Nội dung toàn văn Circular No 51/2001/TT-BTC, promulgated by the Ministry of Finance, guiding the implementation of the Prime Minister's Decision No. 58/2001/QD-TTg of April 24, 2001 on post-investment interest rate support.

|

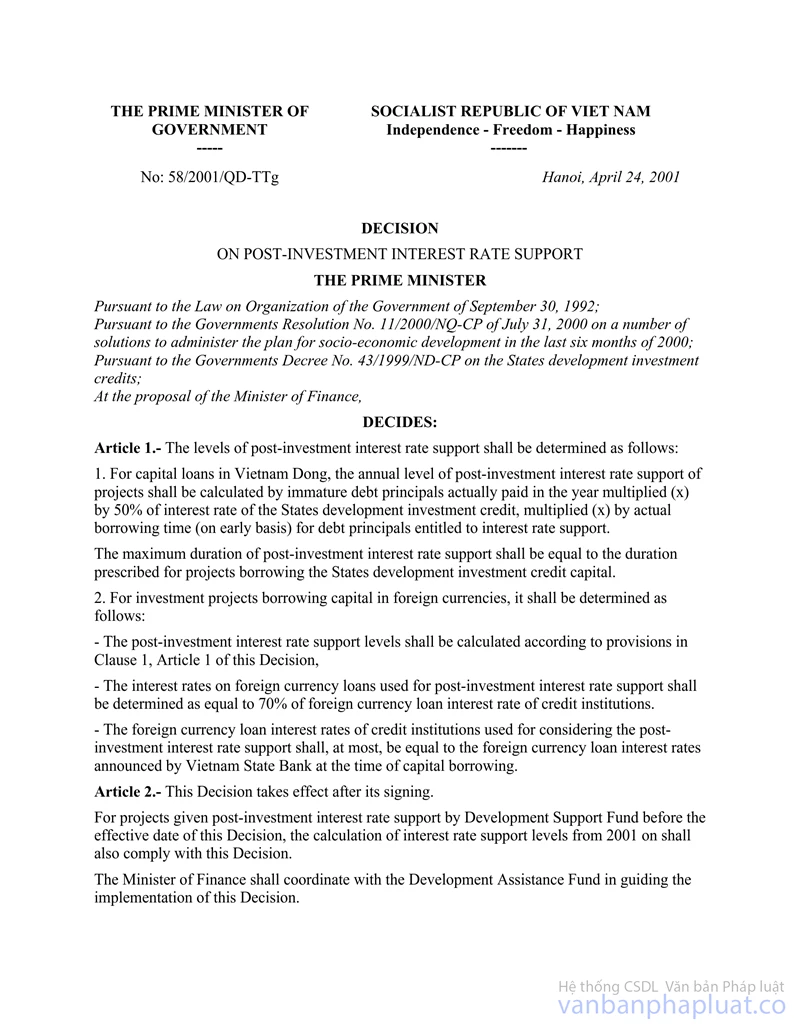

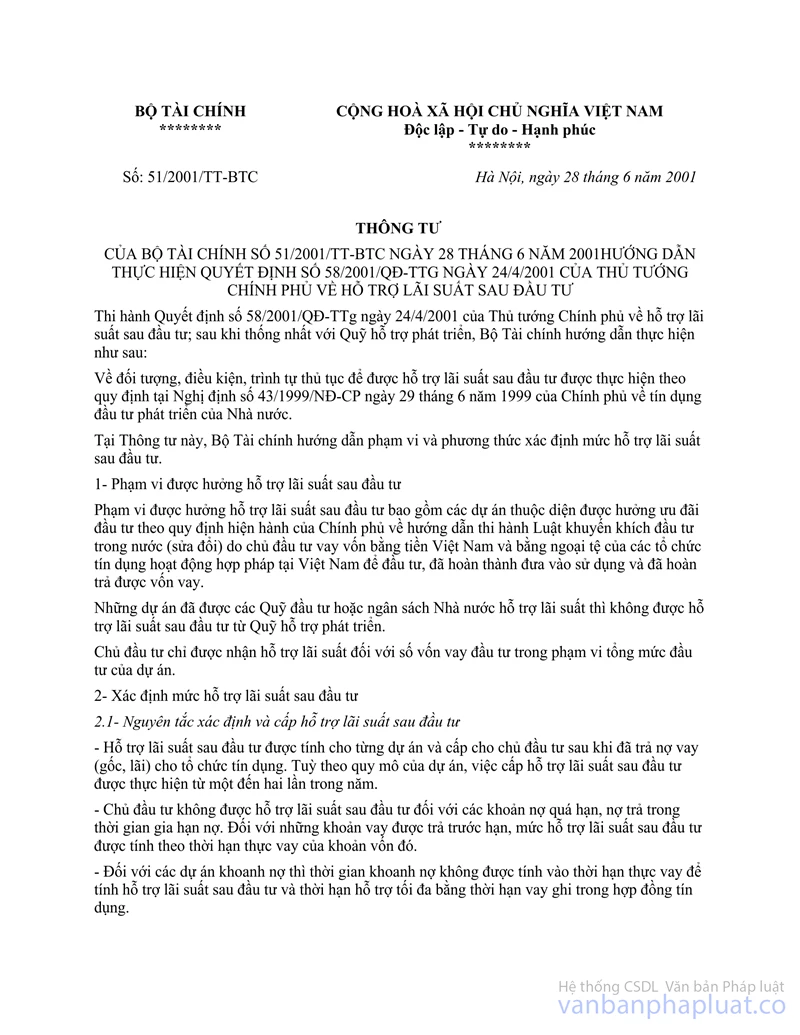

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No: 51/2001/TT-BTC |

Hanoi, June 28, 2001 |

CIRCULAR

GUIDING THE IMPLEMENTATION OF THE PRIME MINISTER’S DECISION No. 58/2001/QD-TTg OF APRIL 24, 2001 ON POST-INVESTMENT INTEREST RATE SUPPORT

In furtherance of the Prime Minister’s Decision No. 58/2001/QD-TTg of April 24, 2001 on post-investment interest rate support; after reaching an agreement with the Development Assistance Fund, the Finance Ministry gives the following guidance for the implementation thereof:

The subjects, conditions, order and procedures for post-investment interest rate support shall continue complying with the provisions of the Government’s Decree No. 43/1999/ND-CP of June 29, 1999 on the State’s development investment credit.

In this Circular, the Finance Ministry guides the scope and methods of determining post-investment interest rate support levels.

1. Scope of post-investment interest rate support:

The scope of post-investment interest rate support covers projects eligible for the investment preferences under the Government’s current regulations guiding the implementation of the Law on Domestic Investment Promotion (amended), which had been invested with loan capital in the Vietnamese currency and foreign currency(ies) borrowed by their investors from credit institutions lawfully operating in Vietnam, have been completed and put into operation, provided that such loan capital has been repaid.

Projects which enjoy interest rate support provided by investment funds or the State budget shall not be eligible for post-investment interest rate support from the Development Assistance Fund.

Investors can only receive interest rate support for investment loan capital amount within the total investment capital level of their projects.

2. Determination of post-investment interest rate support levels:

2.1. Principles for determining and providing post-investment interest rate support:

- Post-investment interest rate support shall be calculated for each project and provided to its investor after loans (principal and interest) are repaid to credit institutions. Depending on size of a project, the provision of post-investment interest rate support shall be effected once or twice a year.

- Investors cannot enjoy post-investment interest rate support for their overdue debts and/or debts repaid in the debt reschedule duration. For loans repaid ahead of time, the post-investment interest rate support levels shall be calculated according to the actual borrowing duration of such capital amount.

- For projects with frozen debts, the debt freezing duration shall not be counted into the actual borrowing term for calculating post-investment interest rate support, and the maximum support duration shall be equal to the duration inscribed in credit contracts.

2.2. Methods of determining post-investment interest rate support levels:

a) For projects with borrowed capital in Vietnam dong:

|

Post- investment interest rate support level for projects |

= |

Immature loan principal actually repaid |

x |

50% of the annual interest rate of the State’s development investment credit |

x |

Actual borrowing duration (converted into years) of loan principal entitled to the post-investment interest rate support |

b) For projects with borrowed capital in foreign currencies:

|

Post- investment interest rate support level for projects |

= |

Immature loan principal actually repaid (in original currencies) |

x |

50% x 70% of the annual interest rate of foreign-currency loans of credit institutions at the time of capital drawing |

x |

Actual borrowing duration (converted into years) of the loan principal entitled to post- investment interest rate support |

- The State’s development investment credit interest rates used for calculating post-investment interest rate support levels are those at the time of drawing loan principals eligible for post-investment interest rate support.

- For foreign-currency loan capital amounts: interest rates for considering post-investment interest rate support are actual lending interest rates of credit institutions.

- The post-investment interest rate support levels for projects with borrowed capital in foreign currencies shall be determined in original foreign currencies. On that basis, according to the USD/VND exchange rate on the inter-bank foreign currency market or foreign currency/VND cross rates announced by the State Bank of Vietnam at the time of providing support amounts, the post-investment interest rate support levels in Vietnam dong shall be determined for projects.

2.3. The actual borrowing duration for calculating post-investment interest rate support is a period of time (number of months shall be converted into years) from the date of debt acknowledgment to the date the immature debt principal is repaid to the credit institution.

a) Determining principles:

- The determination of actual borrowing duration for post-investment interest rate support shall be based on the time of receiving loan capital inscribed in the contracts and the time of repaying loan principal inscribed in debt repayment vouchers (with number of months converted into years) by investors to credit institutions.

- The period from the time of first repayment of immature loan principal to the time of first disbursement of loan capital shall serve as basis for calculating the number of actual borrowing months for the loan principal amount involved in the first repayment, and then such number shall serve as basis for counting back and determining the number of actual borrowing months for the loan principal amounts involved in the subsequent repayments.

b) Determining methods:

The methods of calculating post-investment interest rate support duration for the following cases:

- Capital amount disbursed and repaid in lump-sum;

- Capital amount disbursed in lump-sum and repaid in installments;

- Capital amount disbursed in installments and repaid in lump-sum,

are defined in Appendices 1 and 2 enclosed herewith.

3. Cost-accounting and accountancy:

3.1. For the Development Assistance Fund:

The cost-accounting and monitoring of post-investment interest rate support amounts for projects of the Development Assistance Fund shall be effected in strict compliance with the provisions of the Finance Minister’s Decision No. 162/1999/QD-BTC of December 24, 1999 on the accounting regime applicable to the Development Assistance Fund.

3.2. For investors:

Upon receiving post-investment interest rate support amounts, investors shall conduct cost-accounting of reduction of production and/or business costs in the period.

4. Organization of implementation:

This Circular takes effect after its signing. The calculation of post-investment interest rate support levels as from January 1, 2001 shall comply with the provisions of Decision No. 58/2001/QD-TTg and guidance in this Circular.

Any problems arising in the course of implementation should be reported to the Finance Ministry for study and solution.

|

FOR

THE MINISTER OF FINANCE |

APPENDIX 1

(Issued together with the Finance Ministry’s

Circular No. 51/2001/TT-BTC of June 28, 2001)

Calculation of post-investment interest rate support duration for the following cases

1. For capital amounts disbursed and repaid in lump-sum:

Example 1: Project A borrows VND 200 million and is allowed to draw such capital amount on November 1, 1999 and repay it on March 1, 2000, then the actual borrowing duration shall be 4 months.

2. For capital amounts disbursed in lump-sum and repaid in installments:

Example 2: Project B borrows VND 200 million and is allowed to draw such capital amount on November 1, 1999 and repaid in two installments: VND 100 million on March 1, 2000 and another 100 million on June 16, 2000, then the actual borrowing duration shall be:

+ For the first installment: 4 months

+ For the second installment: 7.5 months (7 months plus 15 days/30).

Example 3: Project C: - The first capital drawing: VND 250 million on November 1, 1999, and the second drawing: VND 250 million on February 1, 2000.

- The first repayment: VND 200 million on June 1, 2000 and the second repayment: VND 100 million on September 10, 2000.

The actual borrowing duration:

+ For the first repayment (VND 200 million): 7 months;

+ For the second repayment for the first capital drawing of VND 50 million (VND 250 million minus VND 200 million): 10.33 months (10 months plus 10 days/30);

+ For the second repayment for the second capital drawing: 7.33 months (7 months plus 10 days/30).

3. For capital amounts disbursed in installments and repaid in lump-sum:

Example 4: Project D: The first capital drawing: VND 100 million on November 1, 1999; the second drawing: VND 100 million on March 20, 2000, and the lump-sum debt repayment: VND 200 million on September 1, 2000.

The actual borrowing duration:

+ For the first capital drawing: 10 months;

+ For the second capital drawing: 5.33 months (5 months plus 10 days/30).

Example 5: Project E: The first capital drawing: VND 100 million on November 1, 1999; the second drawing: VND 100 million on March 15, 2000; and the third drawing: VND 100 million on June 1, 2000.

Repayment: The first installment of VND 250 million on September 1, 2000.

The actual borrowing duration:

+ For the first capital drawing: 10 months;

+ For the second capital drawing: 5.5 months (5 months plus 15 days/30);

+ For the third capital drawing: 3 months.

APPENDIX 2

(Issued together with the Finance Ministry’s Circular No. 51/2001/TT-BTC of June 28, 2001)

Determination of post-investment interest rate support levels for the following cases

Presumably: An enterprise borrows a capital amount of VND 1,200 million from a credit institution with an interest rate of 0.9%/month in 1999 and 0.81%/month in 2000. Such loan shall be repaid on the quarterly basis, with VND 100 million for each quarter. The repayment shall start in the first quarter (March 2000). The borrowing term: 37 months; the grace period: 4 months; the development investment credit interest rate: 9.72% for 1999 and 7% for 2000. And to simplify the calculation, we presume that all capital drawings or debt repayments are made on the first days of the months.

Disbursement: The first installment (November 1, 1999): VND 350 million; the second installment (February 1, 2000): VND 450 million; the third installment (August 1, 2000): VND 60 million; the fourth installment (October 1, 2000): VND 340 million.

In 2000: VND 11.1375 million:

The first quarter (March 1, 2000), provided for the first disbursement: VND 100 million x 4.86% x 4/12 = VND 1.62 million

The second quarter (June 1, 2000), provided for the first disbursement: VND 100 million x 4.86% x 7/12 = VND 2.835 million

The third quarter (September 1, 2000), provided for the first disbursement: VND 100 million x 4.86% x 10/12 = VND 4.05 million

The fourth quarter (December 1, 2000):

+ provided for the first disbursement: VND 50 million x 4.86% x 13/12 = VND 2.6325 million

+ Provided for the second disbursement: VND 50 million x 3.5% x 10/12 = VND 1.45 million

In 2001: VND 20.38 million:

The first quarter (March 1, 2001), provided for the second disbursement: VND 100 million x 3.5% x 13/12 = VND 3.78 million

The second quarter (June 1, 2001), provided for the second disbursement: VND 100 million x 3.5% x 16/12 = VND 4.66 million

The third quarter (September 1, 2001), provided for the second disbursement: VND 100 million x 3.5% x 19/12 = VND 5.53 million

The fourth quarter (December 1, 2001), provided for the second disbursement: VND 100 million x 3.5% x 22/12 = VND 6.41 million

In 2002: VND 25.48 million:

The first quarter (March 1, 2002), + provided for the third disbursement: VND 60 million x 3.5% x 19/12 = VND 3.32 million

+ Provided for the fourth disbursement: VND 40 million x 3.5% x 17/12 = 1.99 million

The second quarter (June 1, 2002), provided for the fourth disbursement: VND 100 million x 3.5% x 20/12 = VND 5.85 million

The third quarter (September 1, 2002), provided for the fourth disbursement: VND 100 million x 3.5% x 23/12 = VND 6.72 million

The fourth quarter (December 1, 2002), provided for the fourth disbursement: VND 100 million x 3.5% x 26/12 = VND 7.6 million

The post-investment interest rate support level for the whole project:

Level for the whole project = Level for 2000 + level for 2001 + level for 2002

Level for the whole project = 11.1375 + 20.38 + 25.48 = VND 56.9975 million.-