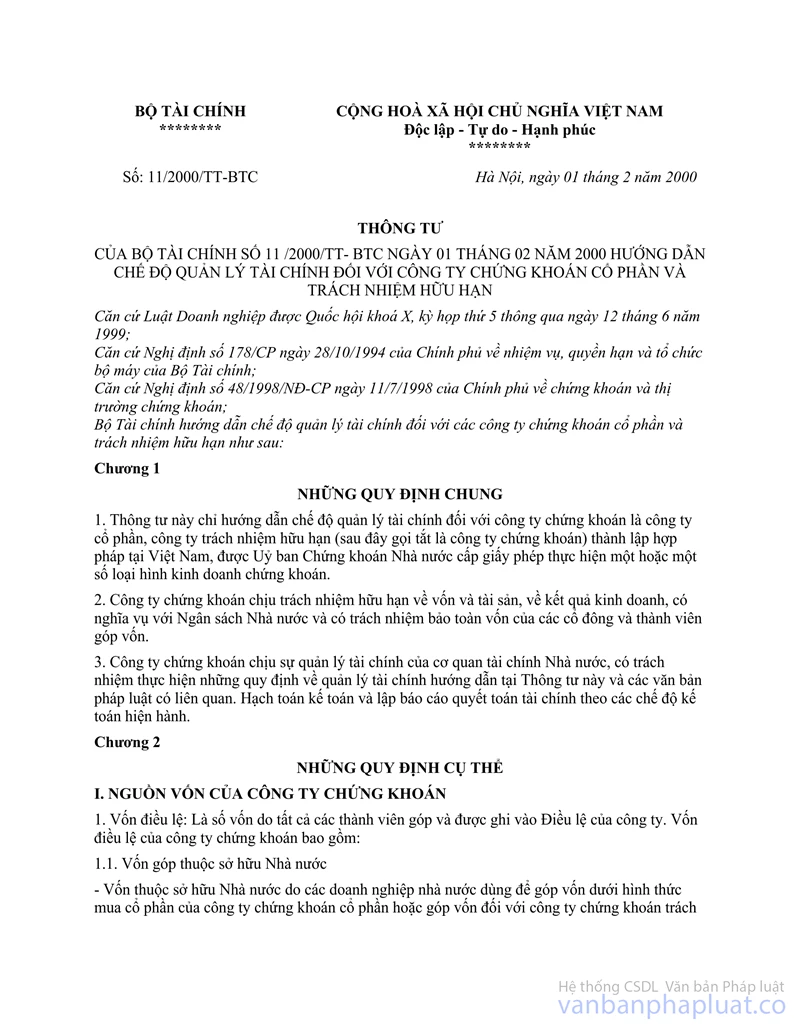

Circular No. 11/2000/TT-BTC of May 01, 2000, guiding the financial management regime applicable to joint-stock and limited liability securities companies đã được thay thế bởi Circular No. 146/2014/TT-BTC on finance regulations for securities companies asset management companies và được áp dụng kể từ ngày 21/11/2014.

Nội dung toàn văn Circular No. 11/2000/TT-BTC of May 01, 2000, guiding the financial management regime applicable to joint-stock and limited liability securities companies

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No: 11/2000/TT-BTC |

Hanoi, May 01, 2000 |

CIRCULAR

GUIDING THE FINANCIAL MANAGEMENT REGIME APPLICABLE TO JOINT-STOCK AND LIMITED LIABILITY SECURITIES COMPANIES

Pursuant to the Law on Enterprises passed on

June 12, 1999 by the Xth National Assembly at its 5th session;

Pursuant to the Government’s Decree No.178/CP of October 28, 1994 on the tasks,

powers and organizational structure of the Ministry of Finance;

Pursuant to the Government’s Decree No.48/1998/ND-CP of July 11, 1998 on

securities and securities market;

The Ministry of Finance hereby guides the financial management regime

applicable to joint-stock and limited liability securities companies, as

follows:

Chapter I

GENERAL PROVISIONS

1. This Circular guides only the regime of financial management applicable to securities companies being joint-stock companies or limited liability companies (hereafter referred to as securities companies), which are lawfully established in Vietnam and licensed by the State Securities Commission to conduct securities trading in one or several forms.

2. Securities companies take limited liability for their capital, assets and business results, have obligations toward the State budget and the responsibility to preserve capital of shareholders and capital contributors.

3. Securities companies are subject to financial management by the State finance agency, have to observe provisions on financial management guided in this Circular and relevant legal documents. They shall conduct the cost-accounting and accountancy and make financial settlement reports according to the current accounting regimes.

Chapter II

SPECIFIC PROVISIONS

I. CAPITAL SOURCES OF SECURITIES COMPANIES

1. Charter capital: is the capital amount contributed by all members of a securities company and inscribed in such company’s charter. The charter capital of a securities company includes:

1.1. Contributed State-owned capital, including:

- State-owned capital contributed by State enterprises by mode of purchasing shares of a joint-stock securities company or contributed to a limited liability company. This capital may be in cash, land use right value or land rental or value of other assets.

- Dividend amounts left by the contributing State enterprises to increase the securities company’s charter capital (if any).

- Source accumulated by the securities company through deduction for the setting up of the reserve fund for charter capital supplement, in proportion to State enterprises’ percentage of capital contribution to the securities company.

1.2. Contributed capital not owned by the State:

- Capital contributed by members, for limited liability companies, or share capital of shareholders, for joint-stock companies.

- Source accumulated by the securities company through deduction for the setting up of the reserve fund for charter capital supplement, in proportion to the percentage of capital contributed by members other than State enterprises.

- Dividends or yields from contributed capital divided to and left by members other than State enterprises to increase the securities company’s charter capital (if any).

2. Capital mobilized by the securities company, including:

- Capital mobilized through the issuance of shares (except for limited liability securities companies);

- Capital mobilized through the issuance of bonds;

- Capital borrowed from organizations within and without the country;

- Capital contributed by partners intended to set up joint-ventures and other forms.

3. Other capital sources (capital formed in the settlement process, entrusted investment capital, aid capital...).

4. Funds and interests created in the course of profit distribution.

The creation, mobilization, management and use of capital sources of the securities companies must comply with the State’s current regulations applicable to joint-stock companies and limited liability companies as well as regulations on securities trading activities.

II. PRESERVATION OF CAPITAL OF SECURITIES COMPANIES

Securities companies shall have to preserve their own capital by themselves, ensure safety for the capital contributors, ensure their liquidity in the course of operation, and raise the efficiency of capital use. The preservation of securities companies' capital shall be effected by the following modes:

1. Setting up of compulsory reserve funds according to provisions of Section IV, Clause 3, Chapter II of this Circular.

2. Reserves deducted as expenditures:

a/ Reserves for securities price decrease calculated upon each type of securities shall be deducted as follows:

|

Reserve level for securities investment Price decrease for the plan year |

= |

Volume of securities with decreased prices at Dec.31st of the reporting year |

x [ |

Price of securities accounted on accounting book |

- |

Closing price of Dec.31st or the latest closing price if Dec.31st is not a trading day |

] |

- Securities companies shall have to set aside reserve for each securities type with decreased price and may synthesize such reserves to serve as basis for accounting them into their operation expenditures.

- Securities price decrease reserves shall be accounted into operation expenditures of the reporting year for purpose of recording in advance the value of losses that may be incurred in the following year, and providing securities companies with a financial source to offset such losses, so as to preserve their business capital.

- Securities companies shall have to refund securities price decrease reserves into their incomes. The refunding of already set aside reserves and the setting aside of new ones shall be carried out at the time of closing accounting books for making annual financial statements.

b/ For reserves for risks arising in the payment process, the deduction level shall be equal to 0.1% of the total payment value.

3. Purchase of insurance for assets and other insurance types necessary for operations of securities companies

III. THE MANAGEMENT OF REVENUES AND EXPENDITURES OF SECURITIES COMPANIES

1. Revenues of a securities company include the followings:

a/ Revenues from business activities:

- Securities brokerage commission;

- Securities trading profits;

- Investment portfolio management charge;

- Revenues from issuance underwriting activities;

- Securities investment consultancy charge;

- Securities custody charge;

- Securities transaction charge;

- Dividends and yields from securities owned by the company.

b/ Revenues from financial activities, including: interests on deposits and revenues from other financial activities.

c/ Revenues from other activities:

- Revenues from lease of assets;

- Revenues from fines; from the recovery of already written off debts; refunded reserves deducted in the preceding year, which have been unused or have not been used up; liquidated, assigned or sold assets; and other revenues.

2. Expenditures of a securities company

a/ Securities trading expenses:

- Securities trading center membership fee (for securities companies being members of securities trading centers);

- Securities listing and registration charge (for securities companies issuing securities listed at securities trading centers);

- Share and bond custody charge;

- Securities transaction charge;

- Expenses for securities issuing agents;

- Share and bond relisting charge;

- Share and bond withdrawing charge;

- Via-account share and bond transfer charge;

- Share and bond consigning charge;

- Charge for use of equipment systems of securities trading centers;

- Postage, expenses for maintenance and repair of fixed assets, procurement of working tools, working trip allowance, loading-unloading costs and transport freight, expenses for treasury operations, expenses for inspection and auditing activities;

- Expenses for advertisement, marketing, sale promotion, guest reception, festive occasions, transactions, external relations, conferences and other expenses shall comply with the following regulations: For the first 2 years after the company establishment, the expense level must not exceed 7% of the total expenditures; from the third year on, it must not exceed 5% of the total expenditures;

- Fixed asset depreciation;

- Expenses for materials and tools;

- Charges for services purchased from outside;

- Wages and amounts of wage nature paid according to the current regime and prescriptions by the Managing Board;

- Such deductions set aside under the State’s regulations as: social insurance, medical insurance, trade union operating fund.

b/ Expenses for financial activities:

- Expenses for loan interest payment;

- Expenses for bond interest payment;

- Expenses for lease of assets to be used in business activities;

- Other expenses.

c/ Payment of taxes, charges and fees according to provisions of law.

d/ Other regular and reasonable expenses:

- Reserves set aside according to provisions of Section II, Chapter II of this Circular;

- Expenses for collection of fines according to the prescribed regime;

- Expenses for severance allowances paid to laborers as prescribed;

- Expenses for professional training;

- Expenses for mid-shift meals, provided that the expense level must not exceed the minimum wage level prescribed by the State for State employees;

- Expenses for liquidation, assignment and sale of assets;

- Expenses for property insurance and other necessary insurance types;

- Yearly dues to associations to which the securities company is a member;

- Other expenses.

3. Securities companies must not account into their expenditures the following:

- Damage already subsidized by the Government or compensated by the damage causing party(ies) or insurance agency;

- Fines paid for their administrative violations, violations of the environmental legislation, fines for overdue loans, fines for violations of financial regimes and other violations;

- Allowances for overseas working trips in excess of the level prescribed by the Managing Board;

- Expenditures from welfare fund and reward fund;

- Regular or irregular difficulty allowances, charity sums;

- Financial supports for mass organizations, societies and other agencies, excluding amounts in support of education activities outside the company, such as: contributions to the study promotion fund, assistance to disabled pupils;

- Expenses on capital construction investment and fixed asset procurement;

- Expenses covered by other funding sources.

IV. DISTRIBUTION OF PROFITS AND DEDUCTIONS FOR SETTING UP FUNDS

The profit of a securities company is determined as the difference of its total revenues minus (-) its total expenditures (including taxes prescribed by law). The arising profits shall also includes the preceding year’s profit amount, which is discovered in the year, minus the loss(es) already determined in the final settlement of the year according to the current regulations.

The profits earned in the year by a securities company shall, after payment of enterprise income tax as prescribed by law, be distributed in the following order:

1. Deducting fines for administrative violations in taxation, violations of the business registration regime, fines for overdue debts, fines for violations of the accounting and statistical regime, fines for breaches of economic contracts (after clearing off the standing amount between the actually collected fines and the imposed ones), and deductible regular expenses upon determination of payable enterprise income tax;

2. Making up for losses not yet cleared against pre-enterprise income tax profit;

3. After the above-said amounts are deducted, the remaining profit amount (assuming 100%) shall be distributed as follows:

- Deductions for setting up the reserve fund for charter capital supplement, which are equal to 5% of the annual net profit. Such fund shall be deducted till it is equal to 10% of the charter capital of the securities company;

- Deductions for setting up the compulsory reserve fund, which are equal to 5% of the annual net profit. Such fund shall be deducted till it is equal to 10% of the charter capital of the securities company;

- Dividing dividends, as for joint-stock securities companies (or dividing profit, as for limited liability securities companies) in proportion to the percentage of capital contributed by shareholders or capital-contributing members;

- Setting up other funds.

V. USE PURPOSES OF FUNDS

1. The reserve fund for charter capital supplement: shall be used to supplement and increase the charter capital, and expand business activities.

2. The compulsory reserve fund: shall be used to secure the safety of the securities companies and deal with force majeure circumstances.

Securities companies must not use the above-said funds to pay dividends.

3. Other funds: shall be used according to regulations of the Managing Board and in compliance with annual resolutions of the Shareholders’ Congress.

Chapter III

ACCOUNTING, STATISTICAL AND AUDITING WORK

1. The fiscal year of securities companies begins on January 1st and ends on December 31st of every calendar year.

2. Securities companies shall have to conduct the cost-accounting and accountancy, and make financial statements in strict accordance with the current accounting and statistical regime of the State.

3. Annually, securities companies must have their financial statements audited. The auditing activities shall be conducted by an independent auditing company after the latter is approved by the State Securities Commission.

4. Quarterly and annually, securities companies shall have to make and send their financial statements to the Ministry of Finance, tax agencies and the State Securities Commission. Quarterly statements must be sent within the first 15 days of the next quarter at the latest; annual statements must be sent within 45 days after the year ends.

a/ An annual statement of a securities company must contain the following documents:

- Report on operations in the year.

- Financial reports, including:

+ Accounting balance sheet

+ Report on business operation result

+ Report on monetary circulation

+ Explanation of financial statement

+ Report on capital resources and the use thereof

+ Report on deductions for setting up and use of funds, distribution of dividends.

b/ A quarterly statement must contain the following documents

- Accounting balance sheet

- Report on business operation result

- Report on monetary circulation

- Report on capital sources and the use thereof.

5. Within 45 days after the end of each fiscal year, the securities companies shall have to publicize their financial matters. Annual financial statements must be certified by independent auditors.

6. Depending on practical conditions, annually, the Ministry of Finance shall coordinate with the concerned agencies in examining the final financial settlements of securities companies if deeming it necessary.

Chapter IV

ORGANIZATION OF IMPLEMENTATION

This Circular takes effect after its signing. Any problems arising in the course of implementation must be promptly reported to the Ministry of Finance for consideration and solution.

|

FOR THE MINISTER OF FINANCE |