Nội dung toàn văn Official Dispatch No. 1121TCT/TS on registration fees

|

THE

FINANCE MINISTRY |

SOCIALIST

REPUBLIC OF VIET NAM |

|

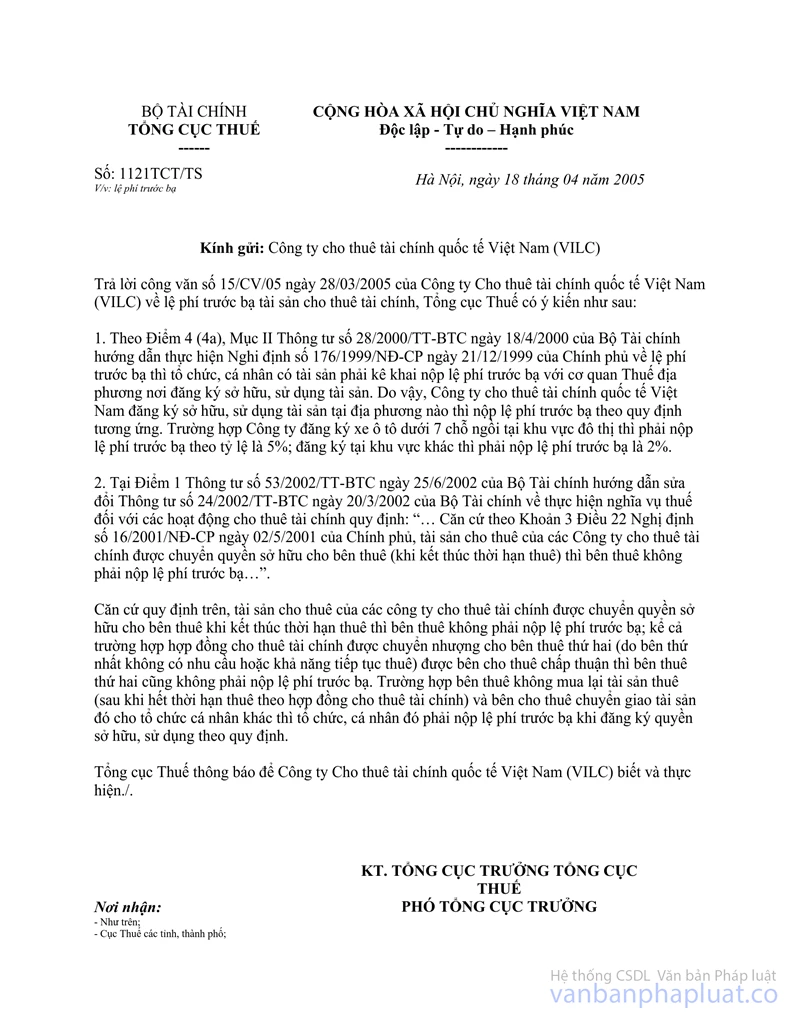

No. 1121 TCT/TS |

Hanoi, April 18, 2005 |

OFFICIAL LETTER

ON REGISTRATION FEES

To: Vietnam International Leasing Company (VILC)

In response to the VILC's Official Letter No. 15/CV/05 of March 28, 2005, on registration fees for financial lease assets, the General Department of Taxation gives the following opinion:

1. According to Point 4 (4a), Section II of the Finance Ministry's Circular No. 28/2000/TT-BTC of April 18, 2000, guiding the implementation of the Government's Decree No. 176/1999/ND-CP of December 21, 1999, on registration fees, asset- owners either organizations and individuals must declare and pay registration fees to local tax offices in the area where they register ownership or use of such assets. Therefore, the VILC shall pay registration fees according to regulations applied in the area where it registers its assets. If the VILC registers cars of under 7 seats in urban centers, it must pay registration fees at the rate of 5%; the registration fee rate is 2% in all other cases.

2. Point 1 of the Finance Ministry's Circular No. 53/2002/TT-BTC of June 25, 2002, guiding amendments to the Finance Ministry's Circular No. 24/2002/TT-BTC of March 20, 2002, on the performance of tax obligations for financial leasing activities, states that "… Pursuant to Clause 3, Article 22 of the Government's Decree No. 16/2001/ND-CP of May 2, 2001, where ownership of lease assets of financial leasing companies is transferred to lessees (at the expiration of lease term), the lessees do not have to pay registration fees thereon…"

According to the above-said provisions, for financial leasing companies' lease assets which have their ownership transferred to lessees at the expiration of a lease term, the lessees shall not have to pay registration fees thereon; even in cases where the financial lease contract has been transferred to the sub- lessee (because the first lessee have no need to or cannot continue with the lease), under the lessor's agreement, the sub - lessee shall also not have to pay the registration fee. Where the lessee do not buy the leased assets (after the expiration of the lease term under the financial lease contract) and the lessor transfers such assets to another organization or individual, such organization or individual must pay registration fee when it/he/she registers ownership or use of the assets according to regulations.

The General Department of Taxation hereby notifies the VILC as instruction for compliance

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |