Nội dung toàn văn Official Dispatch No.11071/BTC-TCT of August 05,2009, on personal income tax on real estate

|

THE

MINISTRY OF FINANCE’S |

SOCIALIST

REPUBLIC OF VIET NAM |

|

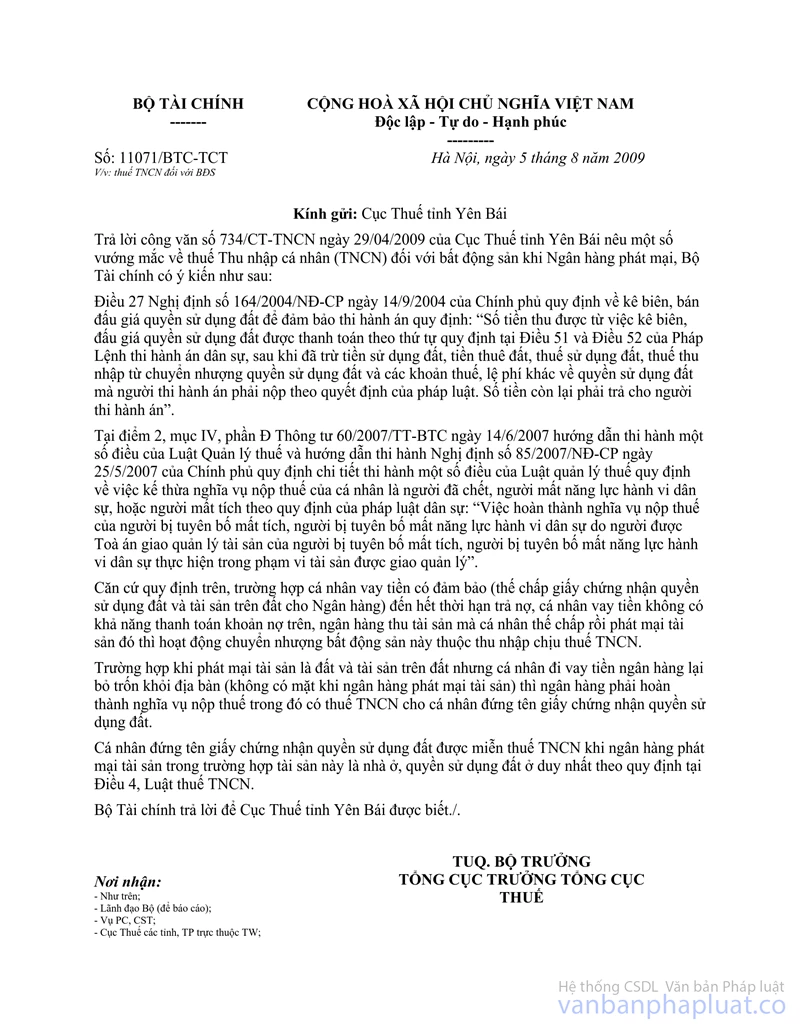

No. 11071/BTC-TCT |

Hanoi, August 05, 2009 |

To: The Tax Department of Yen Bai province

In response to Official Letter No. 734/CT-TNCN of April 29, 2009, of the Tax Department of Yen Bai province, inquiring about personal income tax (PIT) on real estate publicly sold by banks, the Ministry of Finance provides the following guidance:

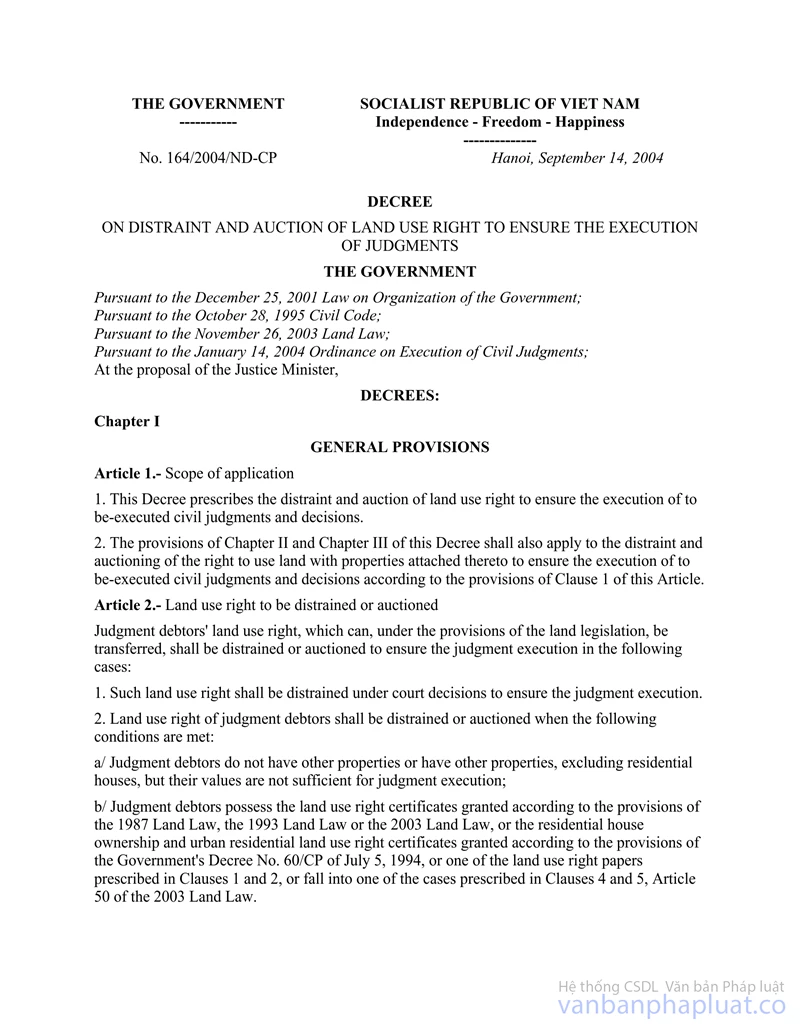

Article 27 of the Government’s Decree No. 164/2004/ND-CP of September 14, 2004, on attachment and auction of land use rights for securing judgment enforcement, stipulates: “Proceeds from land use right attachment and auction shall be paid according to the priority order prescribed in Articles 51 and 52 of the Ordinance on Civil Judgment Enforcement, after subtracting the land use levy, land rent, land use tax, tax on incomes from land use right transfer and other taxes and fees related to land use rights which must be paid by judgment debtors under law. The remainder shall be refunded to judgment debtors.”

Point 2, Section IV, Part E of the Ministry of Finance’s Circular No. 60/2007/TT-BTC of June 14, 2007, guiding the implementation of a number of articles of the Law on Tax Administration and the implementation of the Government’s Decree No. 85/2007/ND-CP of May 25, 2007, detailing the implementation of a number of articles of the Law on Tax Administration, stipulates the takeover of the tax obligation of individuals who are deceased, have lost their civil act capacity or are missing under the civil law as follows: “The tax obligation of a person who is declared missing or having lost his/her civil act capacity shall be fulfilled by another person assigned by the court to manage the former’s assets with the value of these assets.”

Pursuant to the above provisions, in case an individual who has borrowed a loan with security (mortgage of his/her certificate of rights to use land and assets on land at the lending bank) is unable to repay the loan upon its maturity and subsequently the bank attaches and auctions his/her mortgaged asset, income from this real estate transfer is liable to PIT.

Upon public sale of land and assets attached to land, if individual borrowers abscond from the locality (they are absent when banks publicly sell the assets), banks shall fulfill the tax obligation, including personal income tax, for individuals named in land use right certificates.

Individuals named in land use right certificate are exempt from personal income tax when their assets publicly sold by banks are their sole residential houses or land use rights under Article 4 of the Law on Personal Income Tax.

Above is the Ministry of Finance’s reply to the Tax Department of Yen Bai province.

|

|

UNDER

THE MINISTER OF FINANCE’S AUTHORIZATION |