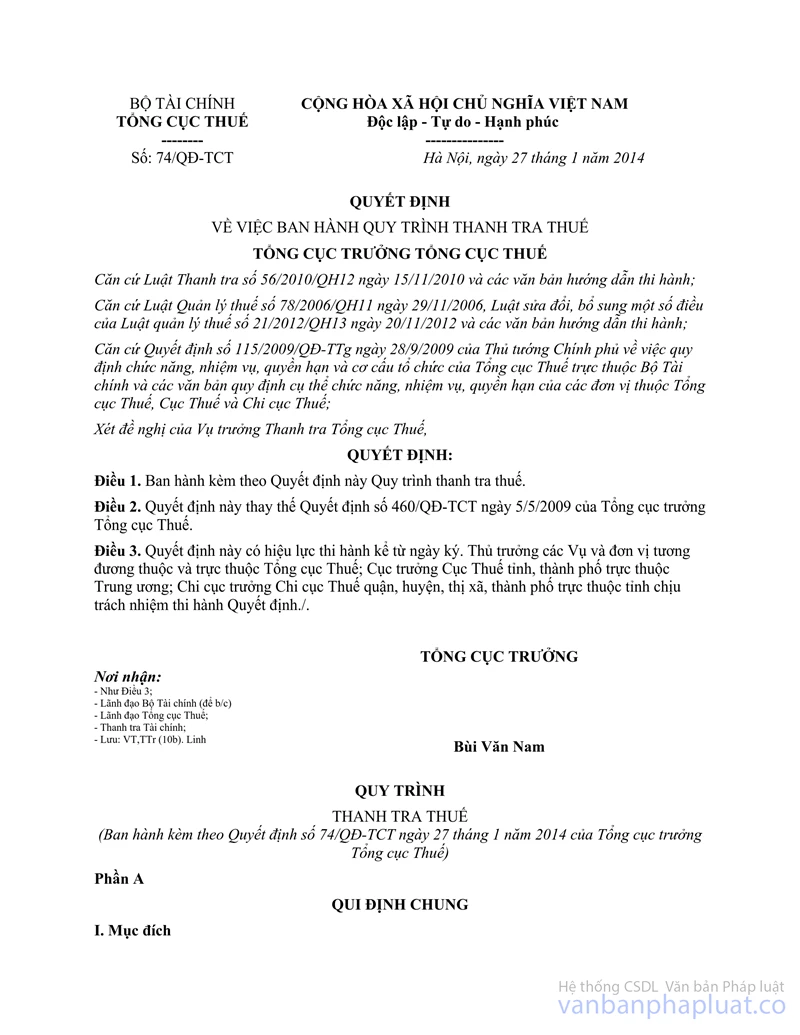

Decision No. 74/QD-TCT dated 2014 on promulgation of procedure for tax inspection đã được thay thế bởi Decision 1404/QD-TCT 2015 on issuance of tax inspection procedure và được áp dụng kể từ ngày 28/07/2015.

Nội dung toàn văn Decision No. 74/QD-TCT dated 2014 on promulgation of procedure for tax inspection

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 74/QD-TCT |

Hanoi, January 27, 2014 |

DECISION

ON PROMULGATION OF PROCEDURE FOR TAX INSPECTION

DIRECTOR OF THE GENERAL DEPARTMENT OF TAXATION

Pursuant to the Law on Inspection No. 56/2010/QH12 dated November 15, 2010 and guiding documents;

Pursuant to the Law on Tax administration No. 78/2006/QH11 dated November 29, 2006, the Law on the amendments to the Law on Tax administration No. 21/2012/QH13 dated November 20, 2012 and guiding documents

Pursuant to the Decision No. 115/2009/QD-TTg dated September 28, 2009 of the Prime Minister defining the functions, tasks, entitlements and organizational structure of the General Department of Taxation affiliated to the Ministry of Finance and documents defining specific functions, tasks, powers of the units affiliated to the General Department of Taxation, Provincial Departments of Taxation and Sub-Departments of Taxation;

At the request of the Director of the Inspectorate of the General Department of Taxation,

DECIDE

Article 1. The Procedure for the tax inspection is issued together with this Decision.

Article 2. This Decision replaces the Decision No. 460/QD-TCT of the Director of the General Department of Taxation dated May 05, 2009.

Article 3. This decision takes effect as of the signing date. The directors of the Departments and equivalent units affiliated to General Department of Taxation, Directors of the Departments of Taxation of central-affiliated cities and provinces (hereinafter referred to as provinces), Directors of the Sub-Departments of taxation of districts shall implement this Decision./.

|

|

DIRECTOR OF GENERAL DEPARTMENT OF TAXATION |

PROCEDURE

TAX INSPECTION

(Issued together with the Decision No. 74/QD-TCT of the Director of the

General Department of Taxation dated January 27, 2014

PART A

GENERAL PROVISIONS

I. Aims

Standardize the tax inspection tasks.

Ensure that the tax inspection activities are conducted under the regulations of the laws and uniform across the General Department of Taxation, Provincial Departments of Taxation and Sub-Departments of Taxation and, which meets the requirements for the reform and modernization of tax.

Enhance the competence to conduct tax inspection activities, ensure that the tax inspections are objective, open and transparent.

II. Scope of regulation

This Procedure regulates the consistent procedures for the tax inspection activities and applied to the regulatory authorities, including: Formulation of plan for annual inspection; Inspection at premises of taxpayers; entering data on inspection and report.

III. Regulated objects

The Procedure for the tax inspection shall apply to Heads of the tax authorities, Inspection divisions, persons in charge of inspection under the management of General Department of Taxation, Provincial Departments of Taxation, Sub-Departments of Taxation.

This Procedure for the tax inspection shall not apply to the inspection activities of the officials in charge of tax inspection conducting independent inspections.

IV. Interpretation of terms

These terms are construed as follows:

1. Tax inspection divisions: Inspectorate of the General Department of Taxation; Inspection offices under the management of the Provincial Departments of Taxation; Inspection units under the management of the Sub-Departments of the Taxation.

2. Heads of the Inspection divisions: Director and Deputy Director of the Inspectorate of the General Department of Taxation, Heads and Deputy Heads of the inspectorates of the Provincial Departments of Taxation, Heads and Deputy Heads of the Sub-Departments of Taxation.

3. Heads of the tax authorities: Director of the General Director of Taxation and Sub Directors; Directors and Deputy of Directors of the Provincial Departments of Taxation, Directors and Deputy Directors of the Sub-Departments of Taxation.

4. Tax authorities: The General Department of Taxation, Provincial Departments of Taxation and Sub-Departments of Taxation.

5. Persons in charge of tax inspection are the eligible officials of the authorities assigned to conduct tax inspections in accordance with the regulations in Article 12 of the Decree No. 07/2012/ND-CP of the Government dated February 09, 2012 (hereinafter referred to as tax inspectors)

6. The time which is expressed as “day” is the days in the solar calendar (including the days off under the regulations).

7. The time which is expressed as “working day” is the working days of the State administrative agencies (excluding the days off under the regulations).

8. The inspection divisions make plans for the tax inspections. In case a tax authority has more than one inspection division, the Head of such tax authority shall assign one inspection division to take charge of making plans for the inspections, summarize and report the inspections.

PART B

CONTENTS OF PROCEDURE

I. Formulation of annual inspection plans

1. Preparation for formulation of annual inspection plans

1.1. Collection of information about taxpayers

The tax inspection divisions shall collect the information about the taxpayers from:

a) The information and data on the taxpayers from the tax authorities (including the databases on the tax information system and other data) including:

- Tax statements, tax refund dossiers, documents on the invoices and other documents that the tax payers must send to the tax authorities under the regulations of the laws.

- Financial statements of the taxpayers.

- Information about the financial and business conditions of the taxpayers;

- Information about the adherence to the laws on taxation of the taxpayers: declaration and tax payment; results of tax inspections, results of the tax inspections in the previous year; tax exemption and reduction…

- Other information (if any)

b) The information and data on the taxpayers from other authorities (if any): Information provided by the State Audit; Government Inspectorate; competent authorities affiliate to the Ministries, Regulatory authorities, Trade Association; media agencies; Information from the tax evasion reports and tax fraud...

1.2. Orientation to formulation of inspection plan

The General Department of Taxation shall issue the guiding documents on the formulation of the tax inspection plan by October every year according to the instructions on the financial inspections given by the Ministry of Finance and the requirements for the tax administration.

The Provincial Departments of Taxation shall issue the guiding documents on the formulation of the tax inspection plans to the Tax inspection divisions of the Provincial Departments of Taxation and Sub-Departments of Taxation by October 31 according to the guiding documents on the formulation of the tax inspection plan issued by the General Department of Taxation.

2. Formulation and approval for annual inspection plans

2.1. At General Department of Taxation

2.1.1 With regard to inspection plan of General Department of Taxation

- The Inspectorate of the General Department of Taxation shall make a list of taxpayers in descending order according to the level of risks, put it into the annual inspection plan of the General Department of Taxation and submit it to the Director of the General Department of Taxation according to the requirements for the tax administration and guiding documents on the formulation of the annual inspection plan of the Ministry of Finance.

- The Director of the General Department of Taxation shall approve the list of taxpayers, put it into the annual inspection plan of the General Department of Taxation and send it to the Inspectorate of the Ministry of Finance not later than November 01 every year.

- The Inspectorate of the General Department of Taxation shall request the Director of the General Department of Taxation to notify the annual inspection plan of the General Department of Taxation to the Provincial Departments directly supervising the inspected entities to cooperate in implementing according to the decisions of the Minister of Finance on the approval for the annual inspection plan.

2.1.2. Approval for inspection plans of Provincial Departments of Taxation

The Inspectorate of the General Department of Taxation shall request the Director of the General Department of Taxation to sign the Decision on the approval and decide the number of the taxpayers to be put into the annual tax inspection plans of the Provincial Departments of the Taxation not later than the December 15 using the form 01/QTTTr issued together with this Procedure according to the applications for the approval for the annual inspection plans sent by the Provincial Departments of Taxation.

2.2. At Provincial Departments of Taxation

2.2.1 With regard to inspection plans of Provincial Departments of Taxation

The tax inspection divisions shall submit the applications for the approval for the annual inspection plans and send them to the General Department of Taxation (the Inspectorate of the General Department of Taxation) before November 25 every year according to the requirements for the tax administration and guiding documents. An application for the approval for a plan consists of: A description of the basis for the formulation of the plan; a list of the inspected taxpayers.

2.2.2. Approval for inspection plans of Sun-Departments of Taxation

The tax inspection divisions shall request the Directors of the provincial Departments of Taxation to consider approving and decide the number of the taxpayers to be put into the annual tax inspection plans of the Sub-Departments of Taxation not later than December 20 every year using the form 01/QTTTr issued together with this Procedure according to the applications for the approval for the annual inspection plans sent by the Sub-Departments of Taxation.

2.3. At Sub-Departments of Taxation

The tax inspection divisions shall submit the applications for the approval for the annual inspection plans to the Directors of the Sub-Departments of Taxation and send them to the Provincial Departments of Taxation before December 15 every year according to the requirements for tax administration and guiding documents on the formulation of the inspection plans. An application for the approval for a plan consists of: A description of the basis for the formulation of the plan; a list of the inspected taxpayers.

2.4. Handling overlapping inspections:

- In case of any taxpayer concurrently listed in the inspection plans of an inferior tax authority and a superior tax authority, the plan of the superior tax authority shall apply.

- In case the inspection plans of the Government Inspectorate, State Audit and Inspectorate of the Ministry of Finance are concurrent with the inspection plans of the tax authorities, the inspection plans of the Government Inspectorate, State Audit and Inspectorate of the Ministry of Finance shall apply.

2.5 Announcement of annual inspection plans

Each annual inspection plan must be announced to the tax payers and the supervisory tax authority of the taxpayers within 30 (thirty) working days from the issuance of the decision on the approval for the inspection plan.

In case of adjustment to the inspection plan or change in the inspection plan due to the concurrence with the plan of a superior authority, that must be notified to the taxpayers.

2.6. The tax authorities of shall give estimates of the manpower and arrange it to conduct irregular inspections in order to meet the requirements for the annual tax administration activities when formulating the annual inspection plans and complete the inspection plans with the best result.

2.7. The lists of the subsidiaries must be put into the inspection plans when formulating the inspection plans in case the taxpayers operate on a large scale such as Incorporations, Groups …

3. Adjustment to annual inspection plans

3.2. An approved annual inspection plan shall be adjusted:

a) if it is requested by the Minister of Finance or Head of a superior regulatory body:

The tax authority shall draw up a draft of the adjustment to the inspection plan and request the competent persons in charge of the approval for the inspection plans to consider approving the adjustment to the inspection plan according to the Head of a superior regulatory body.

b) if it is proposed by the Head of the tax authority:

The Head of the tax authority shall propose the adjustment to the approved annual inspection plan to ensure the fulfillment of the assigned tasks and request the competent persons in charge of the approval for the inspection plans to consider if necessary according to the tasks of the units and requirements for the administration.

3.2 Entitlement to approve adjustment to annual inspection plans

a) The Minister of Finance shall approve the adjustment to the inspection plans of the General Department of Taxation

b) The Director of the General Department of Taxation shall approve the adjustment to the inspection plans of the Provincial Departments of Taxation.

c) The Directors of the Provincial Department of Taxation shall approve the adjustment to the inspection plans of the Sub-Departments of Taxation.

3.3. The contents and procedures for the adjustment to the inspection plans are similar to the contents and procedures for the approval for the annual inspection plans, the reasons for the adjustment of which are specified.

3.4. The tax authorities shall periodically send annual reports on the adjustment to the annual inspection plans to the superior tax authorities in September 05. The superior tax authorities shall approve the adjusted inspection plans before October 05 every year.

4. Cases subject to surprise inspections

- Detection of violations of the laws on taxation committed by the agencies, organizations, or individuals.

- Handling complaints about the tax.

- Separation, merger, amalgamation, dissolution, bankrupt or equitization under the regulation of the laws.

- Tax inspection at the request of the heads of the Tax authorities or the Minister of Finance .

Surprise inspections shall be conducted at the request of the Heads of the Tax authorities.

II. Inspection at taxpayers’ premises

1. Preparation and decision on inspection

1.1. Collection of documents and determination of inspection contents

The head of an Inspection division shall assign the tax inspectors to collect the documents and determine the inspection contents using the form 02/QTTTr issued together with this Procedure according to the annual inspection plans.

1.2. Issuance of Decision on inspection

a) According to the determination of the inspection contents, the Head of the Inspection division shall establish a proposed Inspectorate including: Chief of the Inspectorate, members of the Inspectorate; vice chief (if necessary) to request the Head of the Inspection division to consider approving the Decision on inspection using the form 03/KTTT issued together with the Circular No. 156/2013/TT-BTC) An application for the issuance of the Decision on inspection consists of:

- A written request to the Head of the Tax authority;

- The draft of the Decision on inspection (including inspection tasks and scope);

- The analyzed contents using the form 02/QTTTr;

- Other relevant documents (if any).

d) In case of a surprise inspection, the draft of the Decision on inspection must be submitted together with:

- Evidence against the agencies, organizations, and individuals breaching the laws on taxation (in case of the inspection of agencies, organizations, and individuals breaching the laws on taxation).

- A complaint letter, documents collected from the administration and information about the income of the complainant (if any) (in case of the inspection due to the complaint letter)

- A written request of the taxpayer (in case of the inspection to handle the separation, merger, amalgamation, dissolution, bankrupt or equitization).

c) In case of a taxpayer having subsidiaries, the draft of the Decision on inspection must specify the list of the inspected subsidiaries.

d) The period of an inspection shall be determined according to the nature of the inspection but not more than 45 working days if such inspection is conducted by the General Department of Taxation, not more than 30 working days if such inspection is conducted by a provincial Department of Taxation or Sub-Department of Taxation.

dd) Circulation of the Decision on inspection:

Administrative Board of the tax authority shall send the Decision on inspection to the taxpayer via registered mail which shall be reported to the tax authority within 03 (three) working days from the issuance of the Decision on inspection.

e) Extension of inspection duration:

In case the inspection duration needs extending, the Chief of the Inspectorate must send a report to the Head of the Inspection division to request the Head of the Tax authority to consider deciding to extend the inspection within 05 (five) days before the inspection duration ands according to the Decision. The Decision on inspection shall only be extended once (using the form 18/KTTT issued together with the Circular 156/2013/TT-BTC), applying the principles as follows:

- The total inspection duration (including the extension) shall not exceed 70 working days (if such inspection is conducted by the General Department of Taxation).

- The total inspection duration (including the extension) shall not exceed 45 working days (if such inspection is conducted by a Provincial Department of Taxation or Sub-Department of Taxation).

f) In case of cancellation of inspection or Decision on inspection, deferring inspection

In case a Decision on inspection has been issued but the inspection is cancelled due to any reason, the Chief of the inspectorate must notify the Head of the Inspection division to request the Head of the tax authority to consider issuing the decision on the cancellation of the inspection using the form 16/KTTT issued together with the Circular No. 28/2011/TT-BTC.

- In case a Decision on inspection has been issued but the inspection is cancelled due to the force majeure (the taxpayer abandons the business premises, representative is absent for a long time due to the force majeure, or competent authorities are assessing), the Chief of the inspectorate must notify the Head of the Inspection division to request the Head of the tax authority to consider issuing the decision on the cancellation of the inspection using the form 19/KTTT issued together with the Circular No. 156/2013/TT-BTC.

- The Chief of the inspectorate shall notify the Head of the Inspection division to give the taxpayer a written notification of the approval for or disapproval of the deferment of the inspection within 05 (five) working days from the receipt of the written request for the deferment of the inspection sent by the taxpayer after (s)he receives the Decision on inspection.

- If the inspection is deferred by the tax authority, it shall send the taxpayer a written notification of the reasons for the deferment, deferment period and the time the inspection is re-conducted.

1.3. Notification of announcement of decision on inspection

After a Decision on inspection is issued, the Chief of the inspectorate shall notify (via telephone, mail or document if necessary) the representative of the taxpayer of the plan for the announcement of the Decision on inspection including: time and participants in the announcement of the Decision on inspection.

2. Conduct of inspection

2.1. Announcement of Decision on tax inspection

a) The Chief of the inspectorate shall announce the Decision on inspection to the taxpayer within 15 days from the signing of the Decision on inspection, unless the inspection is deferred or cancelled as prescribed in the abovementioned point f, 1.2, Section II, Part B.

b) When announcing the Decision on inspection, the Chief of the inspectorate shall:

- Introduce the members of the inspectorate;

- Specify the tasks and entitlement of the Inspectorate, inspection duration, rights and obligations of the taxpayer, proposed working plan of the Inspectorate.

- Request the taxpayer to provide information related to the inspection that the Inspectorate find necessary.

- Announce the specific time to work with each subsidiary in case the inspection scope includes the subsidiaries.

c) The announcement of the Decision on inspection must be recorded in writing using the form 05/KTTT issued together with the Circular No. 156/2013/TT-BTC which must be signed by the Chief of the Inspectorate and the legal representative of the taxpayer.

d) The inspection duration is the time from the Decision on inspection is announced to the day on which the inspection at the inspected place is finished.

2.2 Inspection at taxpayer’s premises

a) The Chief and members of the Inspectorate shall request the taxpayer to provide the accounting books and documents related to the inspection.

b) According to the accounting books and documents provided by the taxpayer and tax statements that the taxpayer sent to the Tax authority, the Inspectorate shall:

- Review and compare the documents provided by the taxpayer with the documents stored at the Tax authority.

- Compare the information recorded in the accounting documents, accounting books, accounting reports, financial statements, explanation report with the information in the tax statements to find out the difference.

- Compare the regulations of the Law on Taxation and the guiding documents in different inspection stage to identify the taxpayer’s adherence to tax laws.

- Conduct the inspection of the contents need inspecting.

c) The Inspectorate shall prepare the specific contents that the taxpayer must explain in writing with regard to the documents which is unclear or unable to reach a conclusion. The Inspectorate shall ask the taxpayer in person to clarify the contents and responsibilities of the individuals or collectives in case the written explanation of the taxpayer is unclear. Such conversation must be recorded in writing using the form 03/QTTTr which is signed by the Chief of the Inspectorate and the legal representative of the taxpayer and taped if necessary.

d) In case as assessment of the issues related to the inspection tasks is requested to serve as the basis for the inspection conclusion, the Chief of the Inspectorate must notify the Head of the Inspection division to request the Head of the tax authority to decide the assessment. The assessment is conducted under the regulations of the law on assessment. The Chief of the Inspectorate must notify the result of the assessment to the taxpayer.

dd) Part of or all of the documents related to the inspection tasks can be requested to be sealed by the Chief of the Inspectorate if the documents need remaining. The Decision on the seal of the documents is issued using the form 14/KTTT issued together with the Circular No. 156/2013/TT-BTC and enclosed with the report on the seal. Such report must be signed by the Inspectorate and the legal representative of the taxpayer using the form 15/KTTT issued together with the Circular No. 156/2013/TT-BTC.

The documents must not be sealed after the inspection duration ends. The use of the sealed documents must be permitted by the Chief of the Inspectorate.

If the seal is no longer necessary, the one giving the decision on the seal must make a decision on the cancellation of the seal and a list of the unsealed documents. Such written list must be signed by the legal representative of the taxpayer and the Chief of the Inspectorate. The form 04/QTTTr for the Decision on the cancellation of the seal and Record on the cancellation of the seal are issued together with this Procedure.

e) During the implementation of the decision on inspection, the Chief of the Inspectorate can decide to compile an inventory of the property within the scope of the Decision on tax inspection if the Inspectorate finds it necessary to compile an inventory of the property to compare the accounting books and accounting statements with the reality. It is required to issue the Decision on inventory using the form 16/KTTT issued together with the Circular No. 156/2013/TT-BTC and to file a Record specifying the participants, location of the inventory, names, quantity and conditions of the property using the form 17/KTTT issued together with the Circular No. 156/2013/TT-BTC.

The one making the Decision on inventory must give a Decision on the cancellation of the inventory using the form 05/QTTTr if the inventory of the property is unnecessary.

f) The Inspectorate shall implement the procedures for the impoundment of money, things or licenses under the regulations of the Law on Tax administration and current guiding documents in case of the impoundment of money, things or licenses.

g) The members of the Inspectorate shall provide a written Confirmation of the inspected figures for the taxpayer using the form 06/QTTTr issued together with this Procedure. The Confirmation of the inspected figures is one of the bases to file the Record on inspection.

c) In case of the subsidiaries involved in the Decision on inspection, the Inspectorate shall provide a Record on inspection for each subsidiary. The Summary of the inspection results shall be written by the Inspectorate base on the Record on inspection of each subsidiary.

k) If any force majeure event occurs during the inspection at the premises of the taxpayer so that the inspection must be suspended, the Chief of the Inspectorate shall send the Head of the inspection division a report on the reason for such suspension and the suspension period to request a notification of the suspension of the inspection. The inspection duration does not include the suspension period”.

2.3. Report on inspection progress

a) A periodic report shall be sent not later than the 10th, 20th and the last day of the month (the first Report from the day on which the inspection starts; the last Report prior to the day on which the inspection at the premises of the taxpayer finishes). The Chief of the Inspectorate shall send a progress report on the performance of the tasks of the Inspectorate to the Head of the Inspection division or at the irregular request of the Head of the Inspection division or the Head of the tax authority.

E.g.1: The Inspectorate conducting the inspection from April 03 to the end of April 17 shall make the progress reports as follows: The first Report (filed before April 10) for the time from April 03 to April 10; the last Report (filed on April 17) for the time from April 11 to April 17.

E.g2: The Inspectorate conducting the inspection from May 26 to the end of June 14 shall make the progress reports as follows: The first Report (filed before June 01) for the time from May 26 to May 31; the second Report (filed before June 11) for the time from June 01 to June 10; the last Report (filed on April 17) for the time from June 11 to June 14.

(The progress reports shall be sent not later than the 10th, 20th, and the last day of the month to facilitate summarization and report on the progress of the Inspectorate affiliated to the Inspection division).

b) A progress report on the inspection (using the form 21/KTTT issued together with the Circular No. 156/2013/TT-BTC) includes: completed tasks, tasks in progress, proposed tasks; difficulties and obstacles (if any) and solutions.

2.4. Filing Record on inspection

a) The Inspectorate must draw up a draft of the Record on inspection according to the results written in the Confirmation of the figures of the members of the Inspectorate and the Records of inspection at the subsidiaries (if any). The Draft of the Record on inspection must be agreed with among members of the Inspectorate and announced to the taxpayer. In case of any disagreement of any member of the Inspectorate, the Chief of the Inspectorate shall make the decision and take responsibility for his decision. The members of the Inspectorate can preserve the figures according to their Confirmation of the figures.

b) The Record on inspection must be signed by the Chief of the Inspectorate and the legal representative of the taxpayer within 10 days from the end of the inspection (using the form 04/KTTT issued together with the Circular No. 156/2013/TT-BTC)

c) The number of the Records of inspection that must be filed after each inspection depends on the nature and tasks of each inspection. However, there are at least 03 records: one for the taxpayer, one for the Inspectorate, one for the supervisory tax authority in charge of the taxpayer. A Record on inspection must specify the number of the pages and the attached appendices (if any); each page shall be signed by the Chief of the Inspectorate and the legal representative of the taxpayer, and bear the seal by the taxpayer (overlapping seals and a seal at the end of the record) if the taxpayer has their own seal.

d) If the taxpayer does not sign the Record on inspection after the end of the inspection, the Chief of the Inspectorate shall file a Record on the penalties for administrative violations and notify the Head of the Inspection division to request the Head of the tax authority to consider issuing the Decision on imposition of penalties for administrative violations as well as request the taxpayer to sign the Record on inspection within 05 (five) working days from the announcement of the Draft of the Record on inspection. The Head of the tax authority shall issue the Decision on tax and imposition of penalties for administrative violations of tax and the conclusion of the tax inspection according to the contents written on the Record on inspection within 30 (thirty) days from the announcement of the Record on inspection, if the taxpayer continues to refuse to sign the Record on inspection.

dd) During the production of the Draft of the Report of inspection, the Chief of the Inspectorate must report every difficulty in the policies and mechanism related to the inspection to the Head of the Inspection division for consideration. The Head of the Inspection division must report the difficulties outside their competence to the Head of the tax authority to deal with them within their competence.

e) If there is no assessment result or answer of the competent authorities to the questions concerning the policies and mechanism related to the inspection when the Record on inspection needs signing, the Chief of the Inspectorate must write the questions on the Record and sign the Record on inspection with the taxpayer under the regulation. After the receipt of the assessment result and the answers of the competent authority to the questions concerning the policies and mechanism related to the inspection, the Inspectorate shall make an Appendix of the Record on inspection with the taxpayer using the form 07/QTTTr issued together with this Procedure.

3. End of inspection

3.1. Report on inspection result and draft of inspection result

The Chief of the Inspectorate must report the inspection result to the Head of the Inspection division using the form 08/QTTTr issued together with this Procedure within 15 days from the end of the inspection. The Head of the Inspection division shall give their opinions before submitting to the Head of the tax authority as well as draw up a draft of the inspection result using the form 06/KTTT issued together with the Circular No. 156/2013/TT-BTC

3.2. Inspection conclusion, announcement of inspection conclusion and circulation of inspection conclusion

a) The Head of the tax authority shall sign the inspection conclusion (except for any inspection conclusion needs concluding by the competent authorities) within 15 days from the receipt of the report on the inspection result attached to the draft of the inspection conclusion.

b) During the time that the written inspection conclusion is drawing, the Head of the tax authority can request the Chief and members of the Inspectorate to make a report and the taxpayer to explain to clarify some issues that facilitate the signing and issuance of such inspection conclusion.

c) An application for the promulgation of the Inspection conclusion includes:

- The report on the inspection result of the Inspectorate;

- The Draft of the inspection conclusion;

- The Draft of the Decision on tax and imposition of penalties for administrative violations through the inspection of the adherence to the law on taxation using the form 20/KTTT issued together with the Circular No. 156/2013/TT-BTC.

- The Record on inspection;

- Other written explanations related to the inspection conclusion (if any).

d) The inspection conclusion is announced as follows:

- The Head of the Tax authority shall announce the inspection conclusion at the premises of the taxpayer as well as the legal representative of the taxpayer. The Chief of the Inspectorate can be authorized to announce the inspection conclusion if necessary.

- The announcement of the inspection conclusion shall be recorded in writing using the form 09/QTTT which must be signed by the Head of the Tax authority or the Chief of the Inspectorate (in case of authorization) and the legal representative of the taxpayer.

dd) The inspection conclusion and Decision on tax and imposition of penalties for administrative violations through the inspection of the adherence to the law on tax shall be sent to the taxpayer and supervisory tax authority (if the inspection is conducted by a superior tax authority).

e) In case the handling the violations of tax is outside the competence of the Head of the tax authority, the Head of the tax authority shall make a written request for the penalties for administrative violations of tax imposed by competent persons within 03 working days from the day on which the Inspection conclusion and Decision on the penalties for violations of tax.

4. Other matters related to inspection

4.1. Change in inspection tasks

During the inspection, if it is necessary to change any task written in the Decision on inspection, the Chief of the Inspectorate shall send a report on the reasons for the change in the inspection tasks attached to the Draft of the Decision on the change in the inspection tasks to the Head of the Inspection division. The Head of the Inspection division shall consider and request the Head of the tax authority to consider signing the Decision on the change in the inspection tasks using the form 10/QTTTr issued together with this Procedure.

4.2. Change of Chief or members of Inspectorate

If it is necessary to make a change of the Chief or any member of the Inspectorate during the inspection, the Head of the Inspection division shall consider and request the Head of the tax authority to consider signing the Decision on change of Chief, member of the Inspectorate using the form 11/QTTTr and Decision on supplementation of member of the Inspectorate using the form 12/QTTTr which are issued together with this Procedure.

4.3. Handing over documents and case to investigation agency (if any)

- If there is detection of any tax evasion during the inspection, the Inspectorate shall file a record on the suspension of the inspection, immediately send a report to the Head of the Inspection division and draft a written request that the Head of the tax authority hand over the documents to the investigation agency under the regulations of the laws.

- That the documents and case are handed over shall be recorded in writing using the form 13/QTTTr issued together with this Procedure and the receipt of the documents shall be recorded in writing using the form 14/QTTTr issued together with this Procedure.

4.4. Supervision of implementation of inspection conclusion and decision on handling after inspection

The Inspection division shall take charge and cooperate with the relevant boards in directing, supervising and expediting the implementation of the inspection conclusion, the payment for the tax arrears, refundable tax and fines according to the inspection result to the State budget under the regulations.

4.5 Storage of inspection dossiers

- A dossier on the inspection conducted by the Inspectorate includes: Decision on inspection, Record on inspection, report and explanation of the inspected taxpayer (if any); report on the inspection result; Inspection conclusion; Decision on tax and imposition of penalties for administrative violations (if any).

The Chief of the Inspectorate shall send the inspection dossier to the division or person in charge under the regulations of the laws and regulations of the authority within 30 days from the signing of the inspection conclusion.

The documents that are handed over shall be kept on file with the inspection dossier

III. Entering inspection data and regulations on report

1. Entering data

- The Head of an inspection division shall assign the Inspection division to enter the data on the inspection from the formulation of the inspection plan to the end of the inspection on the supporting systems of inspection.

- The data are entered on the supporting system of inspection, which must ensure the requirements for the progress time of the inspection, targets and the accuracy of the data on the system.

- The Department of the Inspection shall check and urge the Provincial departments of Taxation to enter the inspection data on the System and send a summary of the implementation of the Provincial Departments of Taxation to the General Department of Taxation. The General Department of Taxation shall direct and manage the tax inspection according to such summary.

- The Chief of the Inspectorate shall ensure that the data on the inspected enterprise entered on the System must be sufficient and accurate.

2. Regulations on report

In addition to the unscheduled reports in case of request of the competent authorities, the Inspection division at any tax authority shall monthly and yearly review the result of the inspection on the supporting system of inspection as well as send a report on the inspection to the Head of a tax authority at the same level to sign. The tax authority shall send it to a direct superior tax authority. The report must comply with the regulations as follows:

2.1. Time to finish report data

Because of continual inspections between the reporting periods, the report making must ensure punctuality and continuity between the reporting periods and avoid the repeated reports or in sufficient reports due to the inconsistent time the report data are completed.

The report data of each reporting period must be the final report data of the previous period to the end of such reporting period (each Monthly report is the result of the whole month with the cumulative data from the beginning of the year; each Yearly report is the result of the whole year).

2.2. Periodic reports

- Monthly reports that are filed in every month in a year.

- Yearly reports.

2.3. Time to send report

- With regard to any monthly report

+ The Sub-Department of Taxation shall file a report and send it to the Provincial Department of Taxation before the 05th in the following month.

+ The Provincial Department of Taxation shall file a report and send it to the General Department of Taxation before the 10th in the following month.

- With regard to any yearly report:

+ The Sub-Department of Taxation shall file a report and send it to the Provincial Department of Taxation before the 15th on the first month of the following year.

+ The Provincial Department of Taxation shall file a report and send it to the General Department of Taxation before the 20th in the first month of the following year.

2.4. Methods of report: The written records shall be sent both by post and via email (the Inspectorate of the General Department of Taxation; Inspection offices of Provincial Departments of Taxation) using the form 15/QTTTr issued together with this Procedure.

2.5. Compilation and use of reports on application: In addition to the written reports, the inspection divisions must compile, collect and use the information of the reports stored in the TTR application (Supervision of inspection results) to facilitate the inspections.

PART C

IMPLEMENTATION

1. The Inspectorate of the General Department of Taxation shall instruct the tax authorities to implement this Procedure.

2. Directors of the Provincial Departments of Taxation, Directors of the Sub-Departments of Taxation shall organize and implement this Procedure; conduct period or surprise inspections of the implementation of the Procedure of the inspection divisions and provide rewards or impose penalties under the regulations.

3. Any difficulty or obstacle that arises during the implementation should be reported to the General Department of Taxation for consideration./

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed