Circular No. 55/2003/TT-BTC of June 04, 2003, guiding the amendments and supplements to the Finance Ministry's Circular No. 28/2000/TT-BTC of April 18, 2000 which guides the implementation of Decree No. 176/1999/ND-CP of December 21, 1999 on registration fee đã được thay thế bởi Circular No. 95/2005/TT-BTC promulgated by the Ministry of Finance, guiding the implementation of the provisions of law on registration fees. và được áp dụng kể từ ngày 25/11/2005.

Nội dung toàn văn Circular No. 55/2003/TT-BTC of June 04, 2003, guiding the amendments and supplements to the Finance Ministry's Circular No. 28/2000/TT-BTC of April 18, 2000 which guides the implementation of Decree No. 176/1999/ND-CP of December 21, 1999 on registration fee

|

THE

MINISTRY OF FINANCE |

OF VIET |

|

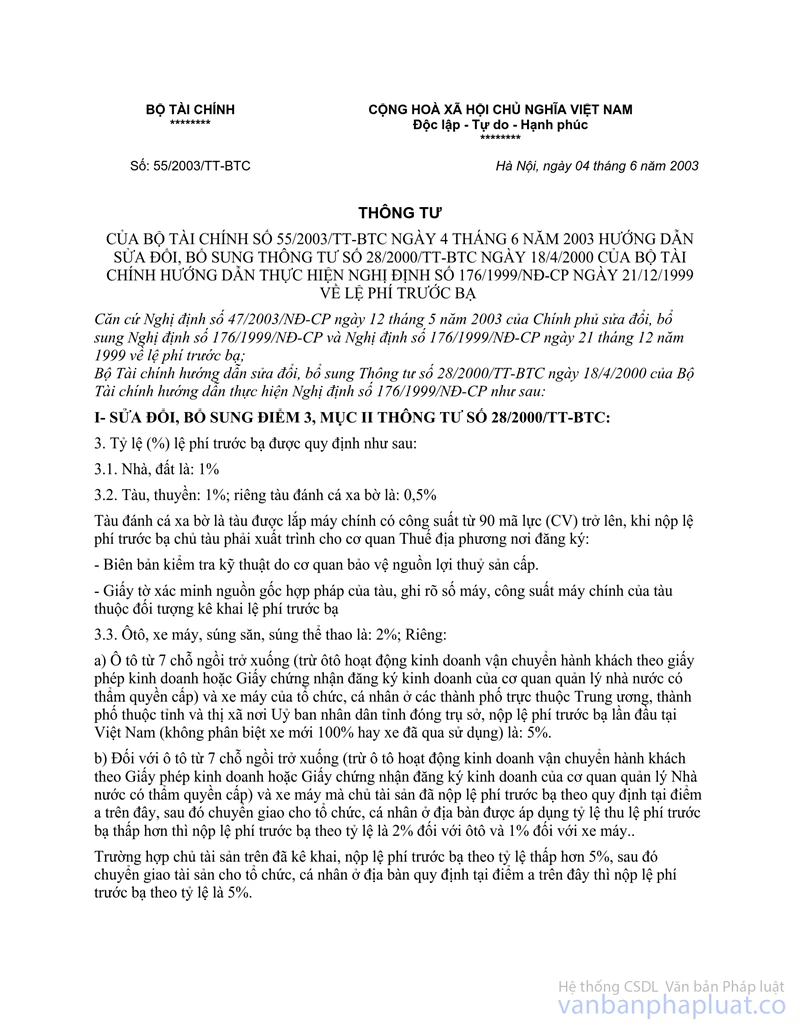

No: 55/2003/TT-BTC |

, June 04, 2003 |

CIRCULAR

GUIDING THE AMENDMENTS AND SUPPLEMENTS TO THE FINANCE MINISTRY'S CIRCULAR No. 28/2000/TT-BTC OF APRIL 18, 2000 WHICH GUIDES THE IMPLEMENTATION OF DECREE No. 176/1999/ND-CP OF DECEMBER 21, 1999 ON REGISTRATION FEE

Pursuant to the Government's Decree No. 47/2003/ND-CP of May 12, 2003 amending and supplementing the Government's Decree No. 176/1999/ND-CP of December 21, 1999 on registration fee< i="">

I. TO AMEND AND SUPPLEMENT POINT 3, SECTION II OF CIRCULAR NO. 28/2000/TT-BTC AS FOLLOWS:

3. The registration fee rates (%) are prescribed as follows:

and houses: 1%

3.2. Ships and boats: 1%, particularly for offshore fishing ships: 0.5%

Offshore fishing ships are those installed with the main engine of 90 horse power (CV) or more, when paying registration fee, the ship owners must produce to the tax offices of the localities where registration is made the following:

- Technical inspection records issued by the aquatic resource-protecting agencies;

- Papers verifying the lawful origin of the ship, clearly inscribing the engine number, capacity of the main engine of the ship which is liable to registration fee declaration.

3.3. Automobiles, motorcycles, hunting rifles and sport guns: 2%;

a/ Cars of 7 seats or under (except for cars used for passenger transportation business under business licenses or business registration certificates granted by competent State management agencies) and motorcycles of organizations and individuals in centrally-run cities as well as provincial cities and capitals, where the provincial People's Committees are headquartered, for which registration fees are paid for the first-time in Vietnam (regardless of whether they are brand-new or second-hand): 5%.

b/ For cars of 7 seats or under (except for cars used for passenger transportation business under business licenses or registration business certificates granted by competent State management agencies) and motorcycles for which the registration fees have been already paid by their owners according to the provisions at Item a above, which are later transferred to organizations and/or individuals in the localities entitled to lower registration fee rates, the registration fees shall be paid at the rates of 2% for cars and 1% for motorcycles.

In cases where the owners of the above-said properties have already declared and paid registration fees at the rates lower than 5% and later transferred these properties to organizations and/or individuals in the localities as prescribed at Point < p="">

< p="">< p="">d.1/ For cars of 7 seats or under of organizations and individuals engaged in passenger transportation business such as taxi companies, passenger transportation companies, tourist-transporting companies,... organizations and individuals that declare and pay registration fee must provide the tax offices with the following:

- Letters of introduction of organizations granted the passenger transportation business licenses or business registration certificates (for organizations) by competent State agencies. Such letters of introduction must clearly state the quantity and type of cars liable to registration fee;

- Lawful vouchers on car purchase as prescribed by the Finance Ministry;

- Passenger transportation business licenses or business registration certificates, issued by competent State agencies (copies certified by the State's Public Notary).

d.2/ For tourist cars financially leased to organizations and individuals that are granted passenger transportation business licenses (or passenger transportation business registration certificates) by competent State agencies, the financial-leasing companies which declare and pay registration fee, must provide the tax offices with the following:

- Financial-leasing companies' letters of introduction, clearly stating the quantity and type of cars registered for financial leasing;

- Financial-leasing business licenses or -business registration certificates, granted by competent State agencies (if they are copies, they must be certified by the State Public Notary);

- Financial-leasing contracts signed between financial-leasing companies and organizations and/or individuals engaged in financial-leasing passenger transportation business, which must clearly state the quantity of financial-leasing cars of 7 seats or under and the leasing term (if they are copies, they must be certified by the State Public Notary);

- Passenger transportation business licenses or business registration certificates, granted by competent State agencies to financial lessees being organizations and/or individuals with their names signed in financial-leasing contracts (copies certified by the State Public Notary).

< p="">< p="">f.1/ Passenger cars of 7 seats or under, excluding lambrettas;

f.2/ Motorcycles, including motorized two-wheelers, motorized three-wheelers, mopeds and the like, excluding motorized three-wheelers used exclusively for the disabled;

f.3/ Cities and provincial capitals mentioned in this Circular are determined according to the States administrative boundaries, concretely as follows:

- Hanoi city, Ho Chi Minh city and other centrally-run cities (such as Da Nang city, Hai Phong city,...), covering all urban and rural districts attached to them, regardless of whether they are inner or outer, urban or rural ones;

- Provincial cities and capitals where the provincial People's Committees are headquartered, covering all wards and communes attached to them, regardless of whether they are inner wards or suburban communes.

II. TO AMEND AND SUPPLEMENT ITEM K1, POINT 3, SECTION I OF CIRCULAR NO. 28/2000/TT-BTC AS FOLLOWS:

k1/ Organizations and individuals that contribute their properties as capital to joint-venture or partnership organizations having the legal person status (State enterprises, private enterprises, enterprises operating under the Law on Foreign Investment in Vietnam, limited liability companies, joint-stock companies,...); For cooperatives' members contributing capital to cooperatives, the property-receiving organizations shall not have to pay registration fee for property contributed as capital; or when such organizations are dissolved, their properties shall be distributed to member organizations and individuals for registration of their ownership or use right. Besides, if cooperatives decide to transfer properties among their members, the property-recipients shall also not have to pay registration fee when re-registering the ownership or use right.

Individuals, who contribute properties as capital to cooperatives, then leave cooperatives and receive their properties, shall not have to pay registration fee. In this case, the property-recipients must produce to the tax offices the following:

- Decisions on setting up cooperatives or charters on cooperatives' operation, enclosed with lists of cooperatives' individual members or papers proving the the capital contributed in properties to cooperatives by capital-contributing cooperatives' individual members (copies certified by the State Public Notary);

- Cooperatives' decisions on returning capital in property to cooperatives' members who leave the cooperatives (copies certified by the State Public Notary);

- Certificates on ownership or use right over properties under the names of cooperatives.

III. IMPLEMENTATION ORGANIZATION:

This Circular takes implementation effect 15 days after its publication in the Official Gazette. All previous regulations on registration fee contrary to Decree No. 47/2003/ND-CP and this Circular's guidance are hereby annulled.

In the course of implementation, if problems arise, agencies, organizations and individuals are requested to promptly report them to the Finance Ministry for study and additional guidance.

|

|

FOR THE FINANCE MINISTER |