Nội dung toàn văn Official Dispatch 848/BTC-TCT Tax policies tax administration related activities service online reservation

|

MINISTRY OF

FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

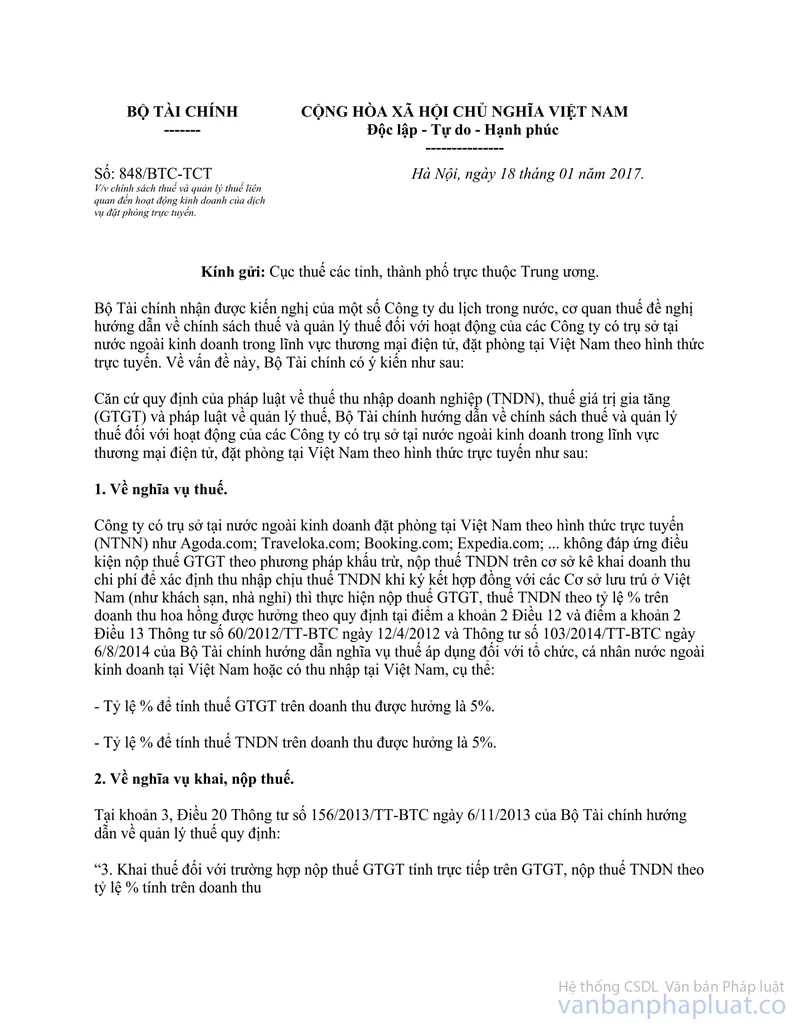

No. 848/BTC-TCT |

Hanoi, January 18, 2017. |

To. Departments of Taxation of provinces and central-affiliated cities

Several domestic tourism companies have requested the Ministry of Finance to provide guidance on tax policies and tax administration related to activities of overseas tourism companies that provide e-commerce or online reservation services in Vietnam.

Pursuant to regulations of law on corporate income tax (CIT), value added tax (VAT) and law on tax administration, the Ministry of Finance hereby provides guidance on tax policies and tax administration related to activities of overseas companies. To be specific:

1. Tax liability:

Overseas companies providing online reservation services in Vietnam (hereinafter referred to as “foreign contractors”) such as Agoda.com; Traveloka.com; Booking.com; Expedia.com, etc. that fail to satisfy conditions for paying VAT according to credit-invoice method or paying CIT on taxable income (= revenue – expense) when signing contracts with accommodation establishments in Vietnam (hotels, hostels, etc.) shall pay VAT and CIT on the received commissions as prescribed in Point a Clause 2 Article 12 and Point a Clause 2 Article 13 of Circular No. 60/2012/TT-BTC dated April 12, 2012 and Circular No. 103/2014/TT-BTC dated August 6, 2014. To be specific:

- The VAT rate (%) shall be 5 %.

- The CIT rate (%) shall be 5 %.

2. Responsibility to declare and pay taxes

Pursuant to Clause 3 Article 20 of Circular No. 156/2013/TT-BTC of the Ministry of Finance dated November 6, 2013 on tax administration:

“3. Declaring VAT on added value and CIT on revenue

a) VAT on added value or CIT on revenue shall be declared whenever a payment is made to the foreign contractor. A terminal tax return shall be made when the contract finishes.

If a Vietnamese party makes more than one payment to a foreign contractor in a month, the taxpayer may request the permission to declare tax monthly instead of whenever a payment is made.

- The Vietnamese party that signs a contract with the foreign contractor shall withhold and pay the taxes on behalf of the foreign contractor and submit tax returns to the supervisory tax authority of the Vietnamese party.”

Accommodation establishments shall declare and pay taxes on behalf of foreign contractors in accordance with the abovementioned regulations. The Departments of taxation of provinces shall assist accommodation establishments in determining tax liability, declaring and paying taxes in accordance with regulations of law. To be specific:

- In the cases where a customer directly pays room rental to an accommodation establishment in Vietnam and this establishment subsequently pays a commission to the foreign contractor, the accommodation establishment shall declare and pay tax on behalf of the foreign contractor.

- In the cases where a customer directly pays room rental to a foreign contractor and the foreign contractor subsequently transfers the room rental to the accommodation establishment and withholds a commission,

+ The Department of Taxation of the province shall request the accommodation establishment to notify the foreign contractor of tax liability, declare and pay taxes on behalf of the foreign contractor if there is a contract between the accommodation establishment and the foreign contractor.

+ The Department of Taxation of the province shall request the accommodation establishment to specify the tax liability of the foreign contractor when the contract between them is signed, declare and pay taxes on behalf of the foreign contractor if there is no contract between the accommodation establishment and the foreign contractor.

Department of Taxation of provinces shall supervise the declaration and payment of taxes on commission paid to foreign contractors in accordance with regulations of law. Any problem arising during the implementation of this document should be reported to the Ministry of Finance for instruction.

|

|

P.P MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by THƯ VIỆN PHÁP LUẬT and

for reference purposes only. Its copyright is owned by THƯ VIỆN PHÁP LUẬT

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed