Nội dung toàn văn Official Dispatch 2402/BTC-TCT 2016 providing guidelines for electronic invoicing

|

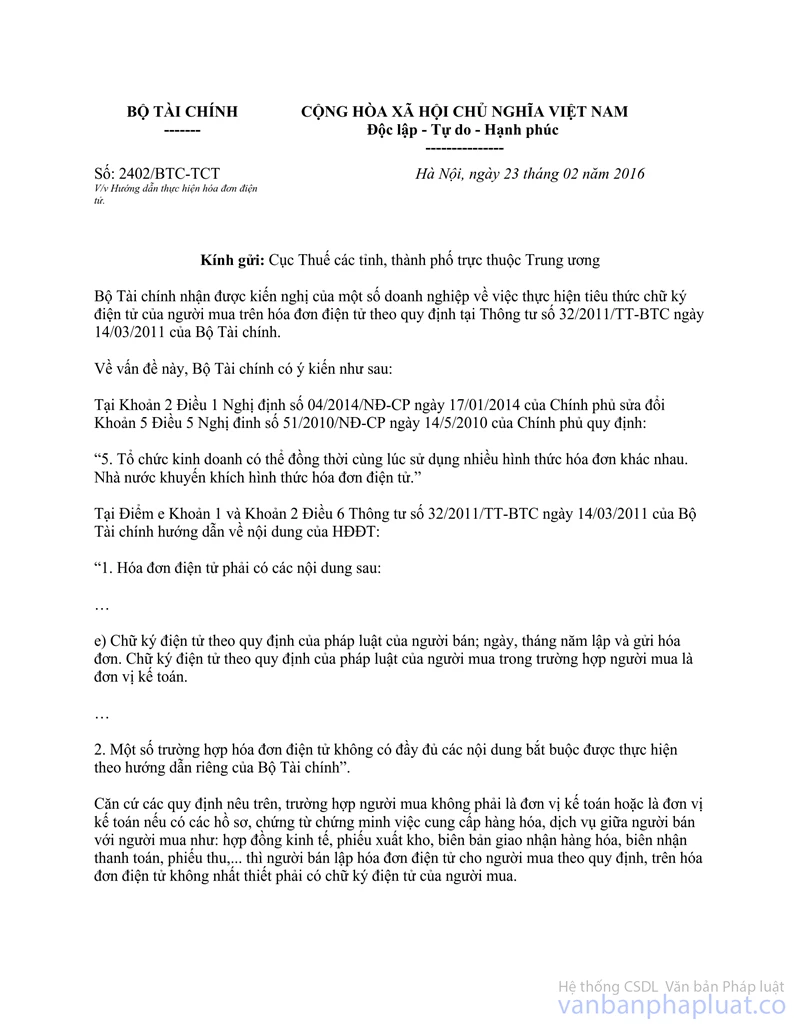

MINISTRY OF FINANCE |

THE SOCIALIST REPUBLIC OF VIETNAM |

|

No. 2402/BTC-TCT |

Hanoi, February 23, 2016 |

To: The Departments of Taxation of provinces and central-affiliated cities

The Ministry of Finance received the propositions of some enterprises about electronic signature of buyers on electronic invoices prescribed in the Circular No. 32/2011/TT-BTC dated March 14, 2011 of the Ministry of Finance.

Below are opinions of the Ministry of Finance:

Clause 2 Article 1 of the Government’s Decree No. 04/2014/ND-CP dated January 17, 2014 that amends Clause 5 Article 5 of the Government’s Decree No. 51/2010/ND-CP dated May 14, 2010:

“5. Traders may concurrently use different types of invoices. The State encourages the use of electronic invoices.”

Point e Clause 1 and Clause 2 Article 6 of the Circular No. 32/2011/TT-BTC dated March 14, 2011 of the Ministry of Finance providing guidelines for contents of electronic invoices:

“1. An electronic invoice shall include the following contents:

…

e) Lawful electronic signature of the seller; date of issuing the invoice. Lawful electronic signature of the buyer in case the buyer is an accounting unit.

…

2. Regarding the electronic invoices which do not contain all compulsory contents, the guidelines from the Ministry of Finance must be adhered to”.

Pursuant to the aforementioned regulations, whether the buyer is an accounting unit or not, if documentary evidences for provision of goods and services between the buyer and seller such as business contract, delivery note, delivery receipts, payment receipts, etc. are available, the seller shall issue an electronic invoice to the buyer as prescribed by law. It is not required to include the buyer’s electronic signature in the invoice.

The Department of Taxation has the responsibility to consider each specific case and fulfillment of eligibility requirements by enterprises to provide guidelines for exemption from the buyer’s electronic signature on the electronic invoice.

For your information and compliance./.

|

|

PP. THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed