Nội dung toàn văn Official Dispatch No. 31 TCT/PCCS, On issuance of sanctioning decisions against

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 31 TCT/PCCS |

Hanoi, January 5, 2005 |

To: Provincial/municipal Tax Departments

In the course of sanctioning administrative violations in taxation domain, there remain different opinions on the sanctioning order and procedures for late payment of taxes and fines. For the uniform implementation of sanctions against acts of late payment of taxes and fines in the entire taxation administration, the General Department of Taxation hereby gives the following opinions:

Clause 9, Article 1 of the Law Amending and Supplementing a Number of Articles of the Value Added Tax Law stipulates: “…if past the tax payment deadline, business establishments still fail to pay taxes, to issue notices on payable tax amounts and fines on late tax payment…” Meanwhile, Clause 2, Article 15 of the current Enterprise Income Tax Law states: “To notify business establishments of their late submission of declarations and late payment of taxes as well as decisions on sanctioning of violations of tax law...”

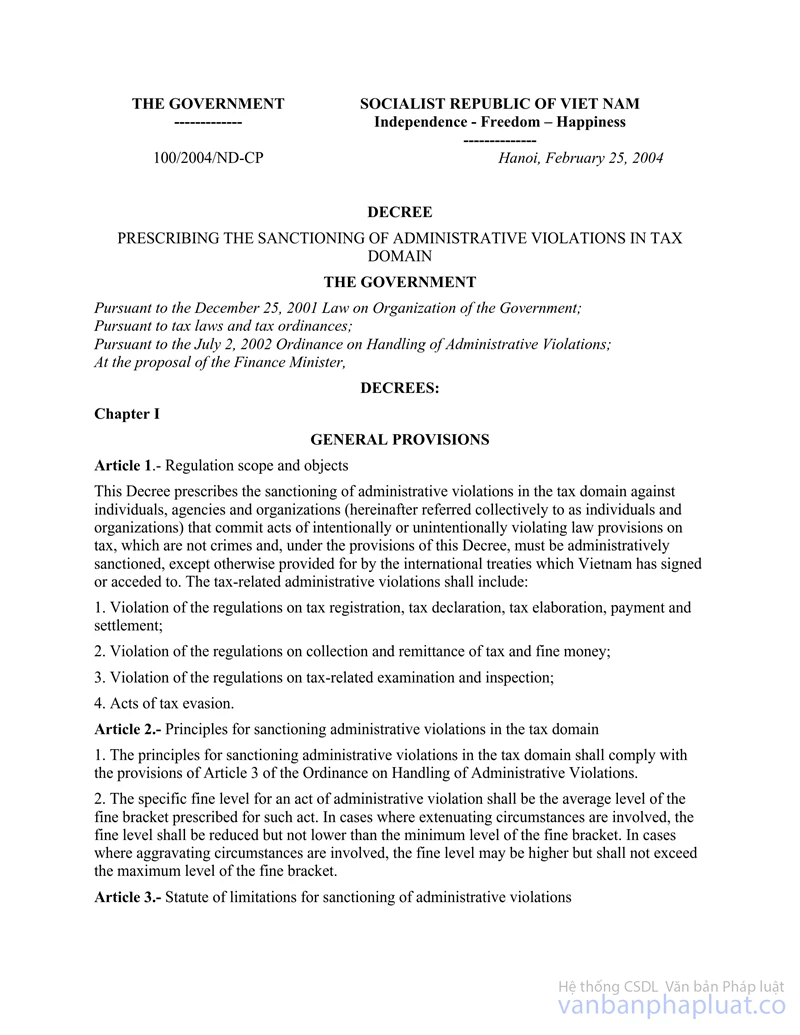

Article 9 of the Government’s Decree No. 100/2004/ND-CP of February 25, 2004 guides the sanctioning of violations in the collection of taxes and fines as follows: “To sanction under the provisions of tax law acts of paying taxes or fines beyond the payment deadlines stated in tax notices or sanctioning decisions. Where no tax notices have been issued, the fines for late tax payment shall be based on tax payment deadlines provided for in tax laws…”

According to Article 18 of the Government’s Decree No. 100/2004/ND-CP providing the sanctioning of administrative violations in the taxation domain, the forms, contents, order and procedures for issuance of administrative sanctioning decisions in the taxation domain must comply with the provisions of Article 56 of the Ordinance on Handling of Administrative Violations. Therefore, all administrative sanctions must be effected through administrative sanctioning decisions made according to the form enclosed with Decree No. 134/2003/ND-CP of November 14, 2003, detailing the implementation of a number of articles of the 2002 Ordinance on Handling of Administrative Violations.

The General Department of Taxation requests the provincial/municipal Tax Departments to comply with the Government’s Decree No. 100/2004/ND-CP of February 25, 2004, providing administrative sanctions in the taxation domain.

The General Department of Taxation notifies the provincial/ municipal Tax Departments thereof for knowledge and implementation.

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |