Nội dung toàn văn Official Dispatch No. 1330/TCT-HTQT on interests on foreign banks’ loans under

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 1330/TCT-HTQT |

Hanoi, April 06, 2007 |

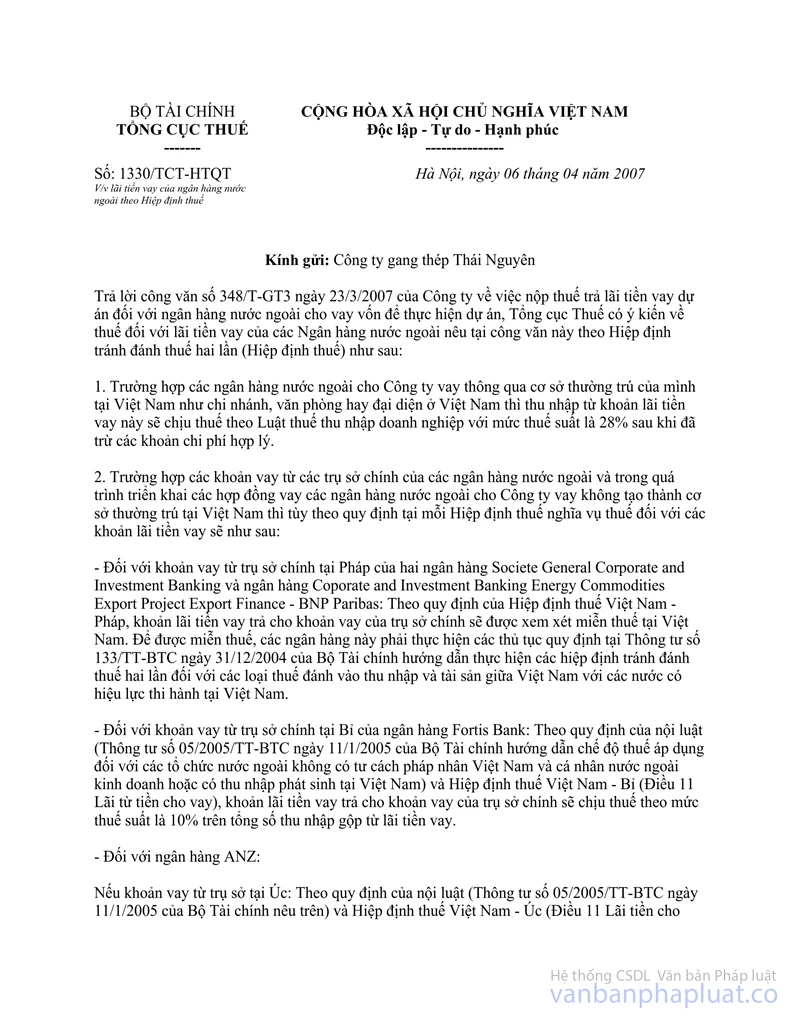

OFFICIAL LETTER

ON INTERESTS ON FOREIGN BANKS’ LOANS UNDER TAX AGREEMENTS

To: Thai Nguyen Pig Iron and Steel Company

In response to the Company’s Official Letter No. 348/T-GT3 of March 23, 2007, on the payment of tax on interests on loans provided by foreign banks for the execution of projects, in this Official Letter the General Department of Taxation gives its opinions regarding taxation of interests on foreign banks’ loans according to the Agreement on Double Taxation Avoidance (Tax Agreement) as follows:

1. If loans are provided to the Company by foreign banks via their permanent establishments in Vietnam such as branches or representative offices, income from interests on those loans is taxable at the rate of 28% under the Law on Business Income Tax after reasonable expenses are deducted.

2. If loans are provided to the Company by head offices of foreign banks and in the course of performance of loan contracts, foreign banks do not set up their permanent establishments in Vietnam, depending on the provisions of each Tax Agreement, their tax liabilities for loan interests are specified as follows:

- For loans provided by the France-based head offices of the two banks of Societe General Corporate and Investment Banking, and Corporate and Investment Banking Energy Commodities Export Project Export Finance - BNP Paribas: According to the provisions of the Vietnam-France Tax Agreement, interests on the loans provided by the head offices may be considered for tax exemption in Vietnam. To be entitled of tax exemption, these banks shall carry out the procedures specified in the Finance Ministry’s Circular No. 133/2004/TT-BTC of December 31, 2004, guiding the implementation of double taxation avoidance agreements with regard to taxes on income and assets, which are signed between Vietnam and other countries and taking effect in Vietnam.

- For loans provided by the Belgium-based head office of Fortis Bank: According to the domestic law (the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005, guiding the tax regime applicable to foreign organizations without Vietnamese legal person status and foreign individuals doing business or earning incomes in Vietnam) and the Vietnam-Belgium Tax Agreement (Article 11 on loan interests), interests on loans provided by the head office are taxable at the rate of 10% of the total income from interests.

- For ANZ Bank:

For loans provided by the Australia-based head office: According to the domestic law (the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005) and the Vietnam-Australia Tax Agreement (Article 11 on loan interests), interests on loans provided by the head office are taxable at the rate of 10% of the total income from interests.

For loans provided by the New Zealand-based head office: At present, there is no tax agreement between Vietnam and New Zealand, therefore, according to the provisions of domestic law (the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005), interests on loans provided by the head office are taxable at the rate of 10% of the total income from interests.

The General Department of Taxation would like to notify its opinions to the Company for information.

|

|

FOR THE GENERAL DIRECTOR OF

TAXATION |