Nội dung toàn văn Official Dispatch No. 12366/BTC-TCHQ 2013 import tax VAT and customs procedures export processing companies

|

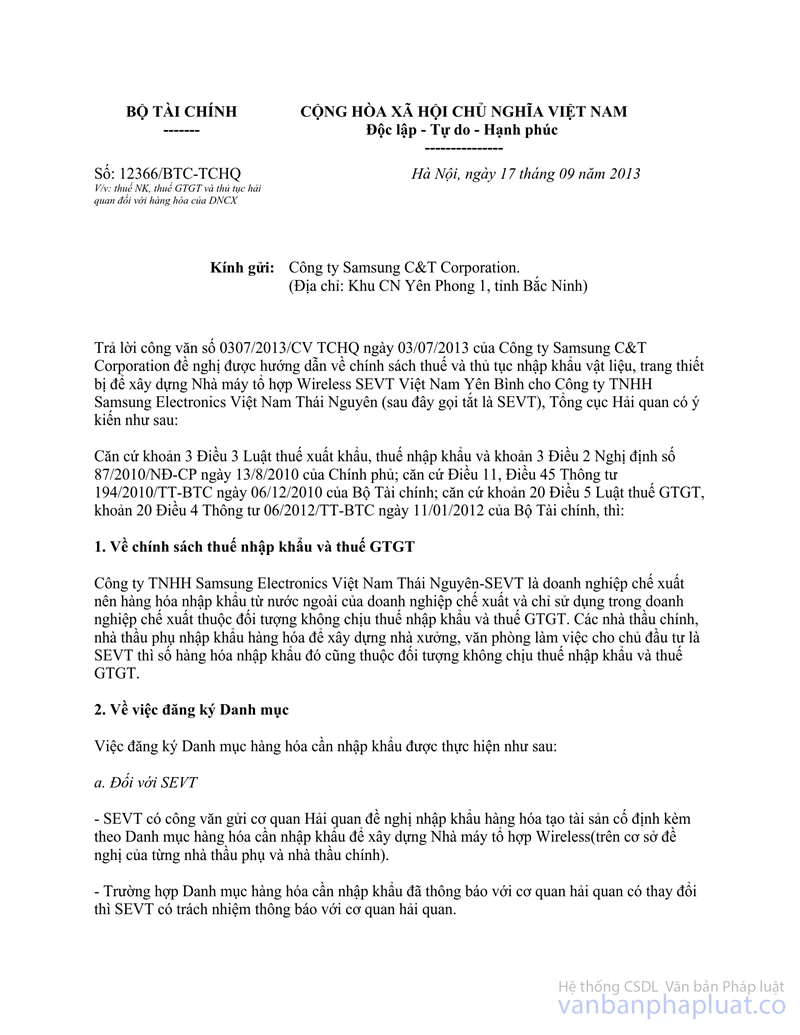

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 12366/BTC-TCHQ |

Hanoi, September 17, 2013 |

|

To: |

Samsung C&T Corporation. |

In response to the Dispatch No. 0307/2013/CV TCHQ dated July 03, 2013 of Samsung C&T Corporation requesting guidance on tax policies and procedure for importing raw materials and equipment to construct SEVT Vietnam Yen Binh Wireless complex for Samsung Electronics Vietnam LLC. In Thai Nguyen (hereinafter referred to as SEVT),

Pursuant to Clause 3 Article 3 of the Law on Export and import tax and Clause 3 Article 2 of the Decree No. 87/2010/NĐ-CP date August 13, 2013; Pursuant to Article 11 and Article 45 of the Circular No. 194/2010/TT-BTC dated December 06, 2010 of the Ministry of Finance; Pursuant to Clause 20 Article 5 of the Law on Value-added tax, Clause 20 Article 4 of the Circular No. 06/2012/TT-BTC dated January 11, 2012,

1. Import tax and VAT

SEVT is a export processing company, thus its goods that are imported from abroad for internal use are exempt from import tax and VAT. Goods imported by general contractors and subcontractors to build workshops and offices for the investor SEVT are also exempt from import tax and VAT.

2. Registration

The List of goods to be imported shall be registered as follows:

a. For SEVT:

- SEVT shall send a written request to the customs authority for permission to import goods to form fixed assets, enclosed with the list of goods to be imported for the construction of Wireless complex (based on the request of every subcontractor and the general contractor).

- SEVT shall notify the customs authority if any change to the List of goods to be imported, which has been submitted to the customs authority, is made.

- SEVT is responsible before the law for the use of goods for the construction of Wireless complex. If the goods in the List submitted to the customs authority are not completely used when the project is finished and then sold to the domestic market, the contractors whose names are on the import declaration shall make tax statement and pay tax in accordance with the Law on Export, import tax and its guiding documents.

b. For the general contractor and subcontractors of SEVT

- The general contractor and subcontractors may make declarations of goods imported for constructing Wireless complex according to the List of imported goods made by SEVT. The customs dossier must comply with current regulations and enclosed with the general contract. If the declaration is made by a subcontractor, it must be enclosed with a contract between the general contractor and the subcontractor;

- When the construction is finished, the general contractor and subcontractor shall follow the procedure for finalization at the customs authority based on the as-built dossier.

3. Customs procedure

Contractors must comply with regulations on customs dossiers in Article 11 and regulations on customs procedures applicable to goods exported and imported by export processing company in Article 45 of the Circular No. 194/2010/TT-BTC dated December 06, 2010 of the Ministry of Finance. Furthermore, when importing goods the contractors must send the customs authority: the notice of successful bid or the notice of contractor appointment (specifying the contents) enclosed with the contracts to sell goods to companies according to the bidding result or sale contracts, specifying that the successful bid or sale prices are exclusive of import tax, excise duty, and VAT.

Foreign contractors shall comply with the Decision No. 87/2004/QĐ-TTg dated May 10, 2004, the Decision No. 03/2012/QĐ-TTg dated January 16, 2012 on amendments to the Regulation on involvement of foreign contractors in construction in Vietnam, promulgated together with the Decision No. 87/2004/QĐ-TTg and relevant documents.

Point a Clause 3 Article 45 of the Circular No. 194/2010/TT-BTC dated December 06, 2010 of the Ministry of Finance shall apply to the goods imported from abroad that are transported directly to the construction site of Wireless complex.

The Customs Department of Bac Ninh province shall strictly supervise the import and use of the investor, the general contractor, and subcontractors. Difficulties that arise shall be reported to the General Department of Customs for instructions.

Samsung C&T Corporation is responsible for following the aforesaid instructions./.

|

|

PP THE DIRECTOR OF THE GENERAL

DEPARTMENT OF CUSTOMS |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments