Nội dung toàn văn Decree no. 182-CP of November 10, 1994 providing details for the implementation of resolution no. 216-nq/ubtvqh9 on the 30th of august 1994 of the standing committee of the national assembly on amending and supplementing turnover tax rates for a number of occupations in the turnover tax table promulgated by the Government

|

THE GOVERNMENT |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 182-CP |

Hanoi, November 10, 1994 |

DECREE

PROVIDING DETAILS FOR THE IMPLEMENTATION OF RESOLUTION No. 216-NQ/UBTVQH9 ON THE 30TH OF AUGUST 1994 OF THE STANDING COMMITTEE OF THE NATIONAL ASSEMBLY ON AMENDING AND SUPPLEMENTING TURNOVER TAX RATES FOR A NUMBER OF OCCUPATIONS IN THE TURNOVER TAX TABLE.

THE GOVERNMENT

Pursuant to the Law on Organization of the Government on the 30th of

September 1992;

Pursuant to the Law on Turnover Taxes passed by the VIIth National Assembly on

the 30th of June 1990; the Law on the Amendment and Supplementation of a Number

of Points in the Law on Turnover Taxes passed by the IXth National Assembly on

the 30th of June 1990; the Law on the Amendment and Supplementation of a Number

of Points in the Law on Turnover Taxes passed by the IXth National Assembly on

the 5th of July 1993, and resolution No.216-NQ/UBTVQH9 on the 30th of August

1994 of the Standing Committee of the National Assembly;

At the proposal of the Minister of Finance.

DECREE:

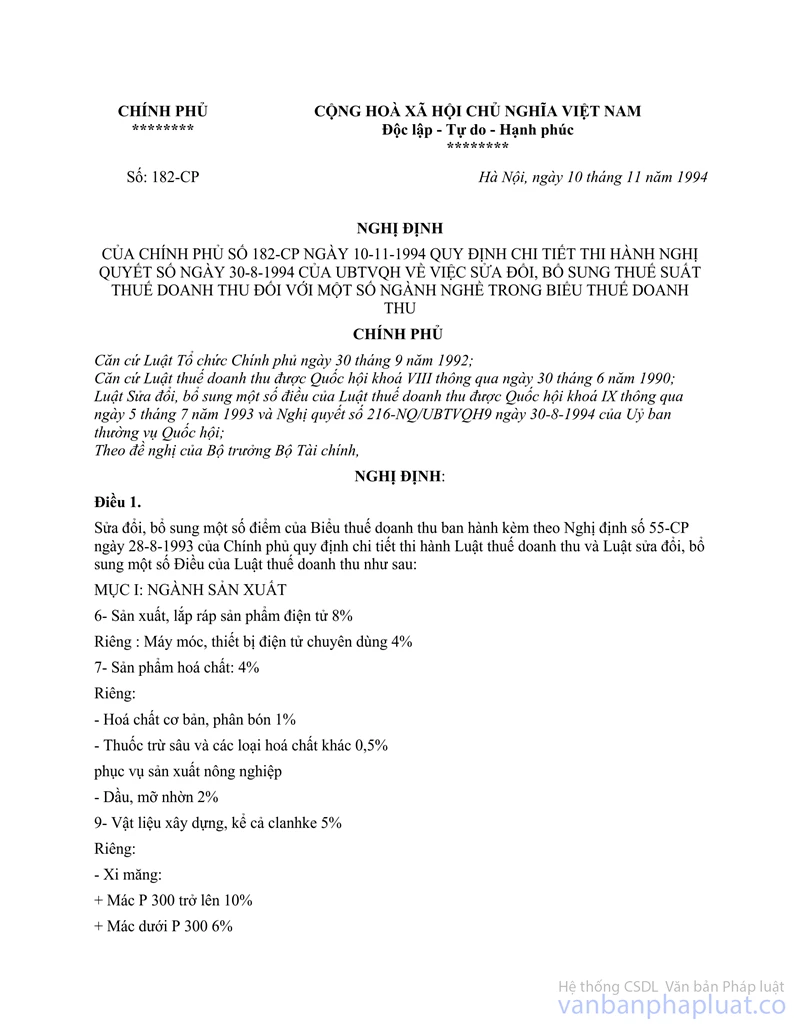

Article 1.- To amend and supplement a number of points in the Turnover Tax Table issued together with Decree No.55-CP on the 28th of August 1993 of the Government which provides details for the implementation of the Law on Turnover Taxes and the Law on the Amendment and Supplementation of a Number of Points in the Law on Turnover Taxes as follows:

PART I - PRODUCTION BRANCHES:

6. Production and assembly of electronic products: 8%

Except: specialized electronic machines and equipment: 4%

7- Chemical products: 4%

Except:

- Basic chemicals, fertilizer: 1%

- Insecticides and other chemicals for agricultural production: 0.5%

- Luboils and grease: 2%

9- Construction materials, including clinker: 5%

Except:

- Cement:

+ From P300 upwards: 10%

+ Under P300: 6%

- Concrete: 3%

12- Paper and paper products:

a/ Assorted paper: 2%

Except: wood pulp, newsprint, writing paper: 1%

b/ Paper products: 4%

18- Fiber, textiles, cotton:

a/ Assorted fibers (including woolen thread for carpet, jute, silk and sedge fibers), thread: 2%

Except: woolen thread, synthetic fiber: 4%

b/ Assorted textiles: 5%

Except: Jute, sedge, bamboo and other woven products made by hand or semi-mechanized equipment: 3%

c/ Home-grown, semi-processed cotton: 1%

22- Printing and publication:

a/ Printing and publishing political books, text-books, scientific and technical books, children's books, books and newspapers in the languages of ethnic minorities: 0%

b/Printing and publishing assorted newspapers: 0,5%

c/ Printing and publishing assorted books: 1%

d/ Producing and distributing films, music cassettes, video-cassettes, laser discs:

- Producing and distributing films: 1%

Except: documentary films, films on revolutionary themes, children's themes, and scientific themes: 0%

- Producing recorded music cassettes, video-cassettes and laser discs: 1%

- Producing blank music and video cassettes: 2%

24.- Physical training and sport equipment, musical instruments and spare-parts: 1%

PART IV - COMMERCE:

9- Dealing in foreign currencies, real estate:

a/ Dealing in foreign currencies: 0.5%

b/ Dealing in real estate (including building houses for sale): 4%

PART VI - SERVICES:

15- Special services:

a/ Dancing: 30%

b/ Horse racing: 20%

c/ Issuing lottery tickets for construction building and conducting other lottery activities: 30%

As for mountain areas: 20%

d/ Shipping agents: 40%

e/ Transport brokerage and other brokerages: 15%

g/ Renting golf courses: 20%

Article 2.- To stipulate in detail the application of a number of turnover tax rates amended or supplemented as mentioned at Article 1:

1. A turnover tax rate of 4% for the production and assembly of specialized electronic machines and equipment, including:

- Producing and assembling specialized electronic equipment for telephone, wireless, wireless telegraphy, wireless radio broadcasting and television broadcasting.

- Producing and assembling radar equipment.

- Producing and assembling electronic equipment for telephone, wire telegraphy, including equipment for transmission lines.

- Producing and assembling electronic equipment for use as safety signals, traffic control on railways, roads, and river transport and for sea and airport control.

- Producing and assembling signal audio-visual electronic equipment such as sirens, traffic signal boards, protection systems, fire fighting equipment...

- Producing systems of electronic equipment for installation in industrial machines or workshops (modernized by electronic equipment).

- Producing and assembling specialized, synchronized electronic equipment with conventional electronic machines and equipment attached.

2. A turnover tax rate of 3% for the production of concrete, including concrete for building houses, workshops, roads, bridges and sluices, sea and air ports, and other pre-fab concrete slabs...

3. A turnover tax rate of 1% for the semi-processing of home-grown cotton, including ginning seeded cotton and sorting out unseeded cotton.

4. The turnover to be taxed in golf course rental includes all the money collected from the issue of membership cards, the sale of admission tickets, the sale of single tickets for playing golf, the rental of golf kits (clubs, balls, shoes, clothes...), the hire of coaches and servants in playing golf...

With regard to other services at the golf course, they are liable to turnover tax rates according to each branch of business. In case a business conducts many forms of activities, and if the turnovers from these activities cannot be separated, the highest tax rate for each occupation shall be used to calculate the total turnover tax.

Article 3.- This Decree takes effect as from the 1st of September 1994.

The Minister of Finance is responsible for guiding the implementation of this Decree.

The Ministers, the Heads of ministerial level agencies and of agencies attached to the Government, the Presidents of the People's Committees of provinces and cities under the Central Government are responsible for organizing the implementation of this Decree.

|

ON BEHALF OF THE GOVERNMENT |