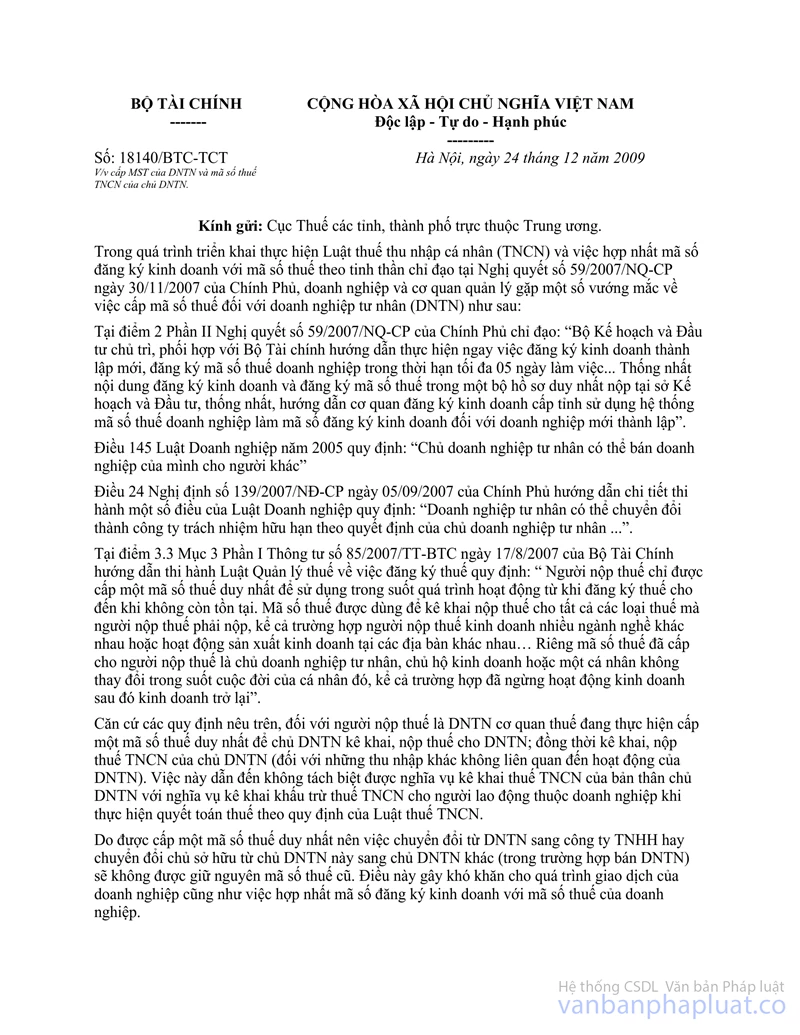

Nội dung toàn văn fficial Dispatch No. 18140 /BTC-TC re grant of tax identification numbers

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No: 18140 /BTC-TC |

Hanoi, December 24, 2009 |

To: Provincial-level Tax Departments

In the course of implementing the Law on Personal Income Tax (PIT) and the unification of business registration codes and tax identification numbers in line with the direction of the Government’s Resolution No. 59/2007/NQ-CP of November 30, 2007, enterprises and administrative agencies have encountered several problems in the grant of identification tax numbers to private enterprises as follows:

At Point 2, Part II of Resolution No. 59/2007/NQ-CP the Government instructed that: “the Ministry of Planning and Investment shall assume the prime responsibility for, and coordinate with the Ministry of Finance in, promptly guiding the business registration for the establishment of new enterprises and registration of identification tax numbers of enterprises within 5 working days… incorporate the registration of business and tax identification number in a single dossier to be submitted to provincial-level Planning and Investment Departments and unify and guide provincial-level business registration offices in using the system of tax identification numbers of enterprises as business registration numbers for the newly established enterprises.”

Article 145 of the 2005 Enterprise Law provides: “Owners of private enterprises may sell their enterprises to others.”

Article 24 of the Government’s Decree No. 139/2007/ND-CP of September 5, 2007, detailing the implementation of a number of articles of the Enterprise Law stipulates: “Private enterprises may transform themselves into limited liability companies under decisions of their owners…”

Point 3.3, Section 3, Part I of the Finance Ministry’s Circular No. 85/2007/TT-BTC of August 17, 2007, guiding the implementation of the Law on Tax Administration regarding tax registration stipulates: “Each taxpayer shall be granted a sole tax identification number for use throughout its operation process from tax registration to dissolution. A tax identification number shall be used for declaration and payment of all taxes payable by the taxpayer, including the case in which the taxpayer conducts different business lines or operates in different localities… Particularly, the tax identification granted to an owner of a private enterprise, an owner of a business household or an individual will be kept unchanged throughout his/her life, including the case in which he/she resumes his/her business after ceasing it for a time.”

Pursuant to the above provisions, for a taxpayer being a private enterprise, the tax agency shall grant a sole tax identification number to its owner to use in declaring and paying taxes for his/her enterprise, at the same time in declaring and paying his/her personal income tax (on other incomes not related to his/her enterprise’s operations). This will result in the inability to separate the obligation to declare personal income tax of the owner of the private enterprise himself/herself and the obligation to declare and withhold personal income tax of his/her enterprise’s employees when making tax finalization under the Law on Personal Income Tax.

Because of the grant of a sole tax identification number, the transformation from a private enterprise into a limited liability company or the change of the owner of a private enterprise (in case of sale of enterprises), the granted tax identification number will not be kept. This has caused difficulties to transactions of the enterprise as well as the unification of the business registration and tax identification numbers.

To help remove these difficulties, the Ministry of Finance guides the grant of tax identification numbers to private enterprises and personal income tax identification numbers to their owners in the direction of granting separate tax identification numbers to these two types of taxpayers as follows:

- Each private enterprise shall be granted a sole tax identification number for concurrent use as enterprise number in line with the Government’s Resolution No. 59/2007/NQ-CP for use throughout its business operation process, including the case of purchase and sale of private enterprises and their transformation into other forms of enterprise. Private enterprises shall use such tax identification number for declaring and paying their taxes and declaring and withholding personal income tax of their employees.

- Each private enterprise owner shall be granted a separate personal income tax identification number for declaring his/her own personal income tax.

In order to prevent bad effects on their transactions as well as their tax declaration and payment, private enterprises may keep their already granted tax identification numbers for use as their tax identification numbers under the above guidance. For private enterprise owners, tax agencies directly administrating their private enterprises shall base themselves on information on these owners in these enterprises’ previously declared tax registration data to grant personal income tax identification numbers to these owners for declaring their personal income tax obligations (private enterprise owners are not requested to declare information for personal income tax registration).

The Ministry of Finance provides its guidance to the Tax Departments for information and compliance.

|

|

FOR

THE MINISTER OF FINANCE |