Nội dung toàn văn Official Dispatch No. 17526/BTC-TCT dated 2014 implementation the Law on amendments to tax Laws

|

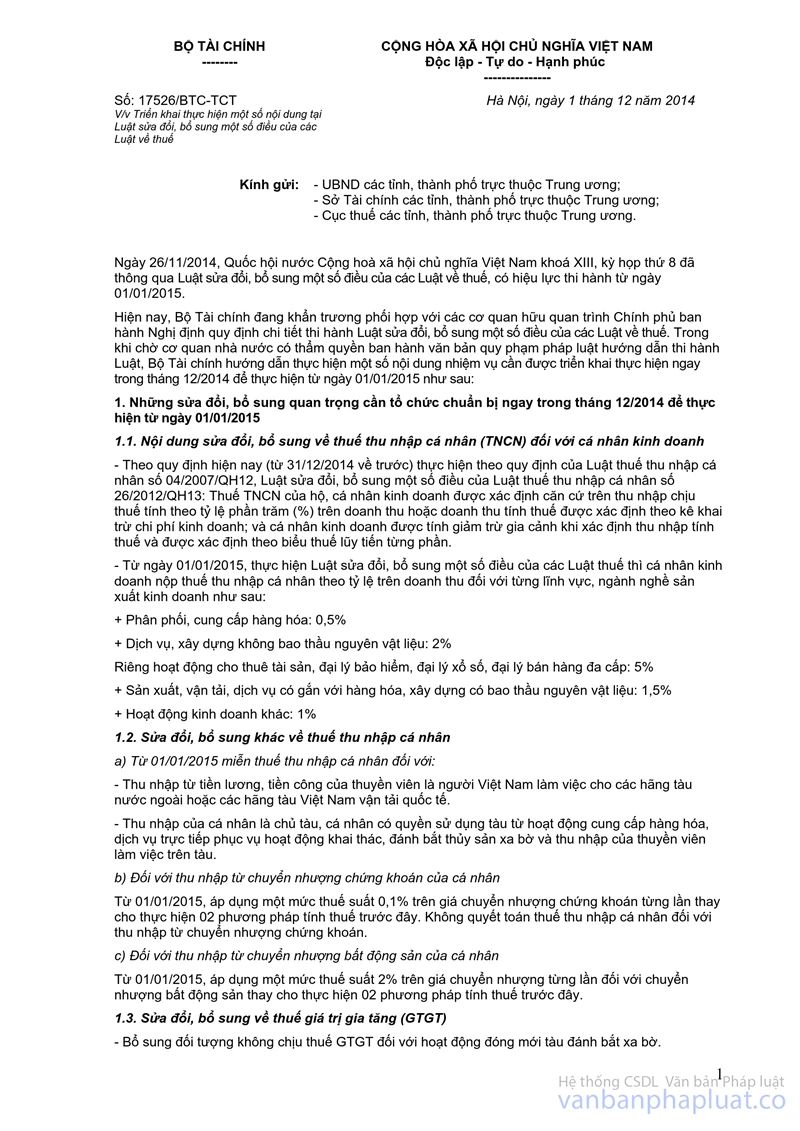

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

No.

17526/BTC-TCT |

Hanoi, December 01, 2014 |

|

To: |

- The

People’s Committees of provinces |

On November 26, 2014, the Law on Amendments to tax laws, which takes effect on January 01, 2015 is passed by the 13th National Assembly of Socialist Republic of Vietnam on November 26, 2014 during the 8th session.

The Ministry of Finance is now cooperating with agencies concerned and the Government in promulgating a Decree on guidelines for the Law on Amendments to tax laws Before legislative documents on guidelines for the said law are promulgated, the Ministry of Finance hereby provide guidance on some tasks that need commencing within December 2014 in order to be put into operation from January 01, 2015:

1. Important amendments that need to preparation within December 2014 and in order to be put into operation from January 01, 2015

1.1. Changes in personal income tax (PIT) incurred by sole traders

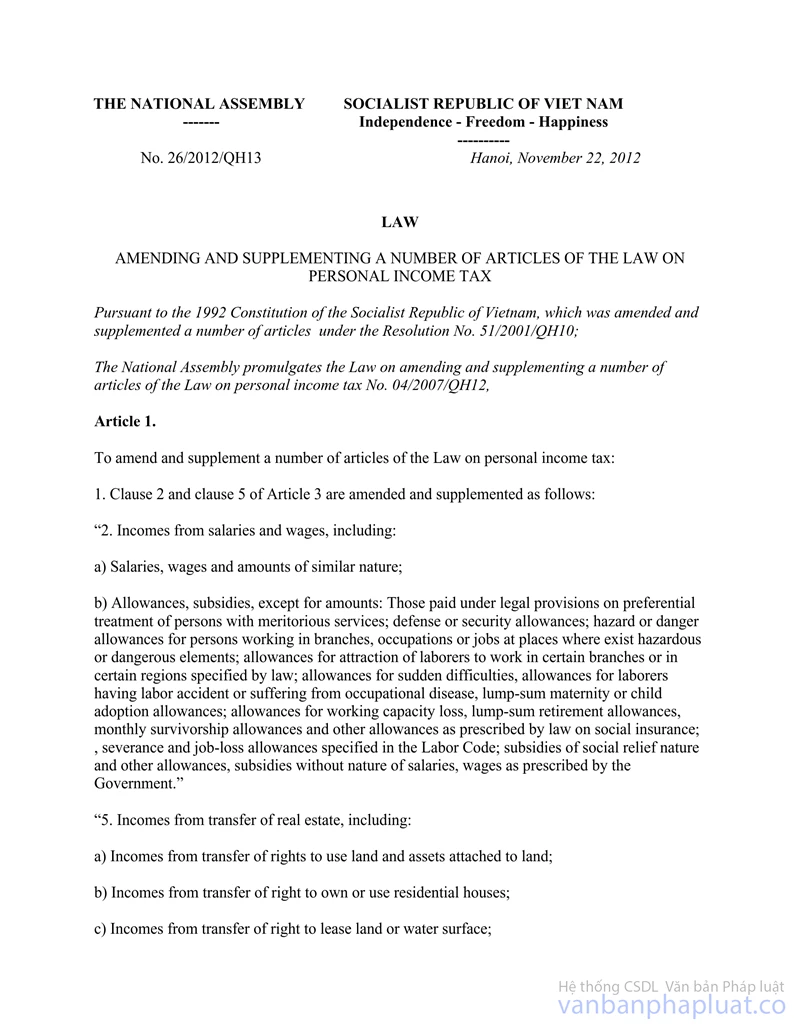

- According to current regulations (December 31, 2014 and earlier) of the Law on PIT No. 04/2007/QH12, the Law No. 26/2012/QH13 on amendments to the Law on PIT: PIT on taxable incomes of business households and sole traders depends is a percentage (%) of the income which equals (=) revenue or assessable revenue minus (-) operating costs; sole traders may claim family deductions when calculating assessable income. Family deductions are determined according to the progressive tax schedule.

- From January 01, 2015, according to the Law on Amendments to tax laws, sole traders shall pay PIT directly on their incomes from the following activities:

+ Distribution, supply of goods: 0.5%;

+ Service provision, construction exclusive of building materials: 2%.

Asset lease, insurance brokerage, lottery brokerage, multi-level marketing brokerage: 5%;

+ Manufacturing, transport, services associated with goods, construction inclusive of building materials: 1.5%.

+ Other business activities: 1%

1.2. Other changes in PIT

a) From January 01, 2015, PIT on the following incomes are exempt:

- Income from salaries, remunerations of Vietnamese crewmembers working for foreign shipping companies or Vietnamese shipping companies that provide international transport services.

- Incomes from provision of goods/services directly serving offshore fishing earned by individuals being ship owners, individuals having the right to use ships, and incomes of crewmembers on ships.

b) With regard to incomes of individuals from securities transfer

From January 01, 2015, 0.1% tax shall be imposed on the price of each securities transfer instead of applying the 02 previous methods. PIT on securities transfer shall not be recalculated at the end of the year.

c) With regard to incomes of individuals from real estate transfer

From January 01, 2015, 2% tax shall be imposed on the value of each real estate transfer instead of applying the 02 previous methods.

1.3. Changes to value-added tax (VAT)

- Building of ships serving offshore fishing is not subject to VAT.

- Three groups of goods including fertilizers, animal feeds, specialized machinery and equipment serving agricultural production, which were previously subject to 5% VAT, are now no longer subject to VAT.

1.4. Changes to severance tax

- Natural water used for agriculture, forestry, aquaculture, and salt production are now no longer subject to severance tax.

2. Regulations on tax administration applied sole traders to be carried out within December 2014 in order to be put into operation from January 01, 2015

2.1. With regard to sole traders paying flat tax

According to the Law on Tax administration, in December 2014, the People’s Committees of districts, Sub-departments of taxation shall instruct every business households and sole traders to implement important contents of the Law on PIT; print, hand out fliers, and instruct business households and sole traders to declare their revenue, which is the basis to determine the flat tax in 2015. Particularly:

a) Tax incurred by business households and sole traders:

- Business households and sole traders whose revenues exceed VND 100 million per year shall pay flat tax for 01 year.

- Determination of tax:

Monthly tax = (revenue subject to PIT in 01 month x PIT rate) + (flat revenue subject to VAT x VAT rate).

b) Tax declaration by business households and sole traders:

Business households and sole traders shall declare their revenue in order to determine flat tax in 2015 using form 01/THKH enclosed herewith.

Provincial Departments of Taxation, the People’s Committees of districts shall instruct Sub-department of taxation to cooperate with economics departments of communes to carry out on-site inspections to verify the revenues in each commune, each trade, especially those who provides food and drink services, transport services, trading, etc. in order to determine the correct taxable revenues of business households and sole traders, ensuring:

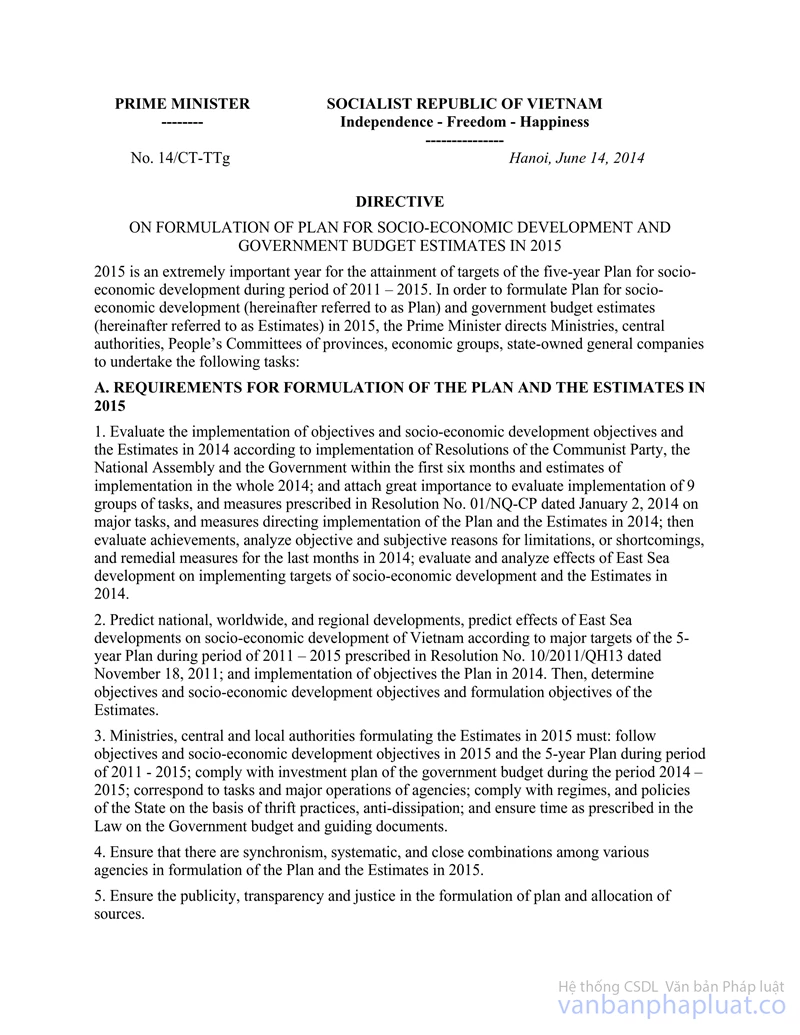

+ Tax is increased by at least 16% compared to tax in 2014 in accordance with the Prime Minister’s Directive No. 14/CT-TTg dated June 14, 2014 on development of socio-economic development plans and state budget estimate in 2015, which are congruous with economic growth and price index.

+ Ensure achievement of budget revenue targets 2015 set by the People’s Council of provinces and districts.

+ The revenue is congruous with the scale, scope of business, sufficient to cover investment costs and operating costs (rent for premises or the equivalent, costs of materials, electricity and water supply, cost prices of goods being sold; labor costs, and wages of employees, etc.)

Accordingly, Sub-departments of taxation shall estimate the revenues and flat tax in 2015, then post them at the People’s Committees of wards, communes, tax authorities, market management boards, etc. before December 25, 2014, and update the number of households, their revenues, tax, etc. on the database of Provincial Departments of Taxation and General Department of Taxation. Provincial Departments of Taxation shall carry out supervision and inspection in accordance with law, and send written remarks to each Sub-department of taxation before January 10, 2015, specifying the business households and sole traders whose business scale and revenues are not congruous. Based on such remarks, every Sub-department of taxation shall hold a meeting with the Tax Advisory Council of the ward or commune about flat tax and revenues in 2015 by January 10, 2015.

According to tax declarations submitted by business households and sole traders, survey result, minutes of meeting with the Tax Advisory Council, feedbacks on flat tax and revenues posted, and requests of Provincial Departments of Taxation, Sub-departments of taxation shall make and approve Tax registers before January 15, 2015. According to the approved Tax registered, Sub-departments of taxation and Provincial Departments of Taxation shall post information about taxpayers paying flat tax on the websites of tax authorities before January 30, 2015.

c) Sub-departments of taxation shall examine the business households and sole traders paying flat tax using previous methods and request them to apply for company registration if they hire 10 employees or more as prescribed by Company law. If the requirements for company establishment are not satisfied, business households and sole traders paying flat tax shall declare tax using form 01/THKH.

2.2. With regard to individuals leasing out assets (hereinafter referred to as lessors)

a) Tax on lease of assets by households and individuals coming into force from January 01, 2015.

- If an individual has a lease contract which is effective for many years and has declared, paid tax according to previous regulations, the tax declared and paid shall not be adjusted.

- Sub-departments of taxation shall instruct lessor to declare tax on the rents from January 01, 2015, which is the basis for calculating VAT and PIT, using form No. 01/KK-TTS enclosed herewith. Sub-departments of taxation shall determine the rents according to the asset lease market in the district or similar districts.

Every lessor shall declare tax only once on each lease contract, and pay tax directly according to the payment term on the contract to State Treasury or a commercial bank authorized by the State to collect government budget revenues as instructed by General Department of Taxation.

b) Tax administration regulations of Provincial Departments of Taxation and Sub-departments of taxation applied to lease of assets.

- Sub-department of taxation shall cooperate with local regulatory bodies (real estate authority, residence authority, etc.) in managing the households and individuals having houses for lease; take measures against asset lease under the guise of lending, free stay, etc. in order to avoid paying tax.

- According to land prices imposed by the People’s Committees of provinces, construction prices, house rents, average rent for real estate, vehicles, and other assets, Provincial Departments of Taxation and Sub-departments of taxation shall develop a database of rents for real estate and assets in each province and district, sorted by street and type of asset (car, ship, etc.). The database is the basis for tax administration, determination of risks, and consultation on tax inspection with regard to lessor.

Above are some regulations that need implementing within December 2014 in order to be put into operation from January 01, 2015. The Ministry of Finance hereby requests the People’s Committees of provinces to instruct Provincial Departments of Taxation, the People’s Committees of districts, and relevant agencies in promptly implementing the Law on Amendments to tax laws. The Ministry of Finance requests Directors of Provincial Departments of Taxation and Sub-departments of taxation to provide training for their officials, organize propagation, and instruct every taxpayer to implement important contents of the Law on Amendments to tax laws.

The People’s Committees, Provincial Departments of Taxation, and Sub-departments of taxation shall report the difficulties that arise during the implementation to the Ministry of Finance at www.mof.gov.vn for prompt instruction./.

|

|

PP MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed