Nội dung toàn văn Official Dispatch No. 258 TCT/DNK of January 19, 2005, on the application of value added tax (VAT) rates

|

THE

GENERAL DEPARTMENT OF TAXATION |

SOCIALIST

REPUBLIC OF VIET NAM |

|

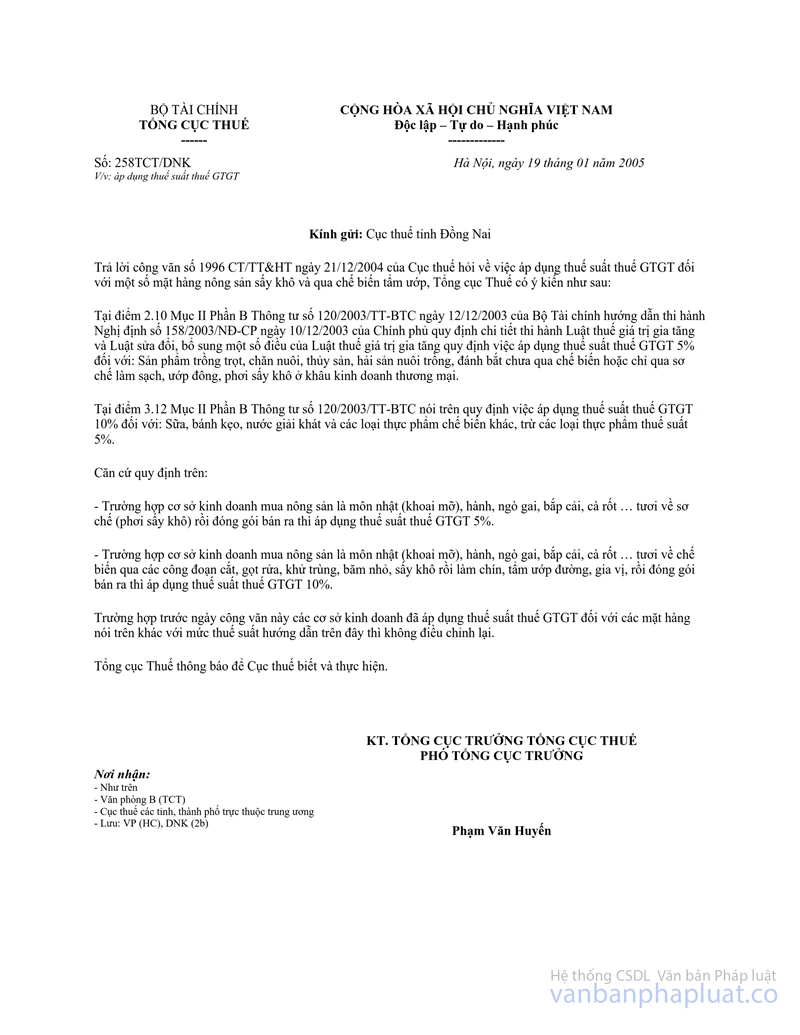

No. 258 TCT/DNK |

Hanoi, January 19, 2005 |

OFFICIAL LETTER

ON THE APPLICATION OF VALUE ADDED TAX (VAT) RATES

To: Taxation Department of Dong Nai province

In response to Official Letter No. 1996 CT/TT&HT of December 21, 2004, of the Taxation Department of Dong Nai province, inquiring about the application of VAT rates to a number of dried or impregnated agricultural produce, the General Department of Taxation gives the following opinions:

Point 2.10, Section II, Part B of the Finance Ministry’s Circular No. 120/2003/TT-BTC of December 12, 2003, guiding the implementation of the Government’s Decree No. 158/2003/ND-CP of December 10, 2003, detailing the implementation of the VAT Law and the Law Amending and Supplementing a Number of Articles of the VAT Law, stipulates that the VAT rate of 5% is applicable to: Cultivation and husbandry products, cultured and fished aquatic and marine products that have not yet been processed or have been preliminarily processed by cleaning, freezing, or drying at the commercial business stage.

Point 3.12, Section II, Part B of the above-mentioned Circular No. 120/2003/TT-BTC stipulates that the VAT rate of 10% shall apply to milk, confectionery, beverages and other processed foodstuff, other than those subject to the VAT rate of 5%.

According to the aforesaid provisions:

- In cases where enterprises purchase fresh winged yams, onions, eryngoes, cabbages, carrots, etc., then undertake preliminary process (drying) and packing up them for sale, the VAT tax rate of 5% is applied .

- In cases where enterprises purchase fresh winged yams, onions, eryngoes, cabbages, carrots, etc., then process them by cutting, cleaning, disinfecting, mincing, drying, cooking, and impregnating with sugar or spices and put them on sale, the tax rate of 10% is applied.

Before the issuance of the Official Letter , if enterprises have applied VAT rates inconsistently with the above instruction , no adjustment is required for.

The General Department of Taxation hereby notifies the Taxation Department of Dong Nai province thereof as instruction for compliance.

|

|

ON

BEHALF OF THE GENERAL DIRECTOR OF TAXATION |