Nội dung toàn văn Official Dispatch No. 13721/BTC-TCT of October 11, 2007, on tax policies for capital transfer

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 13721/BTC-TCT |

Hanoi, October 11, 2007 |

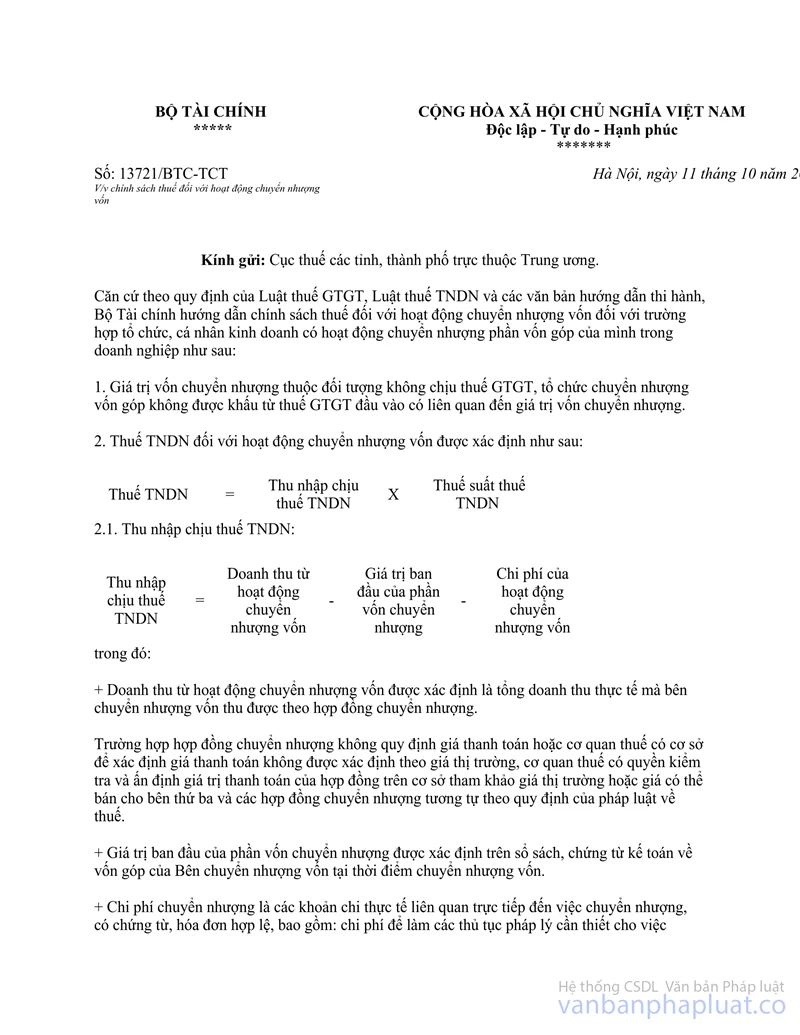

To: Provincial/Municipal Tax Departments

Basing itself on the provisions of the Law on Value Added Tax (VAT), the Law on Business Income Tax (BIT) and guiding documents, the Ministry of Finance hereby guides tax policies for capital transfer in case business organizations or individuals transfer their contributed capital in enterprises as follows:

1. The value of the transferred capital is not subject to VAT, therefore, organizations that transfer their contributed capital are not entitled to input VAT credit related to the value of the transferred capital.

2. BIT on capital transfer incomes is determined as follows:

BIT amount = BIT-liable income x BIT rate

2.1. Income subject to BIT:

|

BIT-liable income |

= |

Capital transfer turnover |

- |

The initial value of the transferred capital |

- |

Capital transfer expenses |

In which:

+ Capital transfer turnover is determined as the total turnover actually received by the transferor under the transfer contract.

When the transfer contract does not specify the payment price or the tax agency has grounds to believe that the payment price is not based on market prices, the tax agency may conduct examination and determine the contractual payment price on the basis of reference to market prices, prices which may be offered to a third party or prices of similar transfer contracts as prescribed by tax laws.

+ The initial value of the transferred capital is determined on books and accounting vouchers on the contributed capital of the transferor at the time of capital transfer.

+ Transfer expenses are actual expenditures with lawful vouchers and invoices directly related to the transfer, including: expenses for carrying out necessary legal procedures for the transfer; charges and fees paid upon carrying out transfer procedures; expenses for transactions, negotiation and signing of the transfer contract and other expenses with payment proofs.

2.2. BIT rates:

For foreign-invested enterprises: The BIT rate of 25% is applied to capital transfers arisen from December 31, 2003 backward. From January 1, 2004, the tax rate of 28% is applied; enterprises are not entitled to BIT exemption or reduction.

For other enterprises: The BIT rates comply with their major business activities.

2.3. Tax declaration and payment:

a/ If the transferor is a foreign organization or individual:

The transferee shall declare and determine the payable BIT amount, withhold and pay tax for the transferor. The transferee shall submit a tax declaration dossier to the tax agency where the enterprise of the transferor has registered tax payment.

b/ If the transferor is a Vietnamese organization or individual:

The transferor shall declare and determine the payable BIT amount. The transferor shall submit a tax declaration dossier to the tax agency where he/she/it has registered tax payment.

c/ A dossier of tax declaration for capital transfer incomes comprises:

- A declaration of BIT on capital transfer (made according to the form issued together with this Official Letter);

- A copy of the transfer contract. In case the transfer contract is made in a foreign language, the following major contents must be translated into Vietnamese: the transferor; the transferee; the transfer time; the transfer contents; rights and obligations of each party; the contract value; and the payment time, mode and currency.

- A copy of the decision approving the capital transfer, issued by a competent agency (if any);

- A copy of the capital contribution certificate, enclosed with the certification of capital-contributing parties;

- Original vouchers of expenses.

The Ministry of Finance gives this notice to provincial/municipal Tax Departments for information and compliance.

|

|

FOR THE MINISTER OF FINANCE |