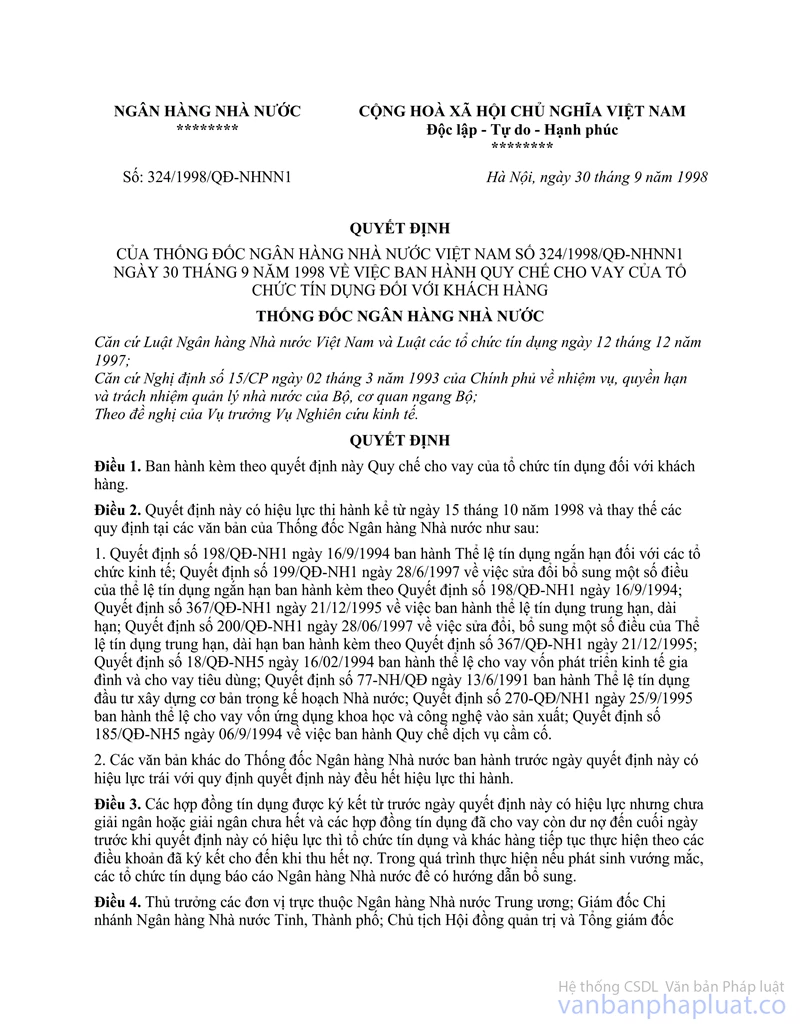

Decision No.324/1998/QD-NHNN1 of September 30, 1998 promulgating the regulation on loan provision to customers by credit institutions đã được thay thế bởi Decision No.284/2000/QD-NHNN1 of August 25, 2000 referring to the issuing of a regulation on credit institutions' lending và được áp dụng kể từ ngày 15/09/2000.

Nội dung toàn văn Decision No.324/1998/QD-NHNN1 of September 30, 1998 promulgating the regulation on loan provision to customers by credit institutions

|

THE STATE BANK |

SOCIALIST REPUBLIC OF

VIET NAM |

|

No. 324/1998/QD-NHNN1 |

Hanoi, September 30, 1998 |

DECISION

PROMULGATING THE REGULATION ON LOAN PROVISION TO CUSTOMERS BY CREDIT INSTITUTIONS

THE GOVERNOR OF THE STATE BANK OF VIETNAM

Pursuant to the Law on the State Bank of

Vietnam and the Law on Credit Institutions of December 12, 1997;

Pursuant to Decree No. 15-CP of March 2, 1993 of the Government on the tasks,

powers and State management responsibility of the ministries and

ministerial-level agencies;

At the proposal of the Head of the Economics Study Department,

DECIDES:

Article 1.- To issue together with this Decision the Regulation on loan provision to customers by credit institutions.

Article 2.- This Decision takes effect from October 15, 1998 and replaces the following legal documents issued by the Governor of the State Bank:

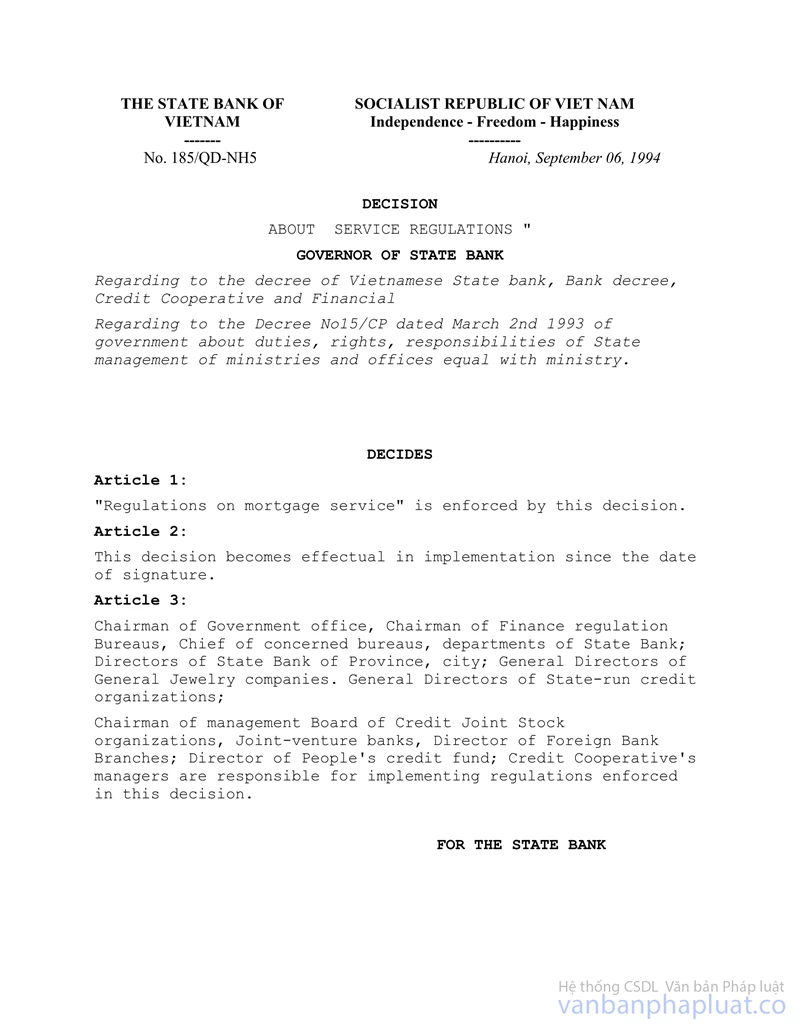

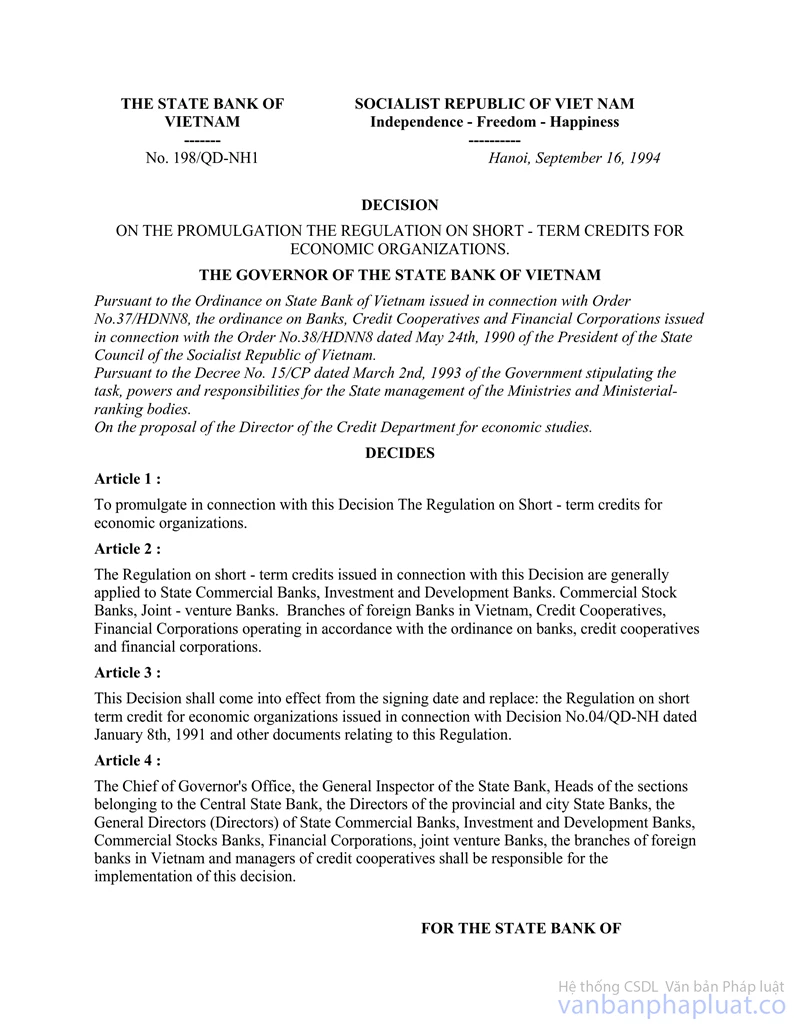

1. Decision No.198/QD-NH1 of September 16, 1994 promulgating the Regulation on short-term credits for economic organizations; Decision No.199/QD-NH1 of June 28, 1997 amending and supplementing a number of Articles of the Regulation on short-term credits issued together with Decision No.198/QD-NH1 of September 16, 1994; Decision No.367/QD-NH1 of December 21, 1995 promulgating the Regulation on medium- and long-term credits; Decision No.200/QD-NH1 of June 28, 1997 amending and supplementing a number of Articles of the Regulation on medium- and long-term credits issued together with Decision No.367/QD-NH1 of December 21, 1995; Decision No.18/QD-NH5 of February 16, 1994 promulgating the Regulation on lending capital for development of family household economy and consumption; Decision No.77-NH/QD of June 13, 1991 promulgating the Regulation on investment credit for capital construction according to the State plans; Decision No.270-QD/NH1 of September 25, 1995 promulgating the Regulation on lending capital for scientific and technological application to production; Decision No.185/QD-NH5 of September 6, 1994 promulgating the Regulation on pledge services.

2. Other legal documents issued by the Governor of the State Bank before this Decision takes effect and contrary to this Decision shall cease to be effective.

Article 3.- For credit contracts which have been signed before this Decision takes effect but the credit has not yet been disbursed or fully disbursed; and for credit contracts with credit already granted and with debit balances available by the end of the day before this Decision takes effect, the concerned credit institutions and their customers shall continue complying with the signed contracts till the full recovery of the loans. In the course of implementation, if any problems arise, they should be reported by the concerned credit institutions to the State Bank for additional guidance.

Article 4.- The heads of units attached to the Central State Bank; the directors of the State Bank’s branches in the provinces and cities; the chairmen of the managing boards and general directors (directors) of credit institutions and the customers who borrow capital from credit institutions shall have to implement this Decision.

|

THE

STATE BANK |

REGULATION

ON LOAN PROVISION TO CUSTOMERS BY CREDIT INSTITUTIONS

(Issued together with Decision No. 324/1998/QD-NHNN1 of September 30, 1998 of the Governor of the State Bank)

Chapter I

GENERAL PROVISIONS

Article 1.- Scope of regulation

This Regulation stipulates the provision of loans in Vietnam dong and foreign currencies by credit institutions to their customers in order to meet the latter’s demand of capital for production, business, services, development investment and people’s life.

Article 2.- Subjects of application

1. Credit institutions established and engaged in lending transaction under the Law on Credit Institutions.

2. Customers borrowing capital from credit institutions, including:

a/ Legal persons being State enterprises, cooperatives, limited liability companies, stock companies, foreign-invested enterprises and other organizations that fully satisfy conditions stipulated in Article 94 of the Civil Code;

b/ Individuals;

c/ Family households;

d/ Cooperation groups;

e/ Private enterprises;

Article 3.- Interpretation of terms:

In this Regulations the following terms shall be construed as follows:

1. Loan provision means a form of granting credit, under which a credit institution provides a customer with a sum of money for use for a certain purpose in a certain period of time as agreed upon on the principle of repayment of both principal and interest.

2. Loan term means a duration counted from the time a customer begins to receive the loan capital till the time both principal and interest are fully repaid, as agreed upon in the credit contract between the concerned credit institution and such customer.

3. Debt-repayment schedule mean different time periods within the loan term, by the end of each of which, as already agreed upon by a credit institution and a customer, the customer shall have to repay part or the whole of the loan to the credit institution.

4. Adjustment of debt-repayment schedule means a credit institution and a customer agree on adjusting the debt-repayment schedule which have earlier been agreed upon in the credit contract.

5. Loan extension means a credit institution accepts the extension of the loan term agreed upon in a credit contract for a certain period of time.

6. Investment project or business and/or production plan means a set of proposals on investing capital in production, business, services, development investment and improving people’s life within a certain period of time.

7. Credit limit means the maximum debit balance of outstanding loans, which is maintained for a certain period of time as agreed upon by a credit institution and a customer in the credit contract.

Article 4.- Implementation of the provisions on foreign exchange management

For foreign currency loans, credit institutions and their customers shall have to strictly abide by the Government’s regulations and guidance of the State Bank on foreign exchange management.

Chapter II

SPECIFIC PROVISIONS

Article 5.- The right to lending autonomy of credit institutions

Credit institutions shall take self-responsibility for their loan decisions. Neither organization nor individual is allowed to unlawfully interfere in the right to lending autonomy of credit institutions.

Article 6.- capital-borrowing principles

Customers borrowing capital from credit institutions shall have to comply with the following principles:

1. To use the loan capital for the right purpose(s) as agreed upon in the credit contracts;

2. To repay both principals and interests on schedule agreed upon in the credit contracts;

3. To ensure that the loan-security comply with the regulations of the Government and the Governor of the State Bank.

Article 7.- capital-borrowing conditions

A credit institution shall consider and decide to provide a loan for a customer if the latter fully satisfies the following conditions:

1. Having civil legal capacity and civil act capacity and taking civil liability as prescribed by law. More concretely:

a/ A legal person must have civil legal capacity;

b/ An individual or owner of a private enterprise must have legal capacity and civil act capacity;

c/ A family household’s representative must have legal capacity and civil act capacity;

d/ A cooperation group’s representative must have legal capacity and civil act capacity;

2. Having financial capability to ensure the full debt repayment within the committed time-limits;

3. Using loan capital for lawful purpose(s);

4. Having feasible/efficient investment project or business and/or production plan;

5. Complying with the loan-security regulations as provided for by the Government and guided by the State Bank.

Article 8.- Types of loans

1. Short-term loans: Credit institutions shall provide short-term loans to customers in order to meet the latter’s demand of capital for production, business, services and people’s life.

2. Medium- and long-term loans: Credit institutions shall provide medium- and long-term loans to customers so that the latter implement investment projects for the development of production, business and services and the improvement of people’s life.

Article 9.- Loan objects:

1. A credit institution shall provide loans on the following objects:

a/ The value of materials, goods, machinery, equipment and expenditures for a customer to implement project(s) or plan(s) on production, business, services, people’s life and development investment;

b/ The export tax amount to be paid by a customer to complete the export procedures for a lot of export goods in which the said credit institution is involved as a loan provider;

c/ The sum of loan interest payable to the credit institution within a project construction period, provided that such project has not been handed over and such immovable asset has not been put into use, regarding a medium- or long-term loan with payable interest included in the value of the immovable asset which has been invested with the loan capital.

2. A credit institution shall not be allowed to provide loans on the following objects:

a/ The payable tax amount, except for the export tax amount stipulated in Point b, Clause 1 of this Article;

b/ The sum of money to be paid for both loan principal and interest to another credit institution;

c/ The loan interest amount payable to the loan-providing credit institution itself, except for cases where such interest amount is provided as loan in accordance with the provisions of Point c, Clause 1 of this Article.

Article 10.- Loan terms

Credit institutions and customers shall reach agreement on loan terms, which may be either of the two following types:

1. Short-term loan: may be 12 months at most, determined according to the production and/or business cycle as well as the customer’s debt-repayment capability.

2. Medium- or long-term loans: shall be determined according to the capital retrieval duration of the investment project, the customer’s debt-repayment capability and the nature of the loan capital source of the concerned credit institution:

a/ Medium term: From 12 months to 60 months (5 years);

b/ Long term: From over 60 months or more but must not exceed the remaining operation duration prescribed in the establishment decision or establishment license of a legal person, and must not exceed 15 years, for loans to projects in service of people’s life.

Article 11.- Lending interest rates

1. The lending interest rates shall be agreed upon by credit institutions and customers in accordance with the State Bank’s stipulations on lending interest rates at the time their credit contracts are signed. The credit institutions shall have to make public different lending interest rates to the customers.

2. The preferential lending interest rates shall apply to those customers who are entitled thereto under the regulations of the Government and under the guidance of the State Bank.

3. In cases where a loan is transformed into an overdue debt, the interest rates set for overdue debts shall apply as provided for by the Governor of the State Bank at the time of signing the credit contract.

Article 12.- Loan amounts

Credit institutions shall, basing themselves on the customers capital demand, the maximum loan ratio compared with the value of the property used as loan security according to regulations of the Government and guidance of the State Bank, on customers’ debt-repayment capability as well as their respective capital sources, decide loan amounts, which must not exceed the limit defined in Article 79 of the Law on Credit Institutions.

Article 13.- Repayment of loan principals and interests

1. Basing themselves on the customers’ production, business and/or service characteristics as well as financial capabilities, incomes and debt-repayment sources, credit institutions and their customers shall reach agreement on the repayment of both loan principals and interests, including the following:

a/ The loan-principal repayment deadlines;

b/ The loan-interest payment deadlines, which may be the same as loan-principal repayment deadlines or be different;

c/ The to be-used currency(ies) for debt repayment and the guaranty of the loan principal’s value in appropriate forms as prescribed by law.

2. When a debt is due or upon the expiry of a loan term, if a customer fails to pay debt on schedule, is not entitled to the adjustment of the debt-repayment schedule or to the loan extension, the due debt must be transformed into an overdue debt and the customer shall have to pay the interest rate set for the overdue debt and calculated on the delayed amount.

3. In cases where the customer pays the debt before it is due, the credit institution and the customer shall reach agreement on the payable amount of loan interest, which must not exceed the amount already agreed upon in the credit contract.

Article 14.- capital-borrowing dossier

1. When having a demand for loan capital, a customer shall have to send to a credit institution the following documents:

- A written request for loan capital with the following main contents: the customer’s name and address; the capital amount to be borrowed; the capital-borrowing purposes; the commitments on the use of loan capital, repayment of both loan principal and interest and other commitments.

- The necessary documents proving that he/she/it satisfies the capital-borrowing conditions as stipulated in Article 7 of this Regulation;

The customer shall take responsibility before law for the accuracy and validity of the documents sent to the credit institution.

2. Credit institutions shall specify types of documents required from customers, based on the characteristics of each category of customers as well as each type of loans in accordance with the provisions in Clause 1 of this Article.

Article 15.- Loan evaluation and decision

1. Credit institutions shall elaborate procedures for considering and approving loans on the principle of ensuring the autonomy and clearly determining the personal responsibility as well as the joint-responsibility of the persons in charge of loan evaluation and decision.

2. Credit institutions shall examine the customers’ documents and at the same time evaluate the feasibility and efficiency of investment projects or production and/or business plans as well as the customers’ debt-repayment capabilities.

Where necessary or prescribed by law, credit institutions may set up a credit council or hire a relevant consulting agency to evaluate customers’ investment projects or production and/or business plans.

3. Within 10 working days for short-term loans and 45 working days for medium- and long-term loans, after receiving the full and valid capital-borrowing dossier as well as necessary information provided by a customer at its request, a credit institution shall have to decide and notify the customer of the approval or non-approval of the loan. If refusing to provide loan to the customer, the credit institution shall have to notify in writing the customer thereof, clearly stating the reasons therefor.

Article 16.- Lending modes

A credit institution shall reach agreement with its customer on the lending mode, suited to the customer’s capital demand and the institution’s capability to inspect and supervise the use of loan capital. The lending mode may be one of the following:

1. Single loan: For each capital borrowing, a customer and the concerned credit institution shall proceed with necessary procedures and sign a credit contract.

2. Loan based on the limit of credit: A credit institution and its customer shall define and agree on a limit of credit to be maintained in a certain period of time or according to a production/business cycle.

3. Loan based on investment project: A credit institution shall provide loan to a customer for the latter’s implementation of investment project(s) on developing production, business, services and improving people’s life.

4. Loan participation: A group of credit institutions provide loan for a customer’s capital-borrowing project or plan; one of these credit institutions shall act as coordinator for the management and coordination with other institutions. The loan participation shall be effected in accordance with this Regulation and the Regulation on Co-Financing by Credit Institutions, issued by the Governor of the State Bank.

5. Installment loan: When providing loan, a credit institution and its customer shall determine and agree on the payable sum of both loan principal and interest, which shall be divided for repayment in different installments by the customer within the loan term. The property purchased with loan capital shall belong to the borrower’s ownership only when such borrower fully repays both loan principal and interest.

6. Loan based on the reserve credit limit: A credit institution shall commit itself to get ready to lend capital to a customer within a certain limit of credit. The credit institution and customer shall reach an agreement on the effective time-limit of the reserve credit limit as well as the level of fee to be paid therefor.

7. Loan through the issuance and use of credit cards: A credit institution may allow its customer to use the loan capital within the credit limit to pay for the purchased goods and services and withdraw money from automatic telling machines or from cash-distributing agents of such credit institution. When providing loan with the issuance and use of credit cards, the credit institution and its customer shall have to abide by the regulations of the Government and the State Bank on the issuance and use of credit cards.

8. Other lending modes shall comply with the provisions of this Regulations and other stipulations of the State Bank.

Article 17.- Foreign currency loans

1. Borrowers: Credit institutions involved in foreign exchange transactions shall be entitled to provide foreign currency loans to customers for the latter’s payment to foreign parties for materials, goods, machinery, equipment and services imported for the customers’ production and/or business activities. The provision of foreign currency loans to borrowers other than those defined above must be approved in writing by the Governor of the State Bank.

2. Capital-borrowing dossier: In addition to the documents stipulated in Article 14 of this Regulation, a customer shall also have to send to the concerned credit institution the following: the import permit or import quota (if any); the import or entrusted import contract and other documents related to the use of loan capital.

3. Repayment of loan principal and interest: A loan in foreign currency must be paid in such currency. In cases where the loan is repaid in another currency or Vietnam dong, such repayment shall be effected according to the agreement between the credit institution and the customer and the currency conversion shall be based on the foreign exchange rate or on the principle for determining foreign exchange rate as agreed upon in the credit contract. Foreign-invested enterprises which have to balance their foreign currency demands by themselves shall not be allowed to repay foreign currency loans in Vietnam dong.

Article 18.- Credit contracts

After deciding a loan, a credit institution and its customer shall sign a credit contract. The credit contract must contain the loan conditions, the loan-use purposes, the ways of loan capital disbursement and use, the loan amount, the interest rate, the loan term, the debt-repayment mode and deadline, the loan security form, the value of the security property, the measures for handling the security property, the transfer or non-transfer of the credit contract and other commitments as agreed upon by the involved parties.

Article 19.- Loan limits

1. The total debit balance of outstanding loans for a customer shall not exceed 15% of the own capital of a credit institution, except for loans from the trust fund sources of the Government, organizations and individuals. In cases where a customer’s capital demand exceeds 15% of the own capital of a credit institution or the customer has the need to mobilize capital from various sources, the credit institutions may jointly provide loans in accordance with the regulations of the Governor of the State Bank.

2. In special cases, a credit institution’s loan may exceed the loan limit stipulated in Clause 1 of this Article but only when so permitted by the Prime Minister on a case-by-case basis.

3. The determination of a credit institution’s own-capital amount to serve as basis for calculating the loan limit as stipulated in Clauses 1 and 2 of this Article shall comply with the regulations of the State Bank.

Article 20.- Cases where loans are not provided

1. A credit institution shall not be allowed to provide loans to the following subjects:

a/ Members of the Managing Board and Control Commission, the General Director (Director), Deputy General Director (Deputy Director) of the credit institution;

b/ The person who evaluates and approves loans;

c/ Father, mother, wife, husband or children of a member of the Managing Board or Control Commission, the General Director (Director), or the Deputy General Directors (Deputy Directors).

2. The provisions of Clause 1 of this Article shall not apply to cooperative credit institutions.

Article 21.- Loan restrictions

1. A credit institution shall not be allowed to provide loans without security, or with preferential conditions on interest rates or loan amounts to the following subjects:

a/ The auditing organizations and auditors that are auditing such credit institution; the chief accountant and inspectors;

b/ Major shareholders of the credit institution;

c/ An enterprise where one of the subjects specified in Clause 1, Article 77 of the Law on Credit Institutions owns more than 10% of the enterprise’s statutory capital.

2. The total debit balance of outstanding loans for the subjects prescribed in Clause 1 of this Article must not exceed 5% of the own capital of the credit institution.

Article 22.- Inspection and supervision of loan capital

1. A credit institution shall have to inspect and supervise the borrowing, use and repayment of loan capital by its customers.

2. A credit institution shall conduct the inspection and supervision before, during and after the lending, suited to its operation characteristics as well as the customer’s business characteristics and his/her/its use of loan capital.

Article 23.- Loan extension and adjustment of debt-repayment schedules

1. If a debt is due but the customer fails to fully repay it due to objective causes and there’s a written proposal for loan extension, the concerned credit institution shall consider and decide the loan extension in accordance with the following stipulations:

a/ The extended duration of a short-term loan shall not be longer than the pre-extension loan term already agreed upon or shall be equal to a production/business cycle but must not exceed 12 months.

b/ The extended duration of a medium- or long-term loan shall not be longer than half of the pre-extension loan term already agreed upon in the credit contract.

c/ If a due debt can neither be paid nor extended, it must be transformed into an overdue debt and the overdue-debt interest rate shall apply.

2. In cases where a customer fails, due to objective causes, to repay the debt on schedule as agreed upon in the credit contract and submits a written request for the adjustment of debt-repayment time-limit(s), the concerned credit institution shall consider such adjustment. If the debt-repayment schedule cannot be adjusted, the credit institution shall transform the due debt into an overdue debt.

3. A customer’s request for loan extension and/or debt-repayment schedule adjustment and the approval thereof by a credit institution must be effected before the debt comes due and the involved parties may agree on the supplements to the credit contract according to the new debt-repayment schedule.

4. For extended loans and loans with adjusted debt-repayment schedules, the interest rates already agreed upon in the credit contracts for the undue debts shall still apply till the end of the extended duration or of the adjusted schedule.

Article 24.- Exemption or reduction of loan interest

A credit institution shall be entitled to decide the exemption or reduction of the loan interest to be paid to it by a customer, on the following principles:

1. The customer suffers from property losses related to the loan capital due to objective causes, thus leading to his/her/its financial difficulties;

2. The level of loan interest exemption and/or reduction shall depend on the financial capability of the credit institution;

3. A credit institution must not exempt or reduce loan interests for customers being subjects prescribed in Clause 1, Article 78 of the Law on Credit Institutions.

4. Credit institutions shall have to issue regulations on loan interest exemption or reduction for customers, which must be ratified by their respective Managing Boards. The loan interest exemption or reduction for customers shall be effected only after the promulgation of the regulation on loan interest exemption or reduction by the concerned credit institution.

Article 25.- Rights and obligations of customers

1. A customer-borrower shall have the right:

a/ To refuse to meet a credit institution’s requirements which vary with the agreements in the credit contract;

b/ To complain or initiate a lawsuit about any breach of the credit contract according to law.

2. A customer-borrower shall have the obligation:

a/ To fully and honestly provide information and documents related to the borrowing and take responsibility for the accuracy of such information and documents;

b/ To use the loan capital for the right purpose(s) and according to the contents agreed upon in the credit contract;

c/ To repay both debt principal and interest as agreed upon in the credit contract;

d/ To take responsibility before law for his/her/its failure to comply with the debt- repayment agreements and fulfill the obligations on loan security as already committed in the credit contract.

Article 26.- Rights and obligations of credit institutions

1. A credit institution shall have the right:

a/ To request customers to provide documents proving the feasibility of their investment projects or production/business plans as well as the financial capabilities of the customers and the guarantors before deciding the loans;

b/ To reject a customer’s request for a loan if such customer is deemed unqualified for the loan, or his/her/its project or plan proves inefficient or contrary to the provisions of law or if the credit institution itself does not have enough capital sources for loans;

c/ To inspect and supervise the process of capital borrowing, using and debt repayment by customers;

d/ To terminate a loan and retrieve debt before schedule if detecting that the customer has provided untrue information or has breached the credit contract;

e/ To initiate a lawsuit against a customer if the latter breaches the credit contract or against the guarantor in accordance with the provisions of law;

f/ When a debt is due, if the involved parties do not reach any other agreement, the concerned credit institution shall be entitled to sell the security property as agreed upon in the contract to recover the loan in accordance with the provisions of law, or request the guarantor to fulfill his/her/its guaranteeing obligation, in cases where a customer borrows capital with guaranty.

g/ To exempt or reduce the loan interest, extend a loan, adjust the debt-repayment schedule, purchase or sell debts according to the regulations of the State Bank and effect the debt roll-over, debt freezing or debt cancellation in accordance with the regulations of the Government.

2. Credit institutions shall have the obligation:

a/ To strictly abide by agreements in the credit contracts;

b/ To keep the credit dossiers in accordance with the provisions of law.

Article 27.- Provision of soft loans and loans for investment and construction according to the State’s plans

1. Credit institutions shall provide loans to customers who are entitled to preferential credit policies according to the regulations of the Government stipulations and the guidances of the State Bank in each period.

2. State credit institutions shall provide loans for investment and construction according to the State’s plans under the law provisions on investment and construction as well as the Government’s regulations on investment and construction credit according to annual State plans.

3. For State credit institutions nominated by the Government to provide loans for customers that are entitled to preferential treatment and loans for investment and construction according to the State’s plans, if there have appeared any interest rate differences or loss to the loans due to objective causes, the handling thereof shall comply with the Government’s regulations and the State Bank’s guidance as well as the regulations of concerned ministries and branches.

4. Before providing a soft loan or loan for investment and construction according to the State’s plan, a credit institution shall evaluate the efficiency of the related project or plan and if such project or plan is deemed inefficient and the borrower is unable to repay the loan principal and interest, such credit institution shall report it to the competent State agency(ies) and, if necessary, to the Prime Minister for consideration and decision.

Article 28.- Trust loans

1. Credit institutions shall provide loans as entrusted by the Government, organizations or individuals inside and outside the country under the trust loan contracts signed with the representative agency(s) of the Government or of the concerned domestic or foreign organizations or individuals. The trust loan provision must comply with the provisions of the legislation on credit and banking and trust contracts.

2. Credit institutions providing trust loans shall enjoy trust fee and other benefits as agreed upon in the trust loan contracts, in accordance with the provisions of international law and practices, so as to cover their expenses and risks and also to earn profits.

Chapter III

IMPLEMENTATION PROVISIONS

Article 29.- Credit institutions and capital borrowers shall have to implement this Regulation. Basing themselves on this Regulation and the relevant legal documents, credit institutions shall issue documents providing detailed professional guidance in accordance with their own conditions, characteristics and statutes.

Article 30.- Organizations and/or individuals that violate this Regulation shall, depending on the nature and seriousness of their violations, be disciplined, administratively handled or examined for penal liability according to law.

Article 31.- Any amendments or supplements to this Regulation must be decided by the Governor of the State Bank.