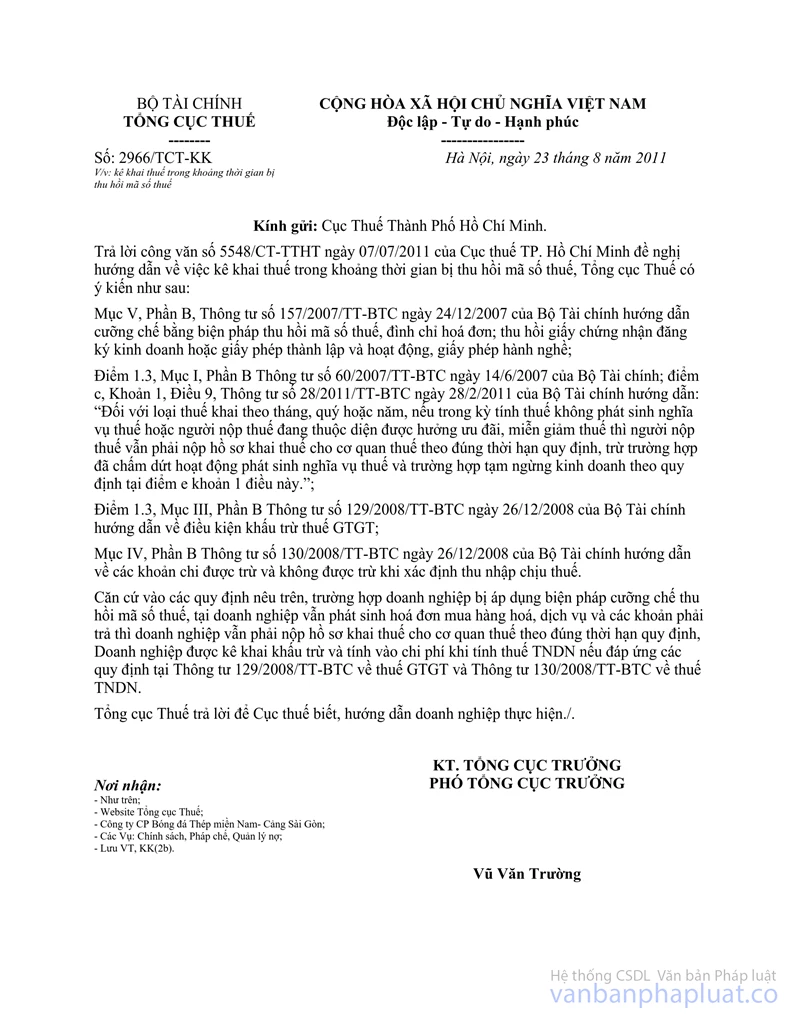

Nội dung toàn văn Official Dispatch No. 2966/TCT-KK on tax declaration in the time of tax code

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 2966/TCT-KK |

Hanoi, August 23, 2011 |

OFFICIAL DISPATCH

ON TAX DECLARATION IN THE TIME OF TAX CODE REDEMPTION

To: Department of Tax of Ho Chi Minh City

On answering the Official Dispatch No. 5548/CT-TTHT dated July 07, 2011 of the Department of Tax of Ho Chi Minh City on the proposal on guidance about tax declaration in the time of tax code redemption. The General Department of Tax has opinions as follows:

Section V, Part B of the Circular No. 157/2007/TT-BTC dated dated December 24, 2007 of the Ministry of Finance guiding the enforcement enforcement by withdrawal of tax identification numbers, suspension of use of invoices; revocation of business registration certificates or establishment and operation licenses or practice licenses.

Point 1.3, Section I, Part B of the Circular No. 60/2007/TT-BTC dated June 14, 2007 of the Ministry of Finance; point c, section 1, Article 9 of the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance guiding For taxes to be declared on a monthly, quarterly or yearly basis, if no tax obligation arises in a tax period or taxpayers are currently eligible for tax incentives, exemption or reduction, taxpayers shall still submit tax declaration dossiers to tax agencies within the set time limit, except for cases in which activities that give rise to the tax obligation have terminated and cases in which business operations are suspended under Point e, Clause 1 of this Article.

Point 1.3, Section II, Part B of the Circular No. 129/2008/TT-BTC dated December 26, 2008 of the Ministry of Finance guiding the conditions for VAT tax

Section IV, Part B of the Circular No. 130/2008/TT-BTC dated December 26, 2008 of the Ministry of Finance guiding on payments without being deducted when defining tax liable incomes.

Based on above regulations, in the case that enterprises applied compulsory measures on tax code redemption, enterprises must submit tax declaration dossiers to tax offices when having arising cases in invoices for trading goods and services or payable amount in accordance with regulated term. Enterprises are allowed to declare tax deduction and add to the expenses when calculating enterprise income tax if they can satisfy all regulations on the Circular No. 129/2008/TT-BTC on VAT and Circular No. 130/2008/TT-BTC on enterprise income tax.

The General Department of Tax answer the Department of Tax for acknowledgement and instructing enterprises to implement./.

|

|

FOR

THE GENERAL DIRECTORATE |