Nội dung toàn văn Decision No. 39/2000/QD-TTg of March 27, 2000, stipulating temporary tax preferences for securities trading activities

|

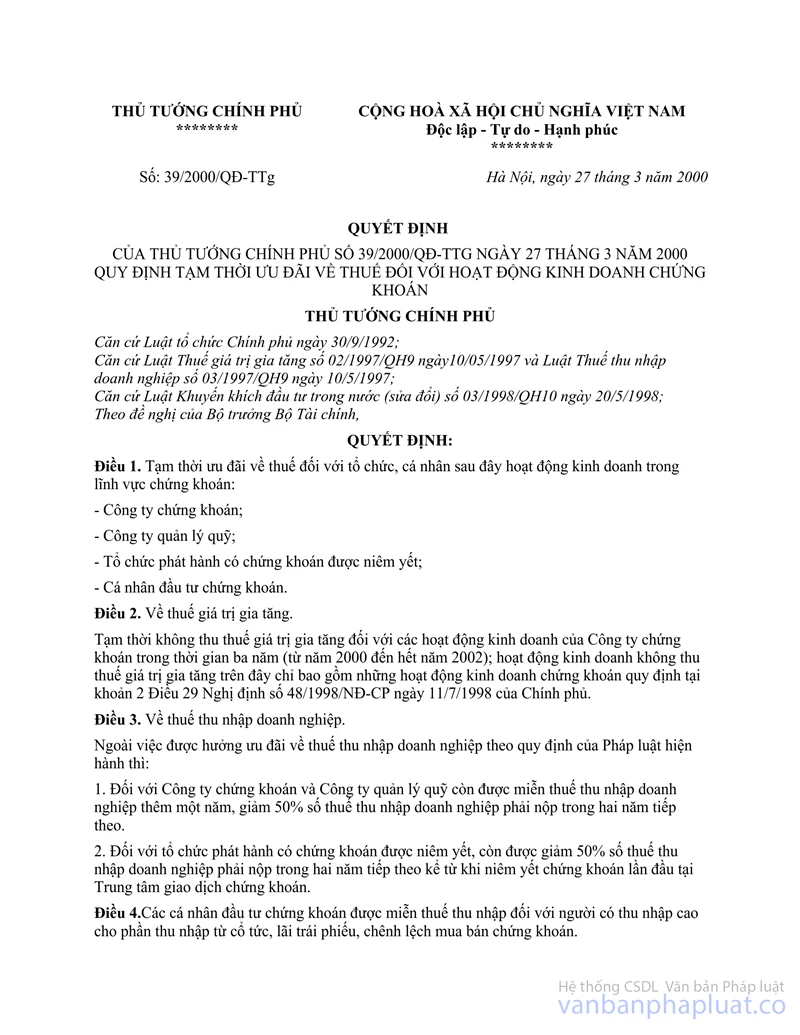

THE PRIME MINISTER OF GOVERNMENT |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 39/2000/QD-TTg |

Hanoi, March 27, 2000 |

DECISION

STIPULATING TEMPORARY TAX PREFERENCES FOR SECURITIES TRADING ACTIVITIES

THE PRIME MINISTER

Pursuant to the Law on

Organization of the Government of September 30, 1992;

Pursuant to Value Added Tax Law No. 02/1997/QH9 of May 10, 1997 and Enterprise

Income Tax Law No. 03/1997/QH9 of May 10, 1997;

Pursuant to Domestic Investment Promotion Law No. 03/1998/QH10 of May 20, 1998

(amended);

At the proposal of the Minister of Finance,

DECIDES:

Article 1.- To temporarily provide tax preferences for the following organizations and individuals conducting business activities in the field of securities:

- The securities companies;

- The fund-managing companies;

- The issuing organizations with listed securities;

- Securities investing individuals.

Article 2.- On the value added tax

Temporarily not to collect the value added tax on the business activities of the securities companies for three years (from 2000 to the end of 2002); the above-mentioned business activities, on which the value added tax is not collected, include only the securities trading activities specified in Clause 2, Article 29 of the Government’s Decree No. 48/1998/ND-CP of July 11, 1998.

Article 3.- On the enterprise income tax

Apart from the enjoyment of preferential enterprise income tax according to the current regulations:

1. The securities companies and the fund-managing companies shall be entitled to enterprise income tax exemption for one more year and 50% reduction of payable enterprise income tax for two subsequent years.

2. The issuing organizations with listed securities shall be entitled to 50% reduction of payable enterprise income tax for two subsequent years as from the time the securities are firstly listed at the securities trading center.

Article 4.- Securities investing individuals shall be exempt from income tax on high-income earners for the incomes from devidend, bond interests and differences between securities purchase and sale.

Article 5.- Securities trading organizations or individuals shall comply with other current law provisions on tax apart from the preferences specified in Articles 2, 3 and 4 of this Decision.

Article 6.- This Decision takes effect 15 days after its signing.

Article 7.- The Minister of Finance shall have to guide the implementation of this Decision.

The ministers, the heads of the ministerial-level agencies, the heads of the agencies attached to the Government, the presidents of the People’s Committees of the provinces and centrally-run cities shall have to implement this Decision.

|

|

FOR THE PRIME MINISTER |