Nội dung toàn văn Official Dispatch 82088/CT-TTHT 2017 tariffs applied to foreign airlines Ha Noi

|

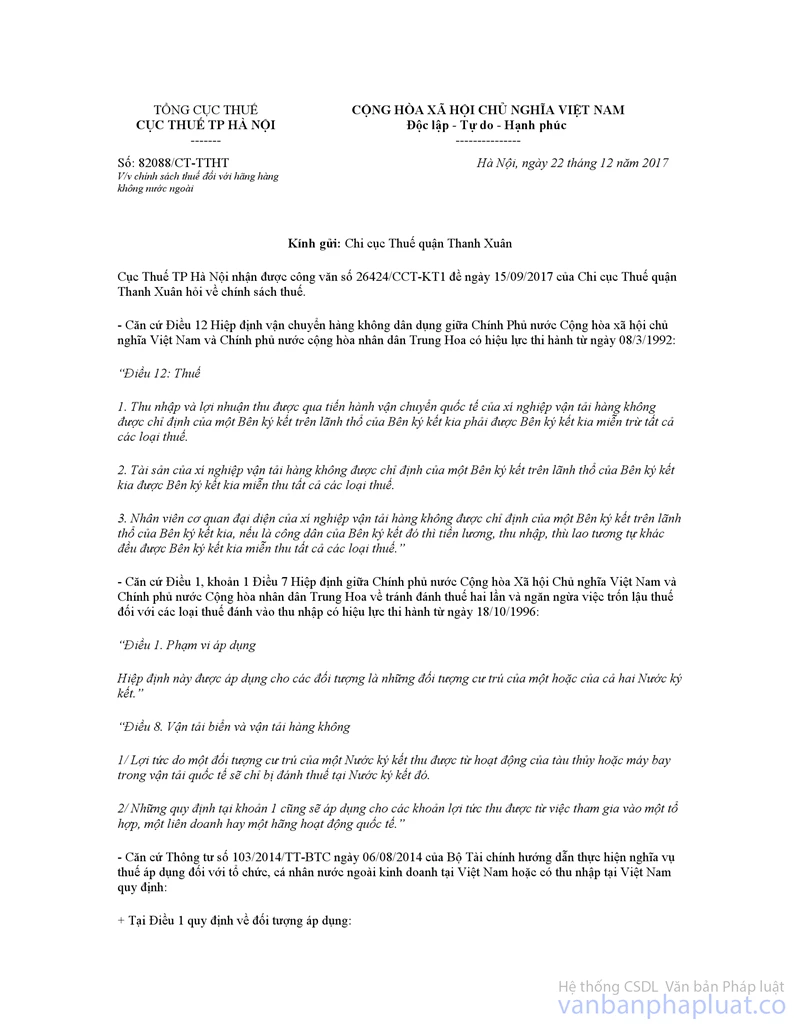

GENERAL DEPARTMENT OF TAXATION |

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 82088/CT-TTHT |

Hanoi, December 22, 2017 |

To: Sub-department of taxation of Thanh Xuan district

Department of Taxation of Hanoi received Official Dispatch No. 26424/CCT-KT1 dated September 15, 2017 from Sub-department of taxation of Thanh Xuan district.

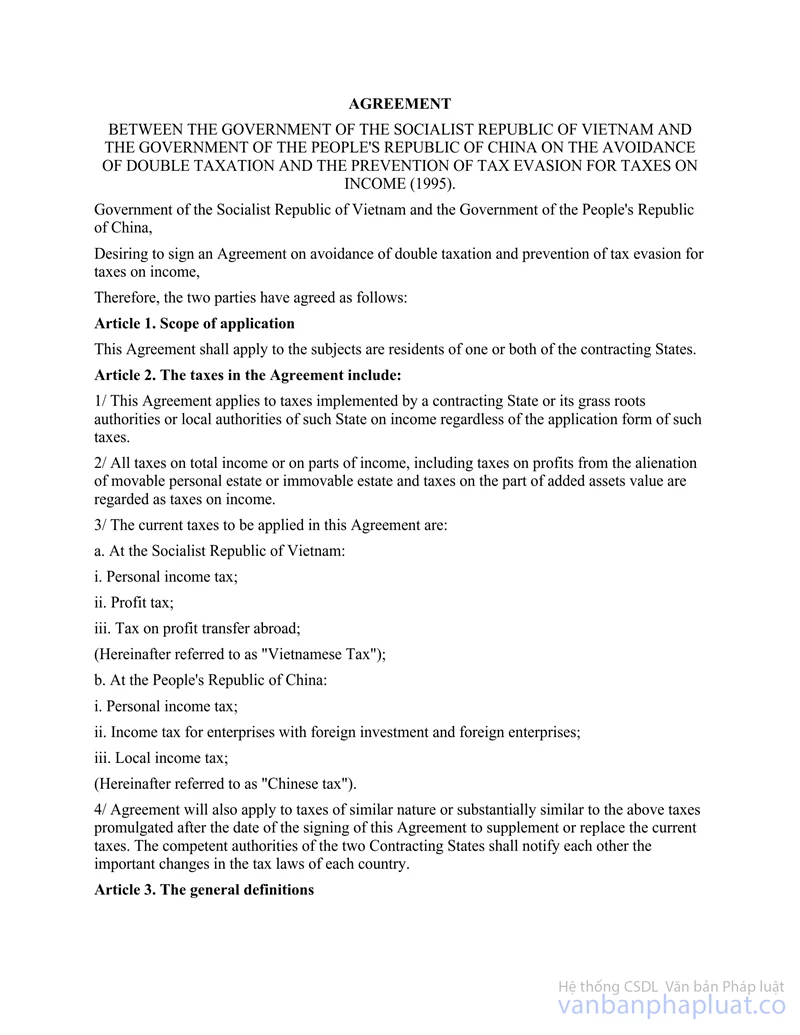

- Pursuant to Article 12 of the Civil Air Transport Agreement between the Government of Socialist Republic of Vietnam and the Government of the People’s Republic of China, which comes into force from March 08, 1992:

“Article 12: Tax

1. Incomes and profits from international transport by the designated airline(s) of a Party within the territory of the other Party shall be exempted from all tariffs by the latter.

2. Assets of the designated airline(s) of a Party in the territory of the other Party shall be exempted from all tariffs by the latter.

3. Salaries, incomes and similar wages of employees of the representative agency of the designated airline(s) of a Party in the territory of the other Party shall be exempted from all taxes by the latter if they are citizens of the former.”

- Pursuant to Article 1, Clause 1 Article 7 of the Double Taxation Agreement between the Government of Socialist Republic of Vietnam and the Government of the People’s Republic of China, which came into force since October 18, 1996:

“Article 1. Scope

This Agreement shall apply to persons who are residents of one or both of the Contracting States.”

“Article 8. Shipping and air transport

1/ Profits derived by a resident of a Contracting State from the operation of ships or aircraft in international traffic shall be taxable only in that Contracting State.

2/ The provisions of paragraph 1 shall also apply to profits from the participation in a pool, a joint business or an international operating agency.”

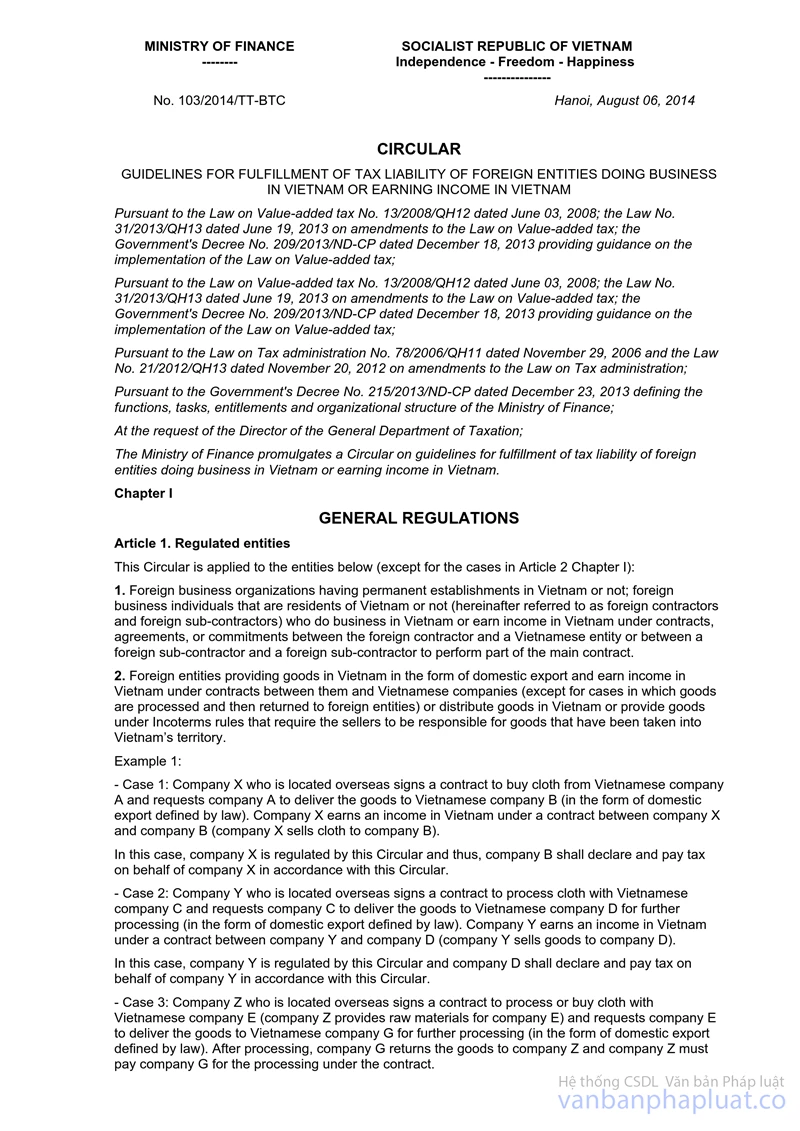

- Pursuant to Circular No. 103/2014/TT-BTC dated August 06, 2014 of the Ministry of Finance on tax liability of foreign organizations and foreigners doing business in Vietnam or earning incomes in Vietnam:

+ Article 1: Scope

“1. Foreign business organizations having permanent establishments in Vietnam or not; foreign business individuals that are residents of Vietnam or not (hereinafter referred to as foreign contractors and foreign sub-contractors) who do business in Vietnam or earn income in Vietnam under contracts, agreements, or commitments between the foreign contractor and a Vietnamese entity or between a foreign sub-contractor and a foreign sub-contractor to perform part of the main contract.”

- Pursuant to Circular No. 156/2013/TT-BTC dated November 6, 2013 of the Ministry of Finance on elaboration of the Law on Tax administration, the Law on amendments to the Law on Tax administration and the Government's Decree No. 83/2013/NĐ-CP dated July 22, 2013:

+ Point c Clause 3 Article 20:

“c) Tax declaration by foreign airlines:

Ticket offices and agents in Vietnam of foreign airlines shall declare and pay corporate income tax on their behalf.

Ticket offices and agents in Vietnam of foreign airlines shall declare and pay corporate income tax on their behalf.

Corporate income tax payable by foreign airlines shall be declared monthly.

c.1) Tax declaration documents:

- Tax declaration form No. 01/HKNN enclosed with the Circular.

- Photocopies of the main contract and sub-contract certified by the taxpayer (for the first tax declaration of the main contract);

- Photocopies of the business license or practice certificate certified by the taxpayer

c.2) Notice of eligibility for tax exemption or tax reduction according to an international agreement:

f the foreign airline is eligible for tax exemption or reduction according to a Double taxation agreement between Vietnam and another country/territory, the following procedure shall be followed:

15 days before the commencement or the first tax period of the year (whichever comes first), the office in Vietnam of the foreign airline shall submit an application dossier to the tax authority, which consists of: + The Notice of eligibility for tax exemption or reduction (form 01/HTQT enclosed with the Circular);

+ The original or certified true copy of the Certificate of residence (consularly legalized) issued by the tax authority of the home country before the year in which the Notice of tax exemption or reduction is issued;

+ A photocopy, which has to be certified by the taxpayer, of the license to operate in Vietnam of issued by Civil Aviation Administration of Vietnam in accordance with the Law on Civil aviation.

- - A Letter of attorney if the taxpayer authorizes a legal representative to carry out the procedure for applying the Agreement.

If a notice of eligibility tax exemption or reduction has been sent in the previous year, only the photocopies of the license to operate in Vietnam issued by Civil Aviation Administration of Vietnam, which are certified by the taxpayer, shall be submitted.

15 days before the expiration of the contract in Vietnam, or the end of the tax year (whichever comes first), the office in Vietnam of the foreign airline shall send the Certificate of residence that has been consularly legalized in that tax year, a declaration of income from international transport (form 01-1/HKNN if tickets are sold in Vietnam, form 01-2/HKNN if seats are swapped or shared) in the tax year to the tax authority as the basis for exemption or reduction of CIT on international transport services of the foreign airline.

If the taxpayer fails to provide sufficient information or documents, explanation must be provided in form 01/HTQT mentioned above.”

+ Clause 3 Article 47 on tax incentives according to international agreements:

“1. The organizations and individuals eligible for tax incentives according to the international agreements that are not Double taxation agreements (hereinafter referred to as international agreements) shall follow the instructions in Clause 2 or Clause 3 of this Article.”

“3. In case a foreign entity does not declare and pay tax directly to the tax authority:

a) Procedure to be followed by the foreign entity:

On the date of conclusion of the contract with the Vietnamese party, the foreign entity shall send the Vietnamese party a dossier, which consists of:

- A photocopy of the international agreement.

- A notice of tax exemption or reduction (form 01/MTPDTA enclosed herewith) certified by the agency that proposed the international agreement, except for the international agreements proposed by the Ministry of Finance).

- A photocopy of the contract with the Vietnamese party, certified by the foreign entity or an authorized representative.

- A translation of the summary of the contract certified by the foreign entity or an authorized representative (if the contract is in a foreign language).

The translation must contain: names of the contract and articles, contractual tasks and tax liability.

- The letter of attorney if the foreign entity authorizes a Vietnamese entity to follow the procedure. The letter of attorney must be signed by representatives of both parties.

- If the foreign entity is not able to provide the contract with the Vietnamese party, it may submit equivalent documents and provide explanation in the notice of tax exemption or reduction.”

Pursuant to the aforementioned regulations and guidelines:

- When Vici Logistics Co., Ltd (hereinafter referred to as “Vici”) signs a contract to act as an agent in Vietnam with a foreign airline, Vici shall declare and pay corporate income tax on behalf of the foreign airline.

- However, since Vietnam and China has entered into the 1992’s Civil Air Transport Agreement and the 1996’s Double Taxation Agreement, both of which provide for exemption of taxes on incomes of airlines.

It is recommended that Sub-department of taxation of Thanh Xuan district reconsiders the eligibility of China Southern Airline to apply the Civil Air Transport Agreement or the Double Taxation Agreement, and instruct the parties to follow the procedures specified in Clause 3 Article 47, Point c2 Clause 3 Article 20 of Circular No. 156/2013/TT-BTC accordingly.

For your reference and compliance./.

|

|

ON BEHALF OF DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed