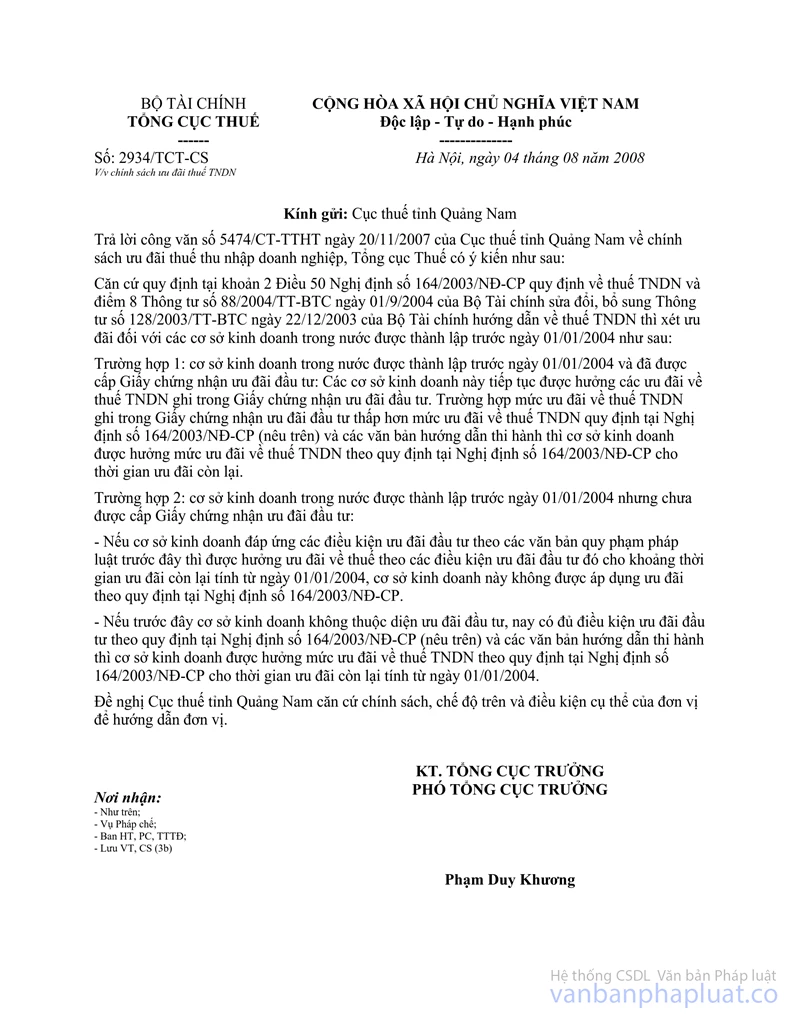

Nội dung toàn văn Official Dispatch No. 2934/TCT-CS on policies on business income tax incentives

|

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 2934/TCT-CS |

Hanoi, August 04, 2008 |

OFFICIAL LETTER

ON POLICIES ON BUSINESS INCOME TAX INCENTIVES

To: Quang Nam Province Tax Office

In reply to Official Letter No. 5474/CT-TTHT of November 20, 2007, of the Quang Nam Province Tax Office regarding the policy on business income tax (BIT) incentives, the General Department of Taxation gives the following opinions:

According to Clause 2, Article 50 of the Government’s Decree No. 164/2003/ND-CP on BIT and Point 8 of the Finance Ministry’s Circular No. 88/2004/TT-BTC of September 1, 2004, amending and supplementing Circular No. 128/2003/TT-BTC of December 22, 2003, providing guidance on BIT, the grant of incentives to domestic business establishments set up prior to January 1, 2004, complies with the following:

Case 1: Domestic business establishments that were set up prior to January 1, 2004, and have been granted investment preference certificates: They will continue enjoying BIT incentives stated in their investment preference certificates. If the levels of BIT incentives stated in their investment preference certificates are lower than those prescribed in Decree No. 164/2003/ND-CP and guiding documents, business establishments will enjoy the levels of BIT incentives prescribed in Decree No. 164/2003/ND-CP for the remaining preferential period.

Case 2: Domestic business establishments that were set up prior to January 1, 2004, but have not yet been granted investment preference certificates:

- If they satisfy the conditions for investment incentives specified in previous legal documents, they will enjoy tax incentives under these investment incentives for the remaining preferential period, starting from January 1, 2004; they are not entitled to incentives specified in Decree No. 164/2003/ND-CP.

- If they were previously ineligible for investment incentives but now satisfy conditions for investment incentives specified in Decree No. 164/2003/ND-CP and guiding documents, they will enjoy BIT incentives specified in Decree No. 164/2003/ND-CP for the remaining preferential period, starting from January 1, 2004.

The Quang Nam Province Tax Office should give guidance for the concerned units based on the above-mentioned policy and regulations.

|

|

FOR THE GENERAL DIRECTOR OF

TAXATION |