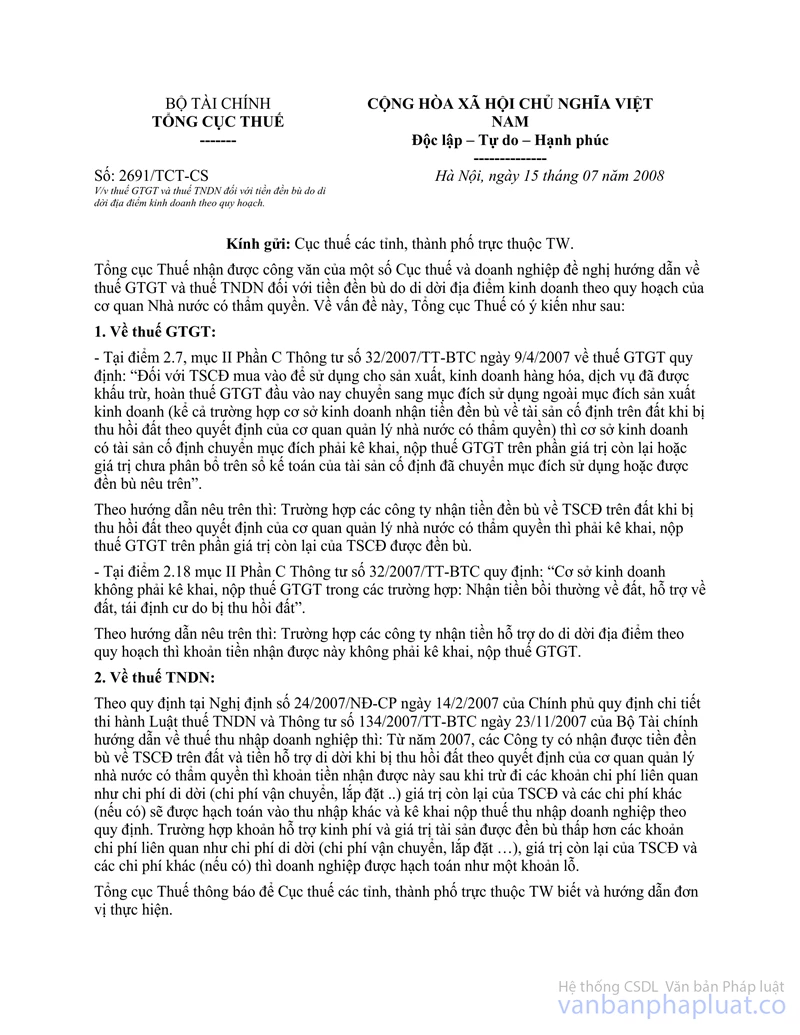

Nội dung toàn văn Official Dispatch No. 2691/TCT-CS on value added tax and business income tax on

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 2691/TCT-CS |

Hanoi, July 15, 2008 |

OFFICIAL LETTER

ON VALUE ADDED TAX AND BUSINESS INCOME TAX ON SUMS OF MONEY RECEIVED AS COMPENSATION FOR RELOCATION OF BUSINESS ESTABLISHMENTS UNDER PLANNING

To: Provincial Tax Offices

The General Department of Taxation has received official letters from several Provincial Tax Offices asking for guidance on value added tax (VAT) and business income tax (BIT) on sums of money received as compensation for relocation of business establishments under plannings of competent state agencies. Regarding this matter, the General Department of Taxation gives the following opinions:

1. Regarding VAT:

- Point 2.7, Section II, Part C of the Finance Ministry’s Circular No. 32/2007/TT-BTC of April 9, 2007, on VAT stipulates: “For fixed assets purchased for use in the production of and trading in goods and services for which input VAT has been credited or refunded, if they are then used for other non-production and trading purposes (including cases where business establishments receive compensation for fixed assets attached to land upon land recovery under decisions of competent state management agencies), business establishments shall declare and pay VAT on the above-metioned fixed assets according to their residual value or their book value which has not yet been allocated.

Under the above guidance, companies that receive compensation for fixed assets attached to land upon land recovery under decisions of competent state management agencies shall declare and pay VAT on the residual value of fixed assets for which compensation has been paid.

- Point 2.18, Section II, Part C of Circular No. 32/2007/TT-BTC stipulates: “Business establishments are not required to declare and pay VAT in the following cases: receiving compensation for land, supports for land and resettlement due to land recovery.”

Under the above guidance, companies that receive supports for relocation under plannings, they are not required to declare and pay VAT on the received amounts.

2. Regarding BIT:

According to the Government’s Decree No. 24/2007/ND-CP of February 14, 2007, detailing the implementation of the BIT Law and the Finance Ministry’s Circular No. 134/2007/TT-BTC of November 23, 2007, guiding BIT, as from 2007, if companies receive compensation for fixed assets attached to land and supports for relocation upon land recovery under decisions of competent state management agencies, the received amounts, after subtracting related expenses such as expenses for relocation (expenses for transportation, installation, etc.), the residual value of fixed assets and other expenses (if any) must be accounted into other incomes for BIT declaration and payment as prescribed. If the support amounts and the compensated value of assets are lower than related expenses such as expenses for relocation (expenses for transportation, installation), the residual value of fixed assets and other expenses (if any), enterprises may account them as a loss.

The General Department of Taxation informs to Provincial Tax Offices thereof for information and guidance for concerned units.

|

|

FOR THE GENERAL DIRECTOR OF

TAXATION |