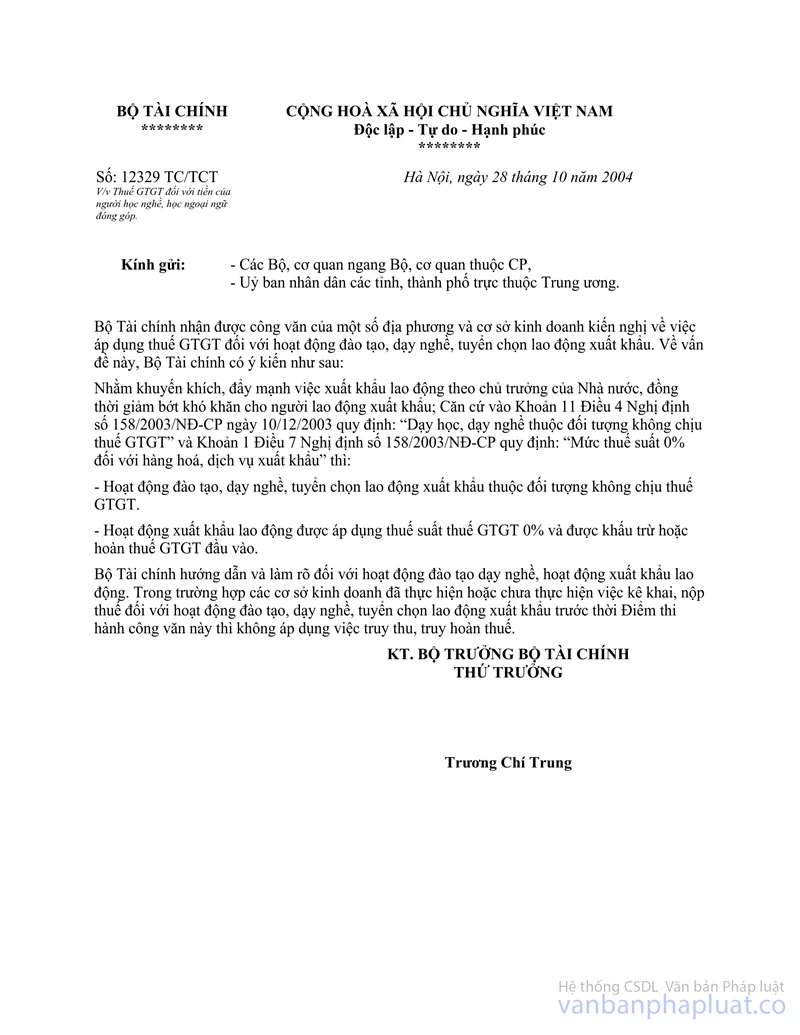

Nội dung toàn văn Official Dispatch No. 12329 TC/TCT of October 28, 2004, on Value added tax (VAT) on money contributed by job trainees or foreign language learners

|

THE MINISTRY OF FINANCE |

THE SOCIALIST REPUBLIC OF VIETNAM |

|

No. 12329 TC/TCT |

Hanoi, October 28, 2004 |

|

To: |

- Ministries, ministerial-level agencies,

Government-attached agencies |

The Finance Ministry has received official letters from some localities and business establishments regarding the application of VAT to job training and teaching activities as well as to the selection of laborers for export. Concerning this matter, the Ministry hereby express its opinions as follows:

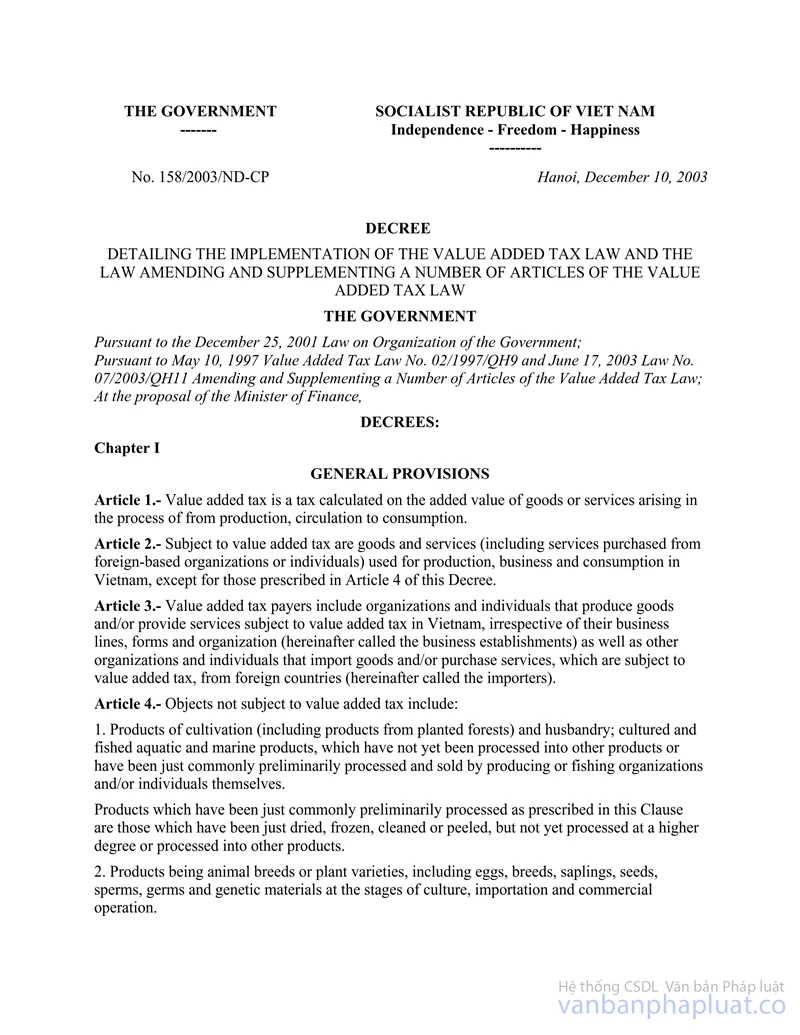

With a view to encouraging and boosting labor export according to the State’s policy while lessening difficulties for export laborers; Pursuant to Clause 11, Article 4 of Decree No. 158/2003/ND-CP of December 10, 2003, which stipulates: “Teaching and vocational training are not subject to VAT,” and Clause 1, Article 7 of Decree No. 158/2003/ND-CP which stipulates: “The 0% tax rate shall apply to export goods and services”:

- Activities of training and teaching jobs as well as selecting laborers for export shall not be subject to VAT.

- Labor export activities shall enjoy the VAT rate of 0% and be entitled to input VAT credit or refund.

The Finance Ministry shall guide and clarify job training and teaching as well as labor export activities. Where enterprises have or have not declared and paid VAT for such activities before the implementation of this Official Letter, the collection of tax arrears and tax refunding shall not apply.

|

|

FOR THE MINISTER OF FINANCE |