Nội dung toàn văn Official Dispatch No. 1648/TCT-DTNN, On taxes applicable to foreign contractors

|

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No.

1648/TCT-DTNN |

Hanoi, May 9, 2006 |

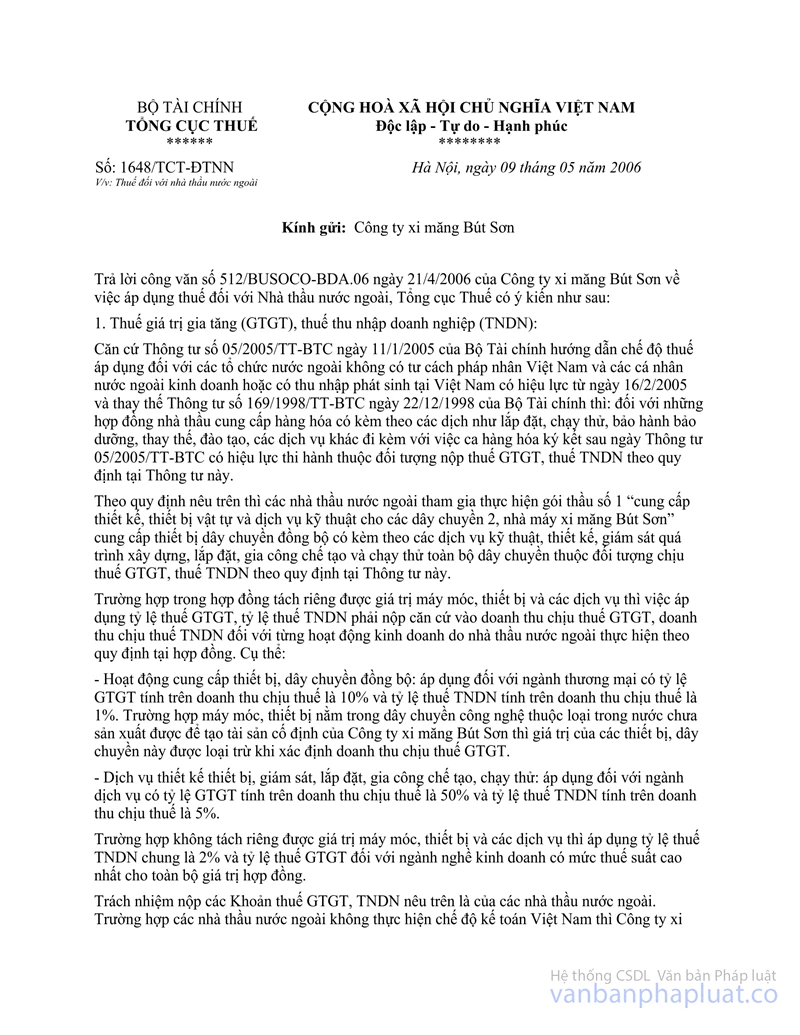

To: But Son Cement Company

In response to Official Letter No. 512/BUSOCO-BDA06 dated April 21, 2006 of But Son Cement Company, inquiring about the application of taxes to foreign contractors, the General Department of Taxation gives the following opinions:

1. Regarding value added tax (VAT) and business income tax (BIT):

Under the Finance Ministry's Circular No. 05/2005/TT-BTC of January 11, 2005, guiding taxes applicable to foreign organizations without Vietnamese legal person status and foreign individuals doing business or earning incomes in Vietnam, which took effect on February 16, 2005 and replaced the Finance Ministry's Circular No. 169/1998/TT-BTC of December 22, 1998, contracts signed after the effective date of Circular No. 05/2005/TT-BTC for supply of goods accompanied with such services as installation, test operation, warranty, maintenance, replacement, training and other services shall be liable to VAT and BIT according to the provisions of this Circular.

According to the aforesaid provisions, foreign contractors that jointly perform contractual package 1 for "supply of designs, equipment, supplies and technical services for projects on the second chain of But Son Cement Plant," supplying equipment in complete chains accompanied with technical services and services of engineering and supervising the construction, installation, manufacture and test operation of the whole chain, shall be liable to pay VAT and BIT according to the provisions of this Circular.

Where the values of machinery, equipment and services in the contract can be separately accounted, the applicable VAT or BIT rate shall be based on the turnover liable to VAT or BIT from each business operation conducted by a foreign contractor under the contract. Specifically as follows:

- For the supply of equipment in complete technological chains: The VAT rate of 10% and the BIT rate of 1% on taxable turnover applicable to commercial authorities shall apply. If machinery and equipment in the technological chain for creation of fixed assets of But Son Cement Company cannot be manufactured at home yet, the value of such equipment and chain shall be excluded upon determining VAT-liable turnover.

- For services of engineering, supervision, installation, manufacture and test operation of equipment: The VAT rate shall apply to 50% of taxable turnover and the BIT rate of 5% on taxable turnover applicable to services shall apply.

Where the values of machinery, equipment and services cannot be separately accounted, the BIT rate of 2% and the VAT rate applicable to the business line subject to the highest tax rate shall apply to the whole contract value.

The responsibility to pay aforesaid VAT and BIT amounts shall rest with foreign contractors. Where foreign contractors do not practice the Vietnamese accounting regime, But Son Cement Company shall be responsible for withholding, declaring and paying such tax amounts into the state budget on foreign contractors' behalf before making payments to these contractors.

2. Regarding personal income tax (PIT):

Individuals working for foreign contractors shall pay PIT for incomes generated in the course of performing jobs of projects according to the provisions of the Ordinance on Income Tax on High Income-Earners and current guiding documents.

Above is the General Department of Taxation's answer to But Son Cement Company's inquiry, for the latter's knowledge and compliance.

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |