Nội dung toàn văn Official Dispatch No. 3387/TCT-CS tax customs for the P&G Company in Vietnam model of global business

|

MINISTRY OF

FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

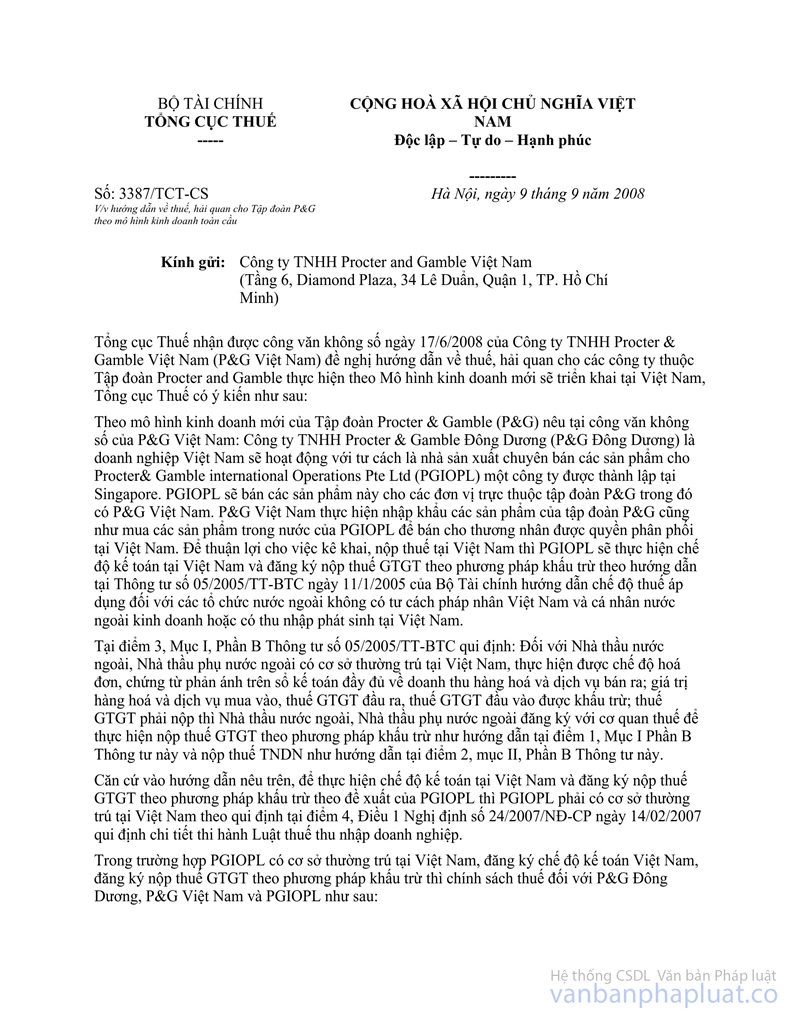

No.: 3387/TCT-CS S |

Hanoi, September 09, 2008 |

|

Respectfully to: |

The Vietnam Procter and Gamble Limited

Liability Company |

The General Department of Taxation has received official dispatch dated 17/6/2008 of the Vietnam Procter & Gamble Limited Liability Company (Vietnam P&G) requesting for guiding on tax, customs for companies of the Procter & Gamble Company in implementation under new business model which will be carried out in Vietnam, the General Department of Taxation has opinions as follows:

According to the new business model of the Procter & Gamble Company (P&G) mentioned at official dispatch of Vietnam P&G: The Indochina Procter & Gamble Limited Liability (Indochina P&G) is a Vietnam enterprise operating with status of a producer specialized in selling products of Procter& Gamble international Operations Pte Ltd (PGIOPL) which is a company established in Singapore. PGIOPL will sell these products to units affiliated P&G Corporation including Vietnam P&G. Vietnam P&G will import products of P&G Company as well as buy domestic products of PGIOPL to sell to traders that have right to distribute in Vietnam. In order to be convenient for tax declaration and payment in Vietnam, PGIOPL will perform the accounting regulation in Vietnam and register for VAT payment by deduction method in accordance with guide in Circular No. 05/2005/TT-BTC dated January 11, 2005 of the Ministry of Finance, guiding the tax regime applicable to foreign organizations without Vietnamese legal person status and foreign individuals doing business or earning incomes in Vietnam.

At point 3 section I, part B of Circular No. 05/2005/TT-BTC stipulates: For foreign contractors or subcontractors that have permanent establishments in Vietnam, keep invoices and documents and fully reflect on accounting books turnover from goods and services sold; the value of goods and services bought, output VAT; deductible input VAT and payable VAT, they shall register with the tax offices to pay VAT by deduction method as guided at Point 1, Section I, Part B of this Circular and to pay EIT as guided at Point 2, Section II, Part B of this Circular.

Based on guide mentioned above, to perform the accounting regime in Vietnam and register for VAT payment by deduction method at the request of PGIOPL, PGIOPL must have permanent establishment in Vietnam as prescribed at point 4, article 1 of Decree No. 24/2007/ND-CP dated February 14, 2007, detailing implementation of Law on enterprise income tax.

In case where PGIOPL haves permanent establishment in Vietnam, register for the accounting regime of Vietnam, register for VAT payment by deduction method, the Indochina P&G, Vietnam P&G and PGIOPL shall be applied the tax policy as follows:

1. About import duty and Value-added tax (VAT) and customs procedures for goods which are exported and sold to PGIOPL by the Indochina P&G; PGIOPL exports and sell goods to Vietnam P&G:

- For raw materials imported in Vietnam by the Indochina P&G, it must submit import duty, VAT and do customs procedures in accordance with current regulations.

- Because PGIOPL does business in Vietnam through permanent establishments, when the Indochina P&G sells goods to PGIOPL, this is relation involving domestic goods purchase and sale (not is export and import relation), the Indochina P&G must issue Value-added invoices for PGIOPL at the tax rates specified in Law on VAT and the guiding documents, since January 01, 2009 comply with the Law on VAT No. 13/2008/QH12.

- When PGIOPL sells goods to Vietnam P&G, this is domestic purchase and sale relation: PGIOPL may issue the Value-added invoices for goods sold at the tax rates specified in Law on VAT and guiding documents.

2. Obligations of VAT and enterprise income tax (EIT) of PGIOPL (through the permanent establishments in Vietnam):

- For VAT: PGIOPL declares and pays VAT in accordance with point 1 section I, part B of Circular No. 05/2005/TT-BTC.

- For EIT: PGIOPL declares and pays EIT in accordance with point 2, section I, part B of Circular No. 05/2005/TT-BTC and Double taxation agreement signed between Vietnam and Singapore.

From 1/1/2009, PGIOPL pays VAT, EIT in accordance with the Law on VAT No. 13/2008/QH12, Law on EIT No. 12/2008/QH12 and the guiding documents.

The General Department of Taxation replies to Vietnam P&G.

|

|

PP THE

GENERAL DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments