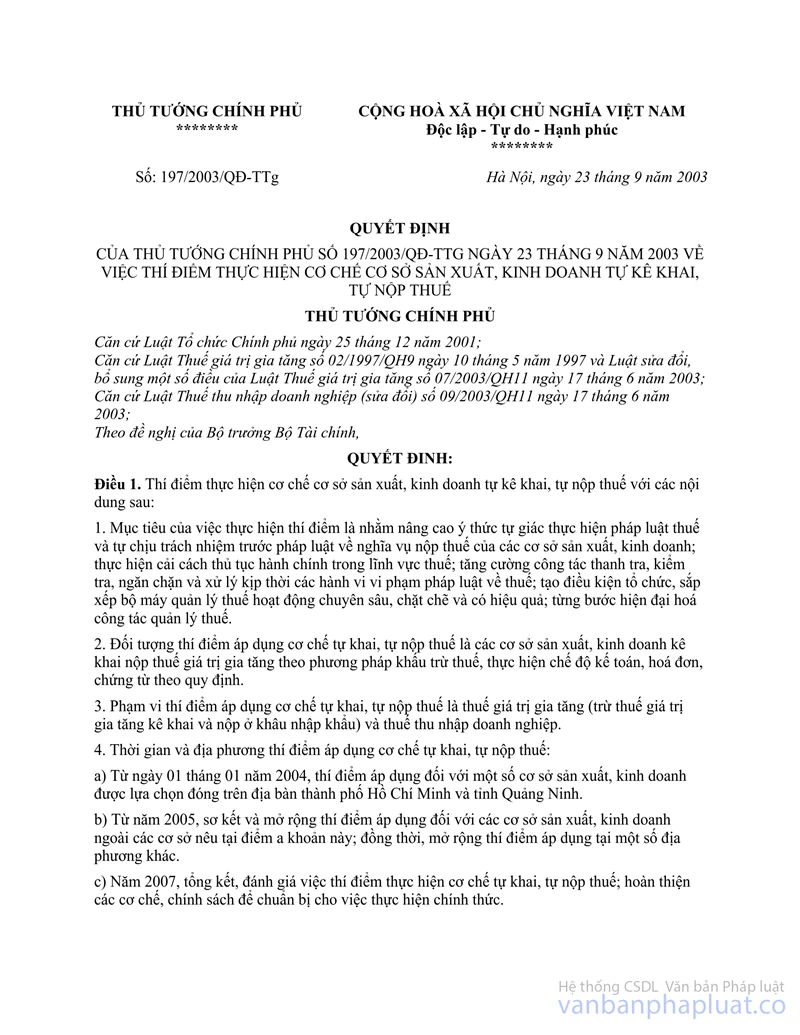

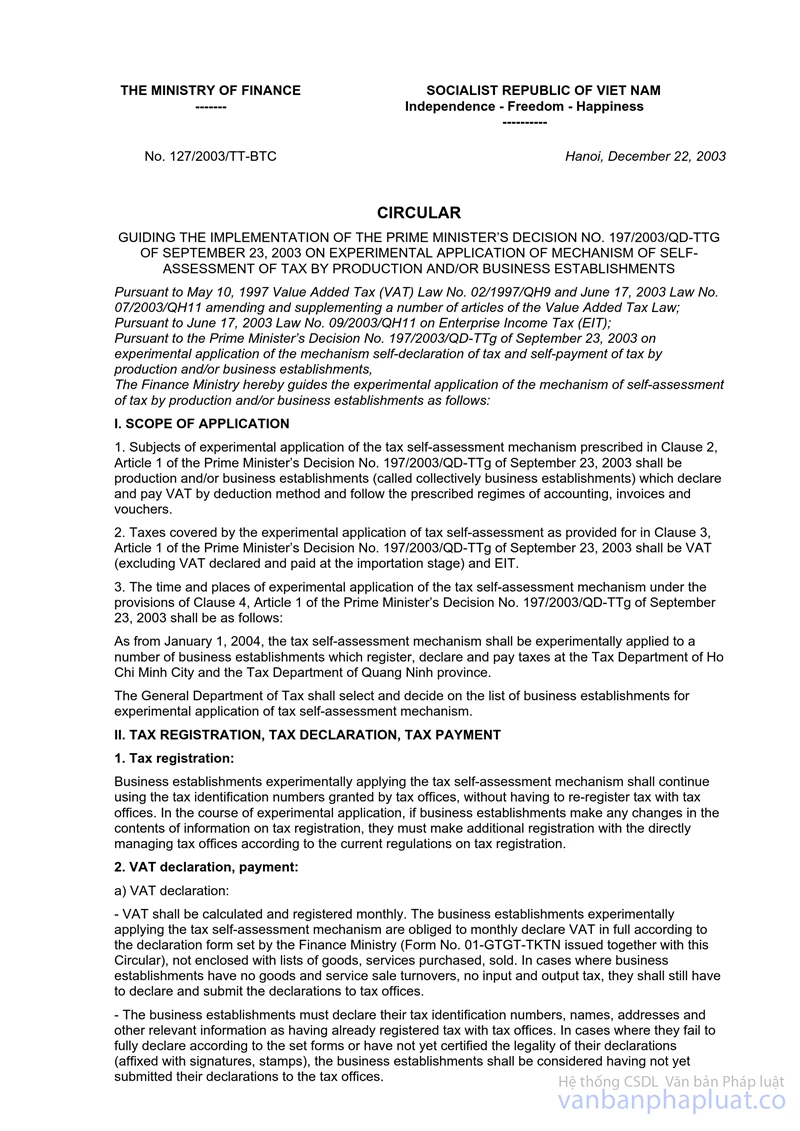

Nội dung toàn văn Decision No. 197/2003/QD-TTg of September 23, 2003, on the experimental application of the mechanism of self-assessment of taxes by production and/or business establishments

|

THE PRIME MINISTER OF GOVERNMENT |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 197/2003/QD-TTg |

Hanoi, September 23, 2003 |

DECISION

ON THE EXPERIMENTAL APPLICATION OF THE MECHANISM OF SELF-ASSESSMENT OF TAXES BY PRODUCTION AND/OR BUSINESS ESTABLISHMENTS

THE PRIME MINISTER

Pursuant to the Law on Organization of the Government of December 25,

2001;

Pursuant to Law No. 02/1997/QH9 of May 10, 1997 on Value Added Tax and Law No.

07/2003/QH11 of June 17, 2003 Amending and Supplementing a Number of Articles

of the Value Added Tax Law;

Pursuant to Law No. 09/2003/QH11 of June 17, 2003 on Enterprise Income Tax

(amended);

At the proposal of the Minister of Finance,

DECIDES

Article 1.- To experimentally apply the mechanism of self-assessment of taxes by production and/or business establishments with the following contents:

1. Objectives of the experimentation are to raise the production and/or business establishments’ conscious sense of observance of tax laws and self-responsibility before law for the obligation to pay taxes; to reform administrative procedures in the field of tax; to enhance the examination and inspection, prevent and handle in time acts of violating tax laws; to create conditions for the organization and arrangement of tax-managing apparatus operating professionally, closely and effectively; and to step by step modernize the work of tax management.

2. Subject to the experimental application of the mechanism of self-assessment of taxes are production and/or business establishments which declare and pay value added tax by the method of tax deduction and implement the prescribed accounting, invoice and voucher regimes.

3. Scope of the experimental application of the mechanism of self-assessment of taxes covers value added tax (excluding value added tax to be declared and paid at the importation stage) and enterprise income tax.

4. Time and localities of the experimental application of the mechanism of self-assessment of taxes:

a/ As from January 1, 2004, to carry out the experimental application in some selected production and/or business establishments based in Ho Chi Minh city and Quang Ninh province

b/ As from 2005, to preliminary review and expand the experimental application to production and/or business establishments other than those stated at Point a of this Clause; and at the same time to expand the experimental application to some other localities.

c/ In 2007, to make the final review and evaluation of the experimental application of the mechanism of self-assessment of taxes; and to finalize mechanisms and policies in preparation for the official application thereof.

Article 2.- Production and/or business establishments subject to the experimental application of the mechanism of self-assessment of taxes shall declare, pay and settle tax as follows:

1. For value added tax:

a/ Monthly, production and/or business establishments shall themselves declare value added tax according to the declaration forms issued by the Finance Ministry and fully pay the declared amounts into the State budget. The deadline for submission of declarations and payment of value added tax shall be the 25th of the subsequent month at the latest.

b/ Annually, production and/or business establishments shall not have to make the settlement of value added tax with tax agencies.

2. For enterprise income tax:

a/ Production and/or business establishments shall themselves shall determine enterprise income tax amounts to be temporarily paid every quarter according to forms prescribed by the Finance Ministry and pay them into the State budget no later than the 25th of the first month of the subsequent quarter.

Enterprise income tax to be temporarily paid every quarter shall be determined on the basis of such quarter’s turnovers, the proportion of taxable incomes to the preceding year’s turnovers as well as the enterprise income tax rates. In cases where there are great changes in production and business activities in the year, thus changing the proportion of taxable incomes to turnovers as compared to the preceding year’s figures, the production and/or business establishments may adjust the proportion of taxable incomes and temporarily pay tax according to the adjusted proportion, but they must file written explanation to tax agencies, clearly stating the reasons therefor. When tax agencies inspect and detect that there exists no ground for the adjustment of the proportion of taxable incomes, they may fix the tax amounts to be temporarily paid every quarter.

b/ At the end of a calendar year or fiscal year, the production and/or business establishments shall themselves declare and settle the enterprise income tax according to the declaration forms issued by the Finance Ministry within 90 days as from the date the calendar year or fiscal year ends; and at the same time fully pay by themselves the deficit tax amounts into the State budget; the surplus amounts, if any, shall be deducted to the tax amounts to be paid in the subsequent tax-payment period.

3. Production and/or business establishments shall have to bear responsibility before law for the truthfulness and accuracy of their tax declaration and calculation prescribed in Clauses 1 and 2 of this Article.

In cases of merger, amalgamation, division, separation, dissolution or bankruptcy, the production and/or business establishments shall have to make the settlement of value added tax and enterprise income tax with tax agencies according to current tax laws.

Article 3.- Tax agencies managing production and/or business establishments which experiment the mechanism of self-announcement and self-payment of taxes shall have to organize specialized apparatuses in order to:

1. Propagate and support production and/or business establishments to understand and properly implement the provisions of tax laws as well as the mechanism of self-assessment of taxes according to the provisions of this Decision.

2. Monitor the tax declaration and payment by production and/or business establishments; notify, urge or handle according to law provisions cases of late tax declaration and payment.

3. Examine, inspect and promptly handle according to their competence acts of violation of tax laws.

4. Apply measures for debt retrieval and coercive measures to cases of failing to pay tax and fines according to laws.

5. Speed up the application of informatic technology to the management of tax collection.

Article 4.- Responsibilities of the Finance Ministry

1. To promulgate documents guiding the implementation of this Decision; work out measures to prevent and restrict the situation of abusing the mechanism of self-assessment of taxes to cheat and appropriate tax amounts to be paid into the State budget. To remove obstacles and difficulties arising in the course of implementation.

2. To coordinate with the concerned ministries and localities in deciding on the selection and expansion of the application of the mechanism of self-assessment of taxes as stated at Points a and b, Clause 4, Article 1 of this Decision. To direct and inspect tax agencies in organizing the realization of contents prescribed in Article 3 of this Decision.

3. To submit to the Prime Minister for decision the expansion of subjects and scope of experimental application of the mechanism of self-assessment of taxes, apart from contents stated in Clauses 2 and 3, Article 1 of this Decision; to propose the promulgation of mechanisms and policies in preparation for the official application of the mechanism of self-assessment of taxes nationwide.

Article 5.- Other agencies, organizations, individuals and production and/or business establishments shall have to provide information on the production and/or business establishments which experiment the mechanism of self-assessment of taxes at the request of tax agencies; and coordinate with tax agencies in removing obstacles as well as cases of violating tax laws and this Decision.

Article 6.- This Decision takes effect as from January 1, 2004.

The ministers, the heads of the ministerial-level agencies, the heads of the agencies attached to the Government and the presidents of the provincial/municipal People’s Committees shall have to implement this Decision.

|

PRIME MINISTER |