Nội dung toàn văn Official Dispatch No. 11660/BTC-TCT, on business income tax policies for domains

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

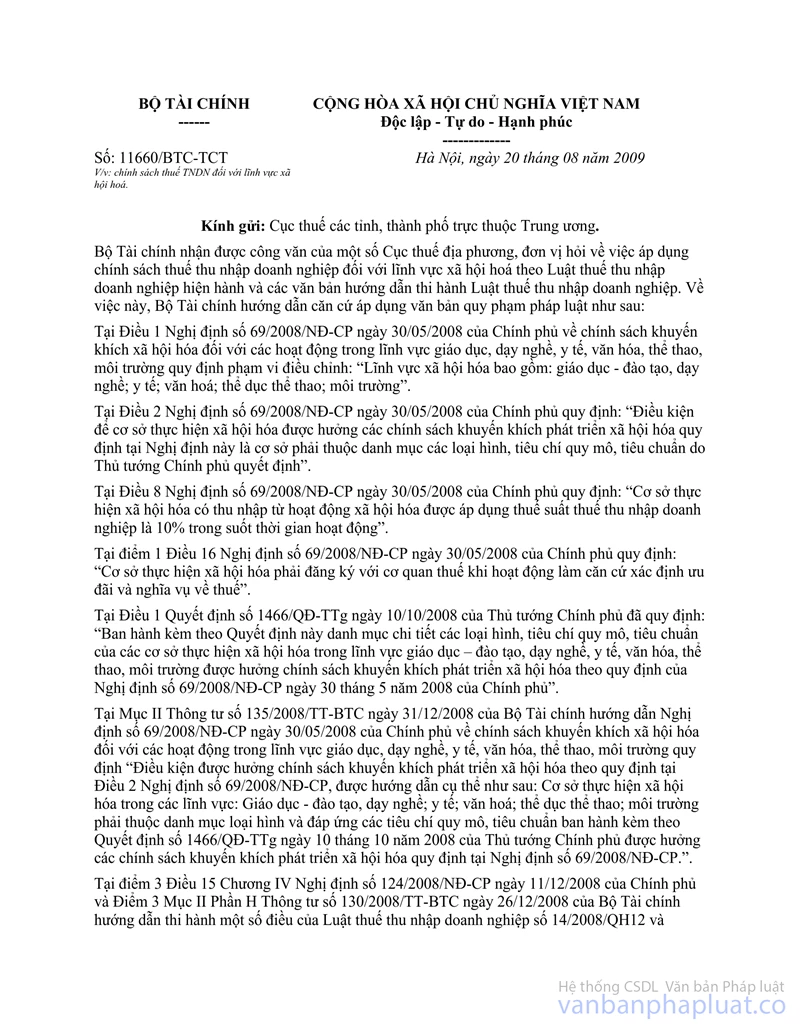

No. 11660/BTC-TCT |

Hanoi, August 20, 2009 |

To: Provincial – level Tax Departments

The Ministry of Finance has received official letters of some provincial-level Tax Departments and units inquiring about business income tax policies for domains encouraged for socialization under the current Business Income Tax Law and its guiding documents. Regarding this, the Ministry of Finance guides the application of these policies on the basis of the following legal documents:

Article 1 of the Government's Decree No. 69/2008/ND-CP of May 30, 2008, on incentive policies for the socialization of educational, vocational, healthcare, cultural, sports and environmental activities prescribes the scope of regulation as follows: “Domains encouraged for socialization include education-training, vocational training; healthcare; culture; physical training-sports; and environment.”

Article 2 of the Government's Decree No. 69/2008/ND-CP of May 30, 2008, stipulates: “Conditions for establishments to enjoy incentive policies prescribed in this Decree are they must be those on the list of entities whose types, sizes and criteria are decided by the Prime Minister.”

Article 8 of the Government's Decree No. 69/2008/ND-CP of May 30, 2008, stipulates: “Establishments engaged in activities encouraged for socialization which earn incomes from these activities are entitled to the 10% business income tax rate for the whole operation period.”

Point 1, Article 16 of the Government's Decree No. 69/2008/ND-CP of May 30, 2008, stipulates: “Establishments engaged in activities encouraged for socialization shall register their operation with tax agencies to provide the basis for determining tax incentives and obligations.”

Article 1 of the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, stipulates: “To promulgate together with this Decision a detailed list of types, sizes and criteria of establishments engaged in education-training, vocational, healthcare, cultural, sports and environmental activities encouraged for socialization which are entitled to incentive policies under the Government's Decree No. 69/2008/ND-CP of May 30, 2008.”

Section II of the Ministry of Finance's Circular No. 135/2008/TT-BTC of December 31, 2008, guiding the Government's Decree No. 69/2008/ND-CP of May 30, 2008, on incentive policies for the socialization of educational, vocational, healthcare, cultural, sports and environmental activities, stipulates: “Conditions for enjoying incentive policies under Article 2 of Decree No. 69/2008/ND-CP are specifically guided as follows: Establishments engaged in education-training, vocational training; healthcare; culture; physical training and sports or environmental activities encouraged for socialization which satisfy the conditions on types, sizes and criteria under the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, may enjoy incentive policies under Decree No. 69/2008/ND-CP.”

Point 3, Article 15, Chapter IV of the Government's Decree No. 124/2008/ND-CP of December 11, 2008, and Point 3, Section II, Part H of the Ministry of Finance's Circular No. 130/2008/TT-BTC of December 26, 2008, guiding a number of articles of Business income tax Law No. 14/2008/QH12 and guiding the Government's Decree No. 124/2008/ND-CP of December 11, 2008, detailing a number of articles of the Business Income Tax Law, stipulate: “The 10% tax rate for the whole operation period for incomes earned by enterprises from education-training, vocational training, healthcare, culture, sports or environmental activities (below referred to as activities encouraged for socialization). Detailed activities encouraged for socialization are specified in the list promulgated by the Prime Minister.”

Point 3, Article 20, Chapter V of the Government's Decree No. 124/2008/ND-CP of December 11, 2008, and Point 5, Part I of the Ministry of Finance's Circular No. 130/2008/TT-BTC of December 26, 2008, stipulate: “Enterprises engaged in activities encouraged for socialization before January 1, 2009, which are currently subject to a tax rate higher than 10%, will be entitled to the 10% tax rate for these activities from January 1, 2009.”

Under the above provisions, “domains encouraged for socialization,” “establishments engaged in activities encouraged for socialization,” and “conditions for enjoying incentive policies for socialization” are specified in the Government's Decree No. 69/2008/ND-CP of May 20, 2008, the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, and the Ministry of Finance's Circular No. 135/2008/TT-BTC of December 31, 2008, guiding the Government's Decree No. 69/2008/ND-CP of May 30, 2008, on incentive policies for the socialization of educational, vocational, healthcare, cultural, sports and environmental activities.

The Ministry of Finance guides the application of business income tax policies for domains encouraged for socialization as follows:

- For establishments engaged in activities encouraged for socialization within the scope of regulation of the Government's Decree No. 69/2008/ND-CP of May 30, 2008 (not of the Government's Decree No. 124/2008/ND-CP of December 11, 2008) and earning incomes from activities encouraged for socialization which meet the conditions on types, sizes and criteria promulgated together the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, and have registered their operation with tax agencies, the time for applying the 10% business income tax rate for the whole operation period is counted from the effective date of the Government's Decree No. 69/2008/ND-CP of May 30, 2008.

- For establishments engaged in activities encouraged for socialization within the scope of regulation of both the Government's Decree No. 124/2008/ND-CP of December 11, 2008, and the Government's Decree No. 69/2008/ND-CP of May 30, 2008, and earning incomes from activities encouraged for socialization, which meet the conditions on types, sizes and criteria promulgated together with the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, and have registered their operation with tax agencies, the time for applying the 10% business income tax rate for the whole operation period is counted from the effective date of the Government's Decree No. 69/2008/ND-CP of May 30, 2008.

- For establishments engaged in activities encouraged for socialization within the scope of regulation of the Government's Decree No. 124/2008/ND-CP of December 11, 2008, not of the Government's Decree No. 69/2008/ND-CP of May 30, 2008:

+ For enterprises which operate in other domains but earn incomes from activities encouraged for socialization or business establishments which earn incomes from activities encouraged for socialization but do not establish financially independent units operating in the domains encouraged for socialization, if they fully meet the conditions on types, sizes and criteria promulgated together with the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, they are entitled to the 10% business income tax rate for the whole operation period for their incomes earned from education-training, vocational, healthcare, cultural, sports and environmental activities from January 1, 2009.

+ For enterprises engaged in activities encouraged for socialization before January 1, 2009, which are currently subject to a tax rate higher than 10%, if they meet the conditions on types, sizes and criteria promulgated together with the Prime Minister's Decision No. 1466/QD-TTg of October 10, 2008, they are entitled to the 10% tax rate for their incomes earned from activities encouraged for socialization from January 1, 2009.

The Ministry of Finance provides the above guidance to provincial-level Tax Departments for information.

|

|

UNDER

THE AUTHORIZATION |