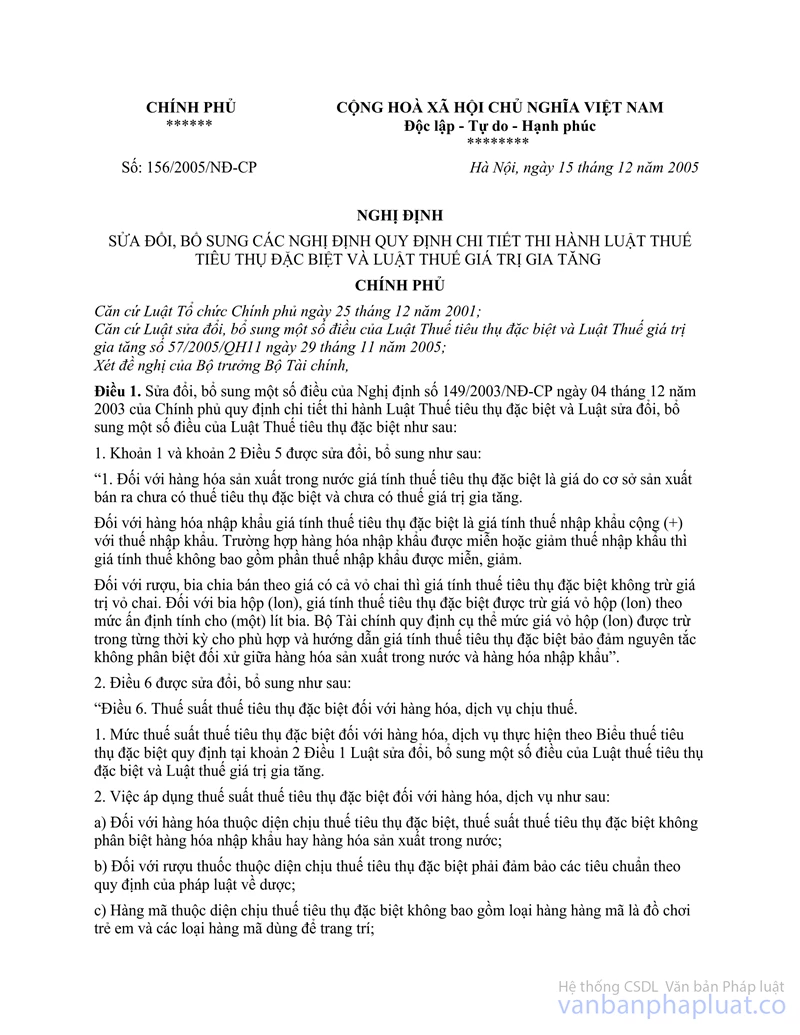

No. 156/2005/ND-CP |

Hanoi, December 15, 2005 |

DECREE

AMENDING AND SUPPLEMENTING THE DECREES WHICH DETAIL THE IMPLEMENTATION OF THE SPECIAL CONSUMPTION TAX LAW AND THE VALUE ADDED TAX LAW

THE GOVERNMENT

Pursuant to the December 25,

2001 Law on Organization of the Government;

Pursuant to November 29, 2005 Law No. 57/2005/QH11 Amending and

Supplementing a Number of Articles of the Special Consumption Tax Law and the

Value Added Tax Law;

At the proposal of the Minister of Finance,

DECREES:

Article 1.- To amend and supplement a number of articles of the Government’s Decree No. 149/2003/ND-CP of December 4, 2003, detailing the implementation of the Special Consumption Tax Law and the Law Amending and Supplementing a Number of Articles of the Special Consumption Tax Law as follows:

1. Clauses 1 and 2 of Article 5 are amended and supplemented as follows:

“1. For home-made goods, the special consumption tax calculation price shall be the sale price, exclusive of special consumption tax and value added tax, set by production establishments.

For imported goods, the special consumption tax calculation price shall be the import tax calculation price plus (+) import tax. Where imported goods are eligible for import tax exemption or reduction, the tax calculation price shall exclude the exempted or reduced import tax amount.

For bottled liquors or beers which are sold at the prices inclusive of the value of bottles, their special consumption tax calculation prices shall include the value of bottles. For canned beers, their special consumption tax calculation prices shall exclude the value of cans at the level set for 01 (one) liter of beer. The Finance Ministry shall set the specific level of value of cans to be excluded for each period and guide special consumption tax calculation prices on the principle of non-discrimination between home-made goods and imported goods.”

2. Article 6 is amended and supplemented as follows:

“Article 6.- Special consumption tax rates of taxable goods and services

1. Special consumption tax rates of goods and services shall comply with the Special Consumption Tariff specified in Clause 2, Article 1 of the Law Amending and Supplementing a Number of Articles of the Special Consumption Tax Law and the Value Added Tax Law.

2. The application of special consumption tax rates to goods and services shall be as follows:

a/ For special consumption tax-liable goods, special consumption tax rates shall apply regardless of whether they are imported or home-made;

b/ For special consumption tax-liable medicated liquors, they must satisfy the standards under the provisions of law on pharmacy;

c/ Special consumption tax-liable votive objects shall not include those being children toys and those used for decoration;

d/ For special consumption tax-liable goods items under the Heading “gasoline of various kinds, naphtha, reformade components and other components for mixing gasoline,” the Finance Ministry shall coordinate with concerned agencies in making specific provisions thereon.”

3. Article 16 is amended and supplemented as follows:

“Article 16.- Special consumption tax reduction or exemption is specified as follows:

If establishments producing special consumption tax-liable goods meet with difficulties caused by natural disaster, enemy sabotage or accident, they shall be considered for special consumption tax exemption or reduction. The tax exemption or reduction shall be settled for the year when losses are incurred. The tax reduction levels shall be determined on the basis of the extent of loss caused by natural disaster, enemy sabotage or accident, which, however, shall not exceed 30% of the tax amount to be paid by law. Where establishments suffer from so great losses that they are incapable of conducting production and business activities or paying tax, they shall be considered for special consumption tax exemption.

The Finance Ministry shall guide the procedures, order and competence to consider tax exemption or reduction provided for in this Article.”

Article 2.- To amend and supplement a number of articles of the Government’s Decree No. 158/2003/ND-CP of December 10, 2003, detailing the implementation of the Value Added Tax Law and the Law Amending and Supplementing a Number of Articles of the Value Added Tax Law as follows:

1. Clause 1 of Article 4 is amended and supplemented as follows:

“1. Products of cultivation (including products from planted forests) and husbandry; cultured and fished aquatic and marine products which have not yet been processed into other products or have been just preliminarily processed and sold by producing or fishing organizations or individuals, and at the stage of importation.

Products which have been just preliminarily processed as specified in this Clause are those which have been just sun-dried, heat-dried, chilled, cleaned or peeled, but not yet better processed or processed into other products. The Finance Ministry shall guide in detail the products specified in this Clause which are not subject to value added tax at the stage of importation, ensuring non-discrimination between home-made goods and imported goods.”

2. Point 1, Clause 2 of Article 7 is amended and supplemented as follows:

“1. Preliminarily processed cotton means cotton which has been peeled, has its seed removed, and has been classified.”

Article 3.- This Decree takes effect as from January 1, 2006.

Article 4.- Ministers, heads of ministerial-level agencies, heads of government-attached agencies, and presidents of provincial/municipal People’s Committees shall have to implement this Decree.

|

|

ON BEHALF OF

THE GOVERNMENT |