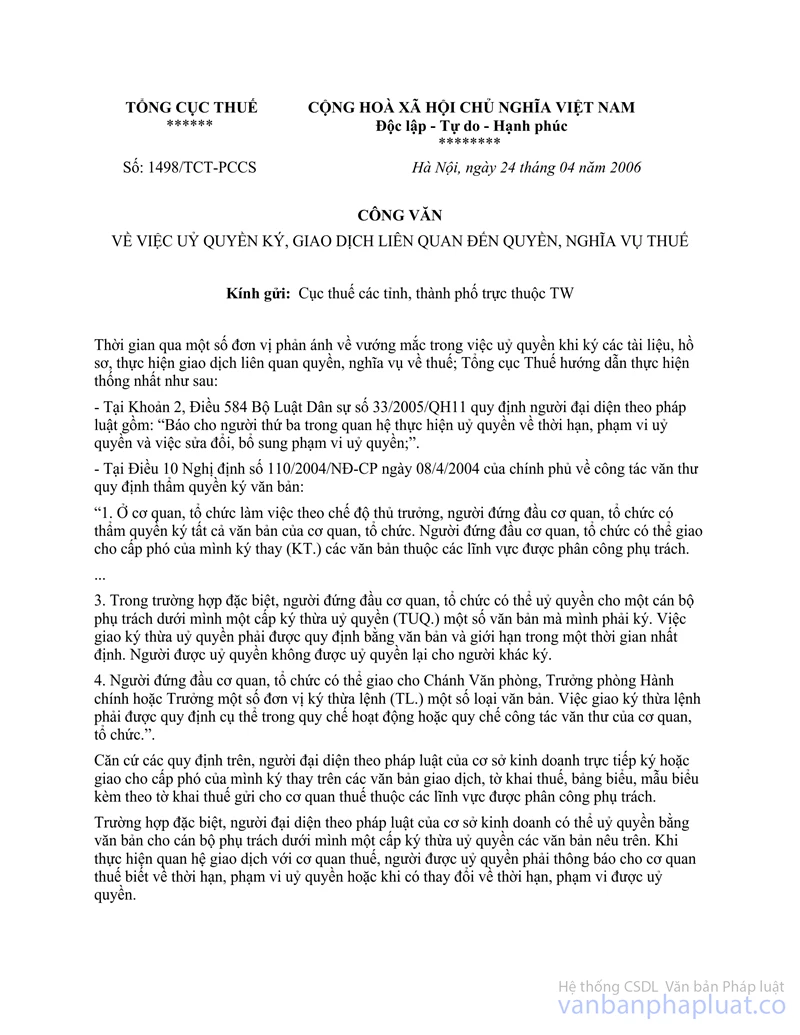

Nội dung toàn văn Official dispatch No.1498/TCT-PCCS mandate for conclusion transaction activities

|

THE GENERAL DEPARTMENT OF TAXATION |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 1498/TCT-PCCS |

Hanoi, April 24, 2006 |

OFFICIAL DISPATCH

ON MANDATE FOR CONCLUSION AND TRANSACTION ACTIVITIES RELATED TO TAX RIGHTS AND OBLIGATIONS

Respectfully to: The Departments of Taxation of central-affiliated cities and provinces

In the recent time, some units reflect about problems in mandate for signing the documents, records, implementing transactions related to tax rights and obligations; General Department of Taxation guide the unified implementation as follows:

- At clause 2, Article 584 of the Civil Code No. 33/2005/QH11 provides for legal representatives included: "To notify a third party concerned with the performance of the mandate of the mandate time limit and scope as well as any amendments or additions to the scope of mandate;".

- At Article 10 of the Government’s Decree No. 110/2004/ND-CP dated 08/4/2004 on clerical work provides for authority of signing documents:

“1. At agencies or organizations operating according to the regime decided by heads, heads of agencies or organizations have competence to sign all documents of their agencies or organizations. Heads of agencies or organizations may assign their deputies to sign on behalf of heads (On behalf of) For documents under the assigned fields.

...

3. In special case, heads of agencies or organizations may authorize for a cadre at level lower than one level for signing under mandate. For some documents that heads must sign. The assignment for signing under mandate must be prescribed in writing and limited in a definite duration. The authorized persons are not permitted to re-authorize for other person in signing.

4. Heads of agencies or organizations may assign the Chief of office, head of Administrative division or head of some units for signing under order for some documents. The assignment for signing under order must be specified in the operational regulation or regulation on clerical work of agencies or organizations.”.

Based on the above provisions, legal representatives of business establishments may directly sign or assign their deputies for signing on behalf of them in transaction documents, tax declarations, tables, forms enclosed with tax declarations to send to taxation agencies under the assigned fields

In special case, legal representatives of business establishments may authorize in writing for a cadre at level lower than one level for signing under mandate in the mentioned-above documents. When implementing transaction relations with taxation agencies, the authorized persons must notify taxation agencies about the mandate time limit and scope as well as any amendments or additions to the time limit or scope of mandate.

Particularly for enterprises, cooperatives just been established, documents in dossier of first tax registration, documents in dossier of buying invoices for the first time must be signed by their legal representatives with a seal to be consider as valid.

General Department of Taxation notifies Departments of Taxation for information and implementation.

|

|

FOR THE

GENERAL DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is translated by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments