Nội dung toàn văn Official Dispatch No. 2387/TCT-CS on the determination of conditions for entitle

|

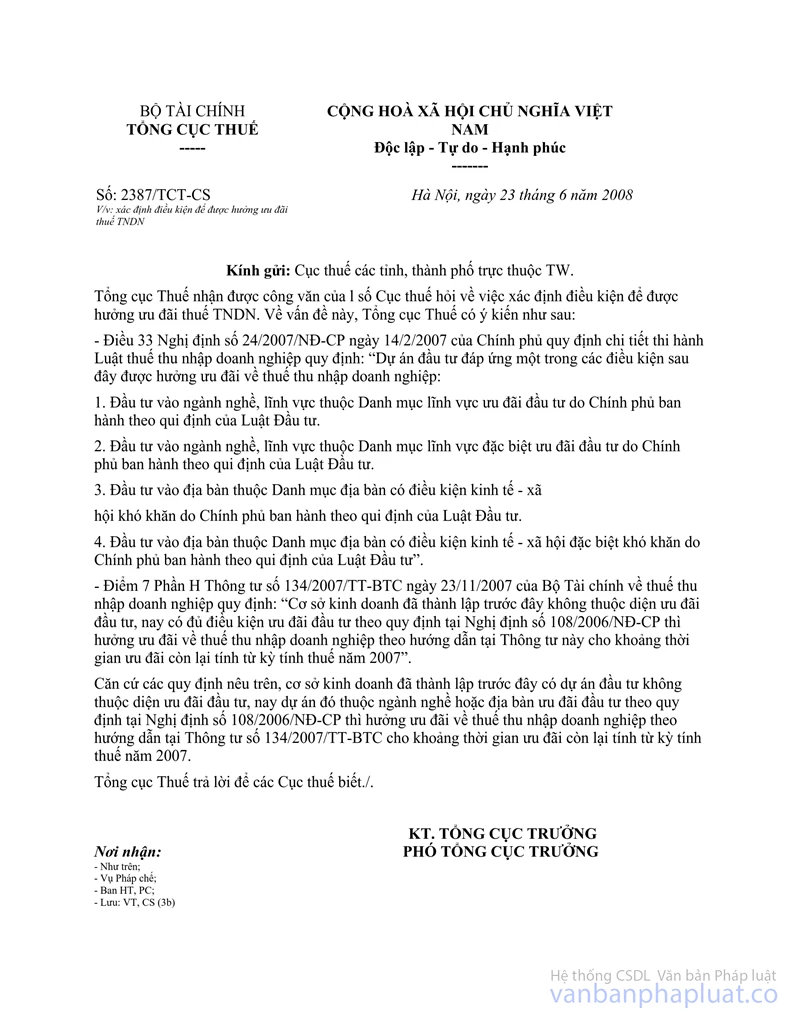

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 2387/TCT-CS |

Hanoi, June 23, 2008 |

OFFICIAL LETTER

ON THE DETERMINATION OF CONDITIONS FOR ENTITLEMENT TO BUSINESS INCOME TAX (BIT) INCENTIVES

To: Provincial Tax Offices

The General Department of Taxation has received official letters from several Provincial Tax Offices inquiring about the determination of conditions for entitlement to BIT incentives. Regarding this matter, the General Department of Taxation has the following opinions:

- Article 33 of the Government’s Decree No. 24/2007/ND-CP of February 14, 2007, detailing the implementation of the BIT Law, stipulates: “Investment projects that satisfy one of the following conditions are entitled to BIT incentives:

1. Investing in business lines or domains in the list of domains entitled to investment incentives issued by the Government under the Investment Law.

2. Investing in business lines or domains in the list of domains entitled to special investment incentives issued by the Government under the Investment Law.

3. Investing in geographical areas in the list of geographical areas with socio-economic difficulties issued by the Government under the Investment Law.

4. Investing in geographical areas in the list of geographical areas with extreme socio-economic difficulties promulgated by the Government under the Investment Law.

- Point 7, Part H of the Finance Ministry’s Circular No. 134/2007/TT-BTC of November 23, 2007, on BIT stipulates: “Business establishments already set up which were not eligible for investment incentives but now satisfy the conditions for investment incentives specified in Decree No. 108/2006/ND-CP will enjoy BIT incentives under the guidance in this Circular for the remaining preferential time starting from the 2007 tax period.”

According to the above-mentioned regulations, business establishments having investment projects which were not eligible for investment incentives but now belong to business lines or geographical areas eligible for investment incentives under Decree No. 108/2006/ND-CP will enjoy BIT incentives under the guidance in Circular No. 134/2007/TT-BTC for the remaining preferential time counting from the 2007 tax period.

The General Department of Taxation notifies Provincial Tax Offices thereof for implementation.

|

|

FOR THE GENERAL DIRECTOR OF

TAXATION |