Nội dung toàn văn Circular 07/2017/TT-BXD method for determining prices of municipal solid waste treatment services

|

MINISTRY OF

CONSTRUCTION |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No.: 07/2017/TT-BXD |

Hanoi, May 15, 2017 |

CIRCULAR

METHOD FOR DETERMINING PRICES OF MUNICIPAL SOLID WASTE TREATMENT SERVICES

Pursuant to the Government’s Decree No. 62/2013/ND-CP dated June 25, 2013 defining functions, tasks, powers and organizational structure of Ministry of Construction;

Pursuant to the Government’s Decree No. 38/2015/ND-CP dated April 24, 2015 providing for the management of waste and discarded materials;

At the request of the Director of the Department of Construction Economics,

The Minister of Construction promulgates a Circular introducing the method for determining prices of municipal solid waste treatment services.

Article 1. Scope and regulated entities

1. This Circular provides guidance on the method for determining the price of municipal solid waste (MSW) treatment service which is used as the basis for setting, evaluating and approving specific prices of MSW treatment services.

2. This Circular applies to organizations and individuals involved in setting, evaluation and approval for prices of MSW treatment services and MSW treatment service providers.

Article 2. Rules for determining prices of MSW treatment services

1. The price of MSW treatment service must be determined in conformity with the MSW treatment technology and according to technical process, environmental protection regulations/ standards, technical-social norms promulgated or announced by competent authorities as well as the service quality.

2. The price of MSW treatment service must be accurately and sufficiently determined, include reasonable costs of construction and operation of the MSW treatment facility, and be conformable with the actual status of the MSW treatment service provider, infrastructure facilities, social – economic conditions and local-government budget.

3. Prices of MSW treatment services approved by competent authorities must be reasonable so as to attract and encourage investors of different economic sectors to invest in MSW treatment industry.

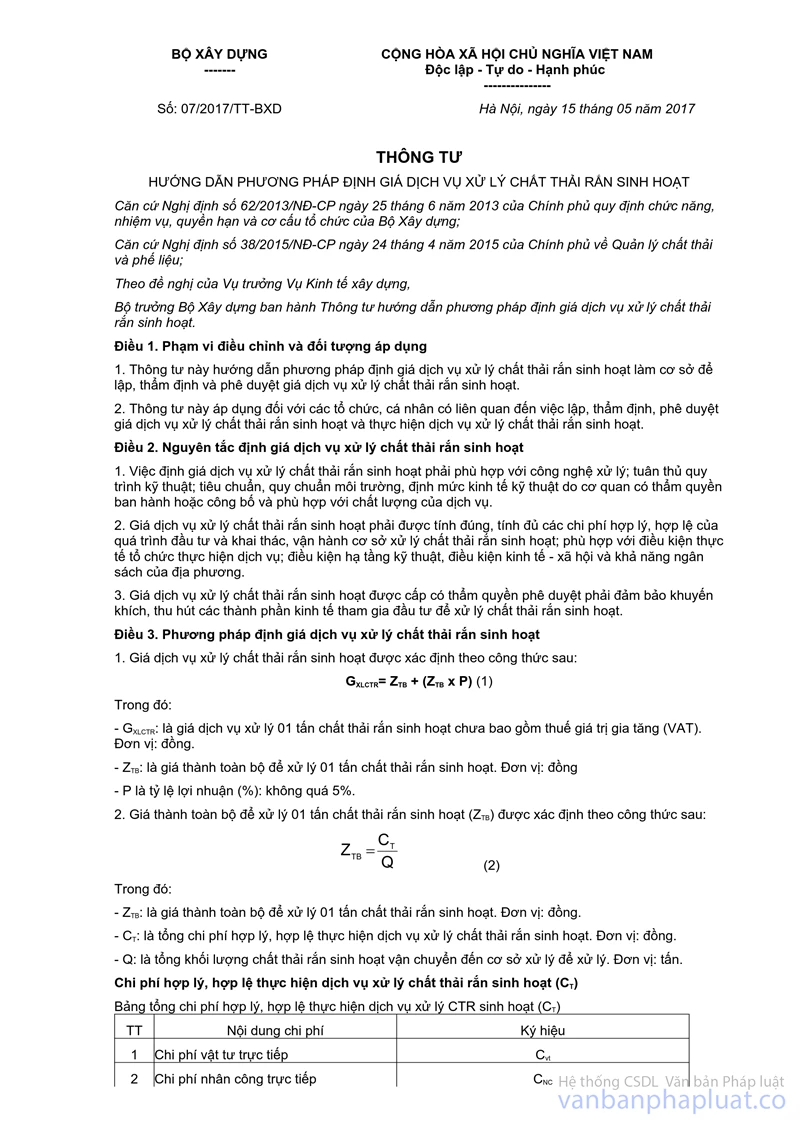

Article 3. Method for determining price of MSW treatment service

1. The price of MSW treatment service shall be determined by applying the following formula:

GXLCTR= ZTB + (ZTB x P) (1)

Where:

- GXLCTR: the price of service rendered for treatment of 01 ton of MSW, exclusive of VAT. Unit: VND

- ZTB: the prime cost for treatment of 01 ton of MSW. Unit: VND- P: profit rate (%), not exceeding 5%.

2. The prime cost for treatment of 01 ton of MSW (ZTB) shall be determined by applying the following formula:

![]() (2)

(2)

Where:

- ZTB: the prime cost for treatment of 01 ton of MSW. Unit: VND

- CT: the sum of reasonable costs for rendering the MSW treatment service. Unit: VND

- Q: total amount of MSW transported to the treatment facility. Unit: ton.

Reasonable costs for rendering the MSW treatment service (CT)

Summary of reasonable costs for rendering the MSW treatment service (CT)

|

No. |

Item |

Symbol |

|

1 |

Direct material cost |

Cvt |

|

2 |

Direct labour cost |

CNC |

|

3 |

Direct machinery and equipment cost |

CM |

|

4 |

Manufacturing overhead |

CSXC |

|

|

Total manufacturing cost |

Cp = Cvt + CNC + CM + CSXC |

|

5 |

General and administrative expenses |

Cq |

|

|

Total cost: |

CT = Cp+ Cq |

Where:

a) Direct material cost (Cvt) includes: costs of materials of various kinds directly used in the course of treating MSW. The cost of a type of material is equal to total quantity of such type of material multiplied by the unit price thereof. In which, the quantity of each type of material is determined according to relative technical regulations/ standards and norms of materials used for treating MSW as promulgated or announced by competent authorities. In case where a material consumption norm is not available, the entity in charge of preparing the pricing plan shall take charge of determining a reasonable material consumption norm to use as the basis for determining material costs in such pricing plan.

The material price is the actual price of material supplied to the MSW treatment facility which must be conformable with the current market price and specified in the price quotation or sales invoice in accordance with the law regulations applicable at the time of preparing the pricing plan. To be specific:

- If products processed from MSW are subject to VAT according to the credit-invoice method, the material price shall exclude VAT.

- If products processed from MSW are not subject to VAT or are subject to VAT according to the direct subtraction method, the material price shall include VAT.

b) Direct labor cost (CNC) includes: cash payments made by the MSW treatment facility to direct workers, consisting of: salaries, wages and salary allowances; social insurance, health insurance and unemployment insurance premiums payable, union dues and other payments made to direct workers involved in the process of MSW treatment.

Salary and wage expenses shall be equal to the number of working days, which is determined according to the direct labor cost norm in the field of MSW treatment promulgated or announced by a competent authority, multiplied by the corresponding salary or wage rate per day. The salary or wage rate per day of a direct employee who is directly involved in the process of MSW treatment shall be subject to decision of a competent authority (the Ministry of Labour, War Invalids and Social Affairs or the Provincial-level People's Committee). In case where the direct labor cost norm is not available, the entity in charge of preparing the pricing plan shall take charge of determining a reasonable direct labor cost norm to use as the basis for determining the direct labor cost in such pricing plan.

Social insurance premiums, health insurance premiums, unemployment insurance premiums, union dues and other payments made to workers who directly perform MSW treatment duties shall be determined in accordance with applicable law regulations (including amounts compulsorily paid by workers and those payable by the enterprise).

c) Direct machinery and equipment cost (CM) shall be determined according to machinery and equipment-shift rate, regulations on management, use and depreciation of machinery and equipment promulgated by the Ministry of Finance. The machinery and equipment-shift rate shall be determined according to the Ministry of Construction’s guidelines and relevant regulations. The period of time when depreciation may be spread out and which is determined according to machinery and equipment operating conditions should be taken into account when determining the direct machinery and equipment cost.

d) Manufacturing overhead (CSXC) includes indirect costs (other than the costs of direct materials, direct labor and direct machinery and equipment) incurred in the MSW treatment facility such as the costs of maintenance and repair of direct machinery and equipment, depreciation and repair of fixed assets (other than direct machinery and equipment), costs of indirect factory supplies and materials, salaries, wages, salary allowances, social insurance, health insurance and unemployment insurance premiums, and union dues of supervisors and workers in the factory (including amounts paid by workers and those payable by the enterprise), costs of environmental monitoring and surveys, rent on factory building (if any), costs of outsourcing services and other cash expenses which are included in the prime cost as prescribed by law.

The costs of materials and labor included in the manufacturing overhead are determined under the provisions on determination of costs of direct materials and direct labor specified in Clause a and Clause b of this Article.

The costs of depreciation and repair of fixed assets included in the manufacturing overhead are determined according to the Ministry of Finance’s regulations on management, utilization and depreciation of fixed assets.

dd) General and administrative expenses (Cq) include necessary costs for maintaining operations of the enterprise’s management and executive board and all expenses in general for the entire enterprise such as costs of depreciation and repair of fixed assets in service of the enterprise’s management and executive board, salaries, wages and salary allowances, social insurance, health insurance and unemployment insurance premiums, union dues of members of the management and executive board (including amounts paid by employees and those payable by the employer), costs of materials, office stationeries, taxes, fees and charges, outsourcing services rendered in the enterprise's office, other general expenses for the entire enterprise such as loan interests, provisions for devaluation of inventory, provisions for bad debts, costs of reception, transactions, scientific researches, technology research and innovation, costs for female workers, and other expenses classified as general and administrative expenses as prescribed by applicable law regulations.

The costs of materials and labor included in the general and administrative expenses are determined under the provisions on determination of costs of direct materials and direct labor specified in Clause a and Clause b of this Article.

The costs of depreciation and repair of fixed assets included in the general and administrative expenses are determined according to the Ministry of Finance’s regulations on management, utilization and depreciation of fixed assets.

The general and administrative expenses shall include all costs and expenses specified above but not exceed 5% of total manufacturing cost (Cp).

Article 4. Implementation organization

1. Prices of MSW treatment services shall be set, evaluated and approved by the entities and authorities prescribed in Clause 2 Article 26 of the Government's Decree No. 38/2015/ND-CP dated April 24, 2015.

2. Every Provincial-level People’s committee shall:

- Perform state management of MSW treatment services, and consider giving approval for prices of MSW treatment services rendered in the province.

- Submit relevant norms, unit prices and service prices announced or promulgated to the Ministry of Construction.

3. Prices of MSW treatment services determined and approved under the provisions herein shall be used as the basis for concluding and terminating contracts for provision of MSW treatment services. In case the determined price of MSW treatment service is higher than the MSW treatment cost announced by the Ministry of Construction, the Provincial-level People’s Committee is required to consult with the Ministry of Construction before giving approval for such service price.

4. Any agreements on adjustment of the price specified in the contract for provision of MSW treatment service signed by and between the MSW treatment facility's owner and a competent authority must be conformable with relevant laws and regulations.

5. With regard to effective contracts, contractual parties are required to consider changing or adjusting contract’s contents in conformity with regulations herein.

6. The entities in charge of preparing pricing plans and owners of MSW treatment facilities may hire qualified and experienced organizations or individuals to prepare or evaluate plans for prices of MSW treatment services which shall be used as the basis for evaluation and approval for suggested MSW treatment service prices.

7. The Ministry of Construction shall announce MSW treatment costs; take charge, instruct and inspect the preparation of pricing plans and implementation of regulations on management of prices of MSW treatment services by local governments.

Article 5. Entry into force

1. This Circular comes into force from July 01, 2017.

2. Difficulties that arise during the implementation of this Circular should be reported to the Ministry of Construction for consideration./.

|

|

PP. MINISTER |