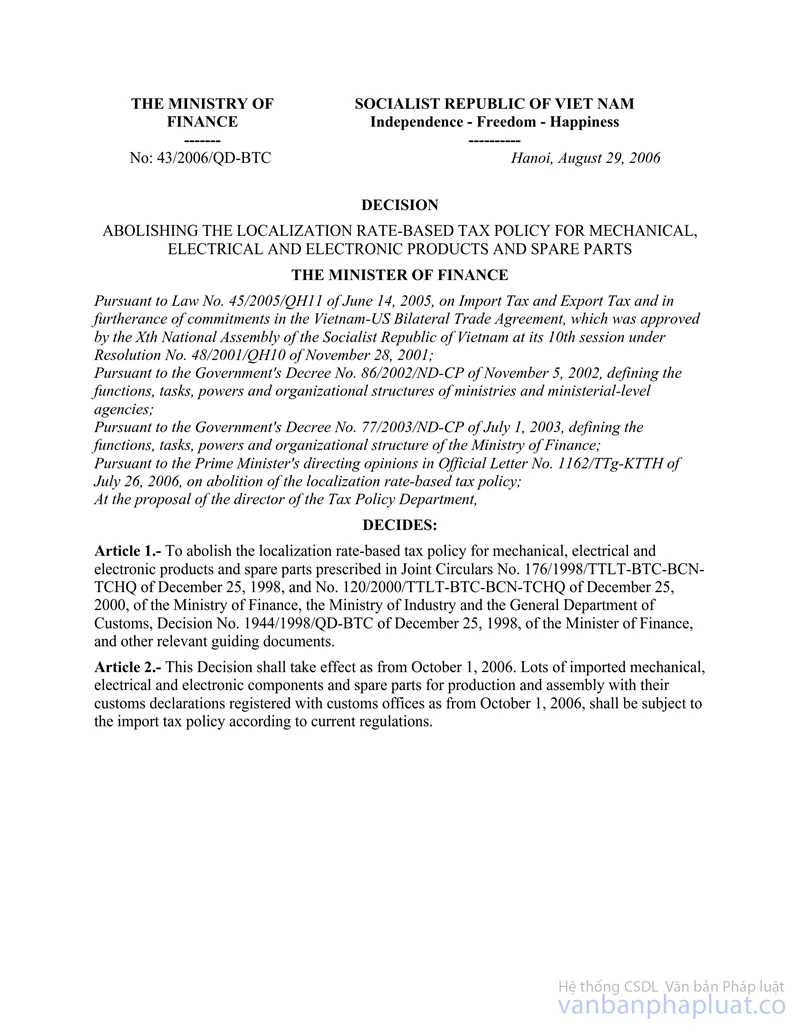

Joint circular No. 176/1998/TTLT-BTC-BCN-TCHQ of December 25, 1998 guiding the implementation of the tax policy per rate of domestic manufacture for products and spare parts of engineering-electricity- electronics industries đã được thay thế bởi Decision No. 43/2006/QD-BTC of August 29, 2006 abolishing the localization rate-based tax policy for mechanical, electrical and electronic products and spare parts và được áp dụng kể từ ngày 01/10/2006.

Nội dung toàn văn Joint circular No. 176/1998/TTLT-BTC-BCN-TCHQ of December 25, 1998 guiding the implementation of the tax policy per rate of domestic manufacture for products and spare parts of engineering-electricity- electronics industries

|

THE MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No.176/1998/TTLT/BTC-BCN-TCHQ |

Hanoi, December 25, 1998 |

INTER-MINISTERIAL CIRCULAR

GUIDING THE IMPLEMENTATION OF THE TAX POLICY PER RATE OF DOMESTIC MANUFACTURE FOR PRODUCTS AND SPARE PARTS OF ENGINEERING-ELECTRICITY- ELECTRONICS INDUSTRIES

In furtherance of the opinions of the Prime Minister in Official Dispatches No.4830/KTTH of September 24, 1997, No.1440/CP-KTTH of November 7, 1998 and No.2687/VPCP -KTTH of July 15, 1998 of the Government Office on the tax policy per rate of domestic manufacture of products;

The Ministry of Finance, the Ministry of Industry and the General Department of Customs jointly provide the following unified guidance for implementation:

1. Subject to regulation:

The import tax rate per rate of domestic manufacture shall apply to the Vietnamese enterprises and foreign-invested enterprises (hereafter called enterprises for short) operating in the following domains:

- Production and assembly of finished products of the engineering, electricity and electronics industries (with import tax rate of from 30 per cent upward).

- Production and assembly of spare pans of the above said finished products (with import tax rate of from 30 per cent upward).

2. Terms:

2.1. Domestic manufacture is the process of production and assembly in the country to replace imports.

2.2. Details are components before primary assembly (or that cannot bc taken apart or further divided).

2.3. Group of details is an ensemble of many details assembled together.

2.4. Part is an ensemble of many details or groups of details assembled together to perform a certain function of the finished product.

2.5 Spare parts is the general designation of the above mentioned details, groups of details or parts.

2.6. Semi-finished product is a detail which has not finished the production stage as designed.

2.7. Product is the general designation of any machinery, equipment, tool, utensils, means of transport...

3. Conditions for application of import tax per rate domestic manufacture:

In order to enjoy the import tariff per rate of domestic manufacture, the enterprises must have the following conditions:

3.1. They must have a technological line of production and assembly (with all the technical conditions, compatible with the investment license or the permit of production and business) already inspected and certified by the Ministry of Industry.

3.2. The products and spare parts manufactured by them must have a certificate of quality registration issued by the quality criteria measurement agency.

3.3. They must register their plans of domestic manufacture of products.

4. Rate of domestic manufacture:

The domestic manufacture rate is determined according to the following formula:

|

N = |

Z - I |

x 100% = ( 1 - |

I |

) x 100% |

|

Z |

Z |

* In which:

- N (%) is the rate of domestic manufacture kind of product or spare parts.

- Z: The import value (OF) of the whole single product or spare part produced or assembled by the enterprise (unit: US$)

- I: Import value (CIF) of the semi-finished product, detail, group of details or part directly imported or imported by authorization or bought from imports of other enterprises (unit: US$).

* For products or spare parts designed and produced by Vietnamese enterprises themselves, Z is the selling price according to the voucher of that product or spare part minus the non-production expenses such as advertisement cost, sale promotion, purchase bonus, commission for agents and indirect taxes to be paid under the prescribed regime.

* For products or spare parts which have N , O, the semi-finished products, details, groups of details and parts imported for production or assembly of these products or spare parts shall have to pay tax according to the tax rates prescribed at the Import Tariff.

5. Import tariff per rate of domestic manufacture:

5.1. Semi-finished products, details, groups of details and parts imported for the production of products or spare parts shall enjoy import tariff per rate of domestic manufacture prescribed by the Ministry of Finance.

5.2. For raw materials and materials imported to produce products or parts, the units are allowed to choose for application one of the following two tariffs:

- Import tariff per rate of domestic manufacture of products or parts. (In this case, all the raw materials and material s must apply a common tariff per rate of domestic manufacture of the products or parts).

- Import tariff for each kind of raw materials as prescribed at the Import Tariff. (In this case, all the imported materials shall apply the tariff prescribed for each kind in the Import Tariff, even if the raw material has a tariff higher than the tariff per rate of domestic manufacture).

6. Preferential index:

For the enterprises producing or assembling products and parts where preferences shall apply the import tariff per rate of domestic manufacture shall be reduced according to this formula:

Tk = Ts x (1 - k)

In which:

- Tk: Preferential import tariff

- Ts: Import tariff per rate of domestic manufacture actually achieved

- k: Regulating coefficient (k ≤ 0.5 which means tax reduction shall not exceed 50% of the tax to be paid)

The Ministry of Industry is the agency to ratify and publicize the preferential products and parts and the regulating coefficient.

7. Organization of implementation:

7.1. Registration of dossier:

Enterprises producing or assembling products and parts must submit to the Customs Office (where import procedures are carried out) the registration dossier in order to enjoy the import tariff per rate of domestic manufacture in the year, including:

- The register of the rate of domestic manufacture for the products and parts and the certification by the Ministry of Industry that the enterprise is qualified to carry out domestic manufacture of products and parts at the registered rate.

- The list and norms for the quantity of the semi- finished products, details, groups of details and components of a product or a part. This list must be divided into lists of imported semi-finished products, details; groups of details and parts together with their import prices (OF) and lists of semi-finished products, details, groups of details and parts produced in the country (for the spare parts bought from production and assembly units in the country the supply units must be clearly specified). The enterprises registering for payment according to the import tariff for raw materials per rate of domestic manufacture shall have to supply the lists and norms of the imported raw materials for production of these products and spare parts;

The above said papers shall be registered only once with the Customs Office and be valid for one year.

7.2. Monitoring and making final accounts of imports:

7.2.1. Monitoring imports: When importing goods, the enterprise shall have to declare fully the quantity of each kind of raw material, semi-finished products, details, groups of details and parts and their import prices. At the same time they shall have to open books to monitor imports as directed by the Customs Office. The General Customs Department shall guide the local Customs Offices to monitor imports in order to ensure convenience for the unit while avoiding the misuse of the import for production and assembly to evade import tax.

7.2.2. Final accounting of imports: By March 31st of the subsequent year at the latest, the enterprise shall have to sum up the situation and make the final account of the situation of import, production and assembly in the previous year. Specifically:

- The account of the rate of domestic manufacture actually achieved.

- The volume of import, the volume already used in production and assembly; the quantity of products and spare parts produced; the quantity carried over to the subsequent year; the quantity already assigned or sold or are not used for production and assembly of products and spare parts.

The data in the report must be certified by the audit agency and sent to the Ministry of Industry and the Customs Office where the unit fills in the import procedures.

On the basis of the report of the enterprise, the Customs Office makes the final accounts for the enterprise. All cases of non compliance with the regulations detected during the making of the final accounts shall be dealt with through retroactive collection of import tax strictly according to the tax rate prescribed at the Import Tariff and other current regulations.

By the end of the 31st day of March of the following year, if the enterprise fails to report the final accounts (without plausible reason), the Customs Office shall temporarily suspend it from the regime of import tariff per rate of domestic manufacture defined at this decision for the subsequent lots of goods.

8. Other provisions:

8.1. For the products and spare parts with import tariff less than 30% (thirty per cent) and which can already be produced in the country but which are not yet able to raise the tax rate to the minimum of 30% (thirty per cent) in order to enjoy the tax policy per rate of domestic manufacture, the Ministry of Industry shall consider case per case which deserve protection and shall coordinate with the Ministry of Finance in handling each case.

8.2. This Circular takes effect from January 1st, 1999.

In the process of implementation should any difficulty arises, the units should report in time to the inter-ministries for study and settlement.

|

FOR THE MINISTER OF

INDUSTRY |

FOR THE MINISTER OF

FINANCE |

FOR THE GENERAL

DIRECTOR OF CUSTOMS |