Circular No. 02/2015/TT-BXD guidance on valuation of drainage service đã được thay thế bởi Circular 13/2018/TT-BXD guiding method for determination of drainage service prices và được áp dụng kể từ ngày 15/02/2019.

Nội dung toàn văn Circular No. 02/2015/TT-BXD guidance on valuation of drainage service

|

THE MINISTRY OF CONSTRUCTION |

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 02/2015/TT-BXD |

Hanoi, April 02, 2015 |

CIRCULAR

GUIDANCE ON VALUATION OF DRAINAGE SERVICE

Pursuant to the Government’s Decree No. 62/2013/NĐ-CP dated June 25, 2013 defining the functions, tasks, entitlements and organizational structure of the Ministry of Construction;

Pursuant to the Government’s Decree No. 60/2003/NĐ-CP dated June 06, 2013 providing instructions on the implementation of the Law on State Budget;

Pursuant to the Government’s Decree No. 130/2013/NĐ-CP dated October 16, 2013 on production and supply of public products and services;

Pursuant to the Government’s Decree No. 80/2014/NĐ-CP dated August 06, 2014 on drainage and wastewater treatment;

Pursuant to the Government’s Decree No. 177/2013/NĐ-CP dated November 14, 2013 providing instructions on the implementation of a number of articles of the Law on Price; At the request of Director General of Department of Construction Economics,

The Minister of Construction promulgates the Circular providing guidance on the valuation of drainage service.

Article 1. Scope and regulated entities

1. This Circular provides guidance on the valuation of drainage and wastewater treatment services (hereinafter referred to as drainage service price) for all types of drainage system as foundations for the establishment and decision on drainage service price applied in urban, industrial zones, economic zones, processing and exporting zones and hi-tech zones (hereinafter referred to as industrial zones) and concentrated rural residential areas.

2. This Circular applies to organizations, individuals and households at home, organizations and individuals abroad operating in the area of drainage in the territory of Vietnam; organizations, competent agencies that carry out formulation, consideration and decision on drainage service price.

3. Industrial complexes are encouraged to apply this Circular.

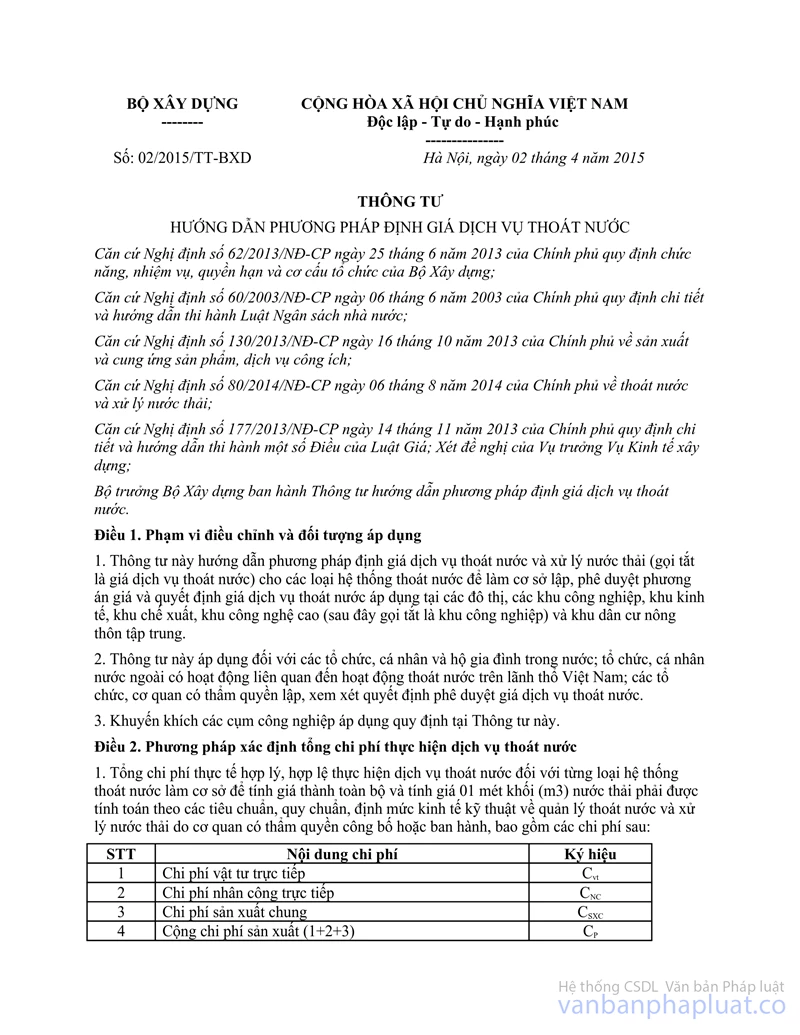

Article 2. Method of valuating total cost for implementation of drainage service

1. Total legitimate cost for the implementation of drainage service by each drainage system as foundations for the calculation of entire cost price of one cubic meter (m3) of wastewater shall be calculated on the basis of regulations, standards, economic and technical norms on management of drainage and wastewater treatment issued by competent agencies including:

|

No. |

Description |

Signs |

|

1 |

Direct material cost |

Cvt |

|

2 |

Direct labor cost |

CNC |

|

3 |

General production cost |

CSXC |

|

4 |

Total production cost (1+2+3) |

Cp |

|

5 |

Business management cost |

Cq |

|

6 |

Total drainage service cost (4+5) |

CT |

2. For drainage services performed in urban, industrial zones and concentrated rural residential areas, each cost item is determined as follows:

a) Direct material cost includes costs of raw materials, fuel, chemicals, motive power directly used, and secondary materials used for the implementation of drainage and wastewater treatment services.

Direct material cost is determined by multiplying total quantity of each material used by its corresponding unit price; of which:

- Quantity of materials used for drainage and wastewater treatment must conform with regulations, standards, economic and technical norms on drainage and wastewater treatment issued by competent agencies. For types of materials put into production without regulations, standards, economic and technical norms issued by competent agencies, the unit charged with building plan for drainage service price shall establish level of price based on its price plan and make the submission to People’s committees of provinces for approval.

- Material price is actual purchase price stipulated, instructed or announced by competent agencies at the time of calculation (for types of materials with price fixed and managed by the State in the following manners: price registration, price declaration, price negotiation and public disclosure of price information) or market price recorded in invoices according to law provisions at the time of calculation (for types of materials outside the list with price announced, instructed or stipulated by competent agencies) plus (+) appropriate cost of transport to the location of drainage, wastewater treatment (if any).

b) Direct labor cost includes expenses in cash paid to employees who are directly involved in the tasks by the drainage unit such as salaries, wages, shift meals, social insurance, medical insurance, unemployment insurance, trade union income and other expenses as prescribed for workers who are directly involved in drainage and wastewater treatment, of which:

- Salaries, wages are determined by multiplying the number of working days under economic and technical norms on drainage and wastewater treatment announced or issued by competent agencies by corresponding unit price of working day (unit price of working day includes basic pay, allowances according to law provisions);

- Expenses for shift meals (if any) to employees taking part in operation of business according to applicable regulations;

- Expenses for social insurance, medical insurance, unemployment insurance, allowances, trade union fee and other expenses (if any) paid to employees directly involved in the implementation of drainage and wastewater treatment according to applicable regulations;

c) General production cost is indirect production cost (apart from direct material cost and direct labor cost as prescribed in Points a, b, Clause 2 of this Article) including depreciation and repair of fixed assets; expenses for consumables, tools, equipment used in the workshop; wages, allowances, shift meals (if any) paid to employees; social insurance, medical insurance, unemployment insurance and trade union income paid to employees; expenses for test of standard of wastewater, discharge system, expenses for services hired outside and other expenses in cash entered into the cost price according to law provisions.

Method of determining expenses for materials, services, labor in general production cost is applied the same as cases prescribed in Points a, b, Clause 2 of this Article.

Cost of fixed asset depreciation is guided by regulations made by the Ministry of Finance on management of use and depreciation of fixed assets.

d) Business management cost is total expenses for business management and leading apparatus, expenses for business in general including depreciation and repair of fixed assets serving business management and leading apparatus; expenses for wages, bonus, allowances, shift meals (if any) paid to Board of directors and department managers; social insurance, medical insurance, unemployment insurance and trade union income paid to business management apparatus; expenses for materials and office supplies, taxes, fees and charges, expenses for outside services for business offices; other general expenses for entire business management such as loan interests, provisions against devaluation of goods in stock, provisions against doubtful debts, expenses for guest reception, transaction, scientific research, technological innovation research, invention, improvement, environmental protection, education, training, healthcare for employees, expenses for female employees and other management expenses according to applicable regulations. Business management cost is included in the cost price according to criteria appropriate for products of businesses such as treatment, drainage, construction, installation and other products of businesses (if any); other management cost according to applicable regulations.

Method of determination of expenses for materials, services, labor and fixed asset depreciation in the business management cost is instructed in accordance with Points a, b, c, Clause 2 of this Article.

3. When determining total production and business cost, the drainage unit must carry out adequate and accurate calculation of legitimate costs excluding expenses not entered as the expenses for production and business as prescribed in regulations on general method of valuation of goods and services issued by the Ministry of Finance and other relevant law provisions.

General expenses are used not only for drainage service but bear relation to a variety of activities of the drainage unit and such expenses shall be distributed in the accounting period in compliance with regulations on accounting and provisions set out hereof.

Article 3. Definition of drainage service price

1. Cost price for the entire one (01) cubic meter of wastewater is determined with the following formula:

|

ZTB = |

CT |

|

SLT |

Where:

a) ZTB: Cost price for the entire 01 cubic meter of wastewater on average; Unit: VND/m3

b) CT: Total expenses for drainage service determined according to Article 2 hereof;

c) SLT: Total amount of wastewater collected, transported and treated through the drainage system; Unit: m3

Total amount of wastewater collected, transported and treated through the drainage system includes wastewater from households and other types of wastewater discharged to the drainage system. In which, the amount of wastewater from households is determined according to Article 39 of the Government's Decree No. 80/2014/NĐ-CP dated August 16, 2014 on drainage and wastewater treatment; In case households who use clean water from the central water supply system install wastewater flow meters, amount of wastewater shall be calculated on the basis of such meters. Installation of wastewater flow meters by households (except domestic wastewater) is encouraged. Amount of other types of wastewater is calculated and determined according to applicable standards and regulations.

2. Cost price for the entire one (01) cubic meter of wastewater is determined with the following formula:

GDVTN = {ZTB + (ZTB x P)} x K

Where:

GDVTN: drainage service price

ZTB: Cost price for the entire 01 cubic meter of wastewater on average

P: Limit profit rate based on actual business conditions of drainage units and average income of local people in localities, the People’s committees of provinces shall regulate appropriate profit rate in the drainage service price structure and ensure at least 5% over the entire cost price

K: Adjustment coefficient pertaining to content of pollutants is determined according to content of pollutants contained in wastewater (not domestic wastewater) and determined according to criteria of COD (mg/l) of each type of wastewater based on nature of use or activities generating wastewater or separate subjects. Content of COD is determined on the basis of analysis results made by standard labs. Coefficient K is determined as follows:

|

No. |

Content of COD (mg/l) |

Coefficient K |

|

1 |

151 - 200 |

1,5 |

|

2 |

201 - 300 |

2 |

|

3 |

301 - 400 |

2,5 |

|

4 |

401 - 600 |

3,5 |

|

5 |

> 600 |

4,5 |

Drainage service price determined with the formula prescribed in Clause 2 of this Article excludes VAT.

Article 4. Implementation

1. The Ministry of Construction shall preside over inspection of the construction and promulgation of regulations on management of drainage service price in localities and inspection of the construction of price plan and compliance with the laws on drainage service price by drainage units under this Circular.

2. People’s committees of provinces shall be responsible for performing state administration on wastewater drainage in the administrative divisions within management; carrying out examination and approval for drainage service price between the drainage unit and owner of drainage systems to determine contractual price for management and operation; depending on particular socio-economic conditions in localities, People’s committees of provinces shall make decision on the itinerary and level of drainage service cost applied to households in the administrative divisions within management.

In case drainage service price in localities decided by People’s committees of provinces is lower than the drainage service price that is appropriately and accurately calculated with expenses for drainage services and appropriate profit rates included, People’s committees of provinces shall make compensations from local budget to ensure lawful rights if the drainage unit.

3. The Service of Construction shall preside over and cooperate with the Service of Finance, the Service of Natural Resources and Environment and relevant Services in inspecting the construction and implementation of drainage service price applied to relevant entities in the localities, acting as advisors for People’s committees of provinces on making immediate handling of difficulties arising and at the same time making the report to the Ministry of Construction for monitoring and revision if necessary.

4. Transitional handling shall be instructed in Article 47 of the Government's Decree No. 80/2014/NĐ-CP dated August 06, 2014 on drainage and wastewater treatment.

Article 5. Effect

1. This Circular takes effect since June 01, 2015.

2. Difficulties that arise during the implementation of this Circular should be reported (relevant agencies and units) to the Ministry of Construction for consideration and handling. /.

|

|

PP THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed