Nội dung toàn văn Official Dispatch No. 3504/NHNN-CSTT of May 15th, 2009, Implementation of interest rate support mechanism.

|

STATE

BANK OF VIETNAM |

SOCIALIST

REPUBLIC OF VIET NAM |

|

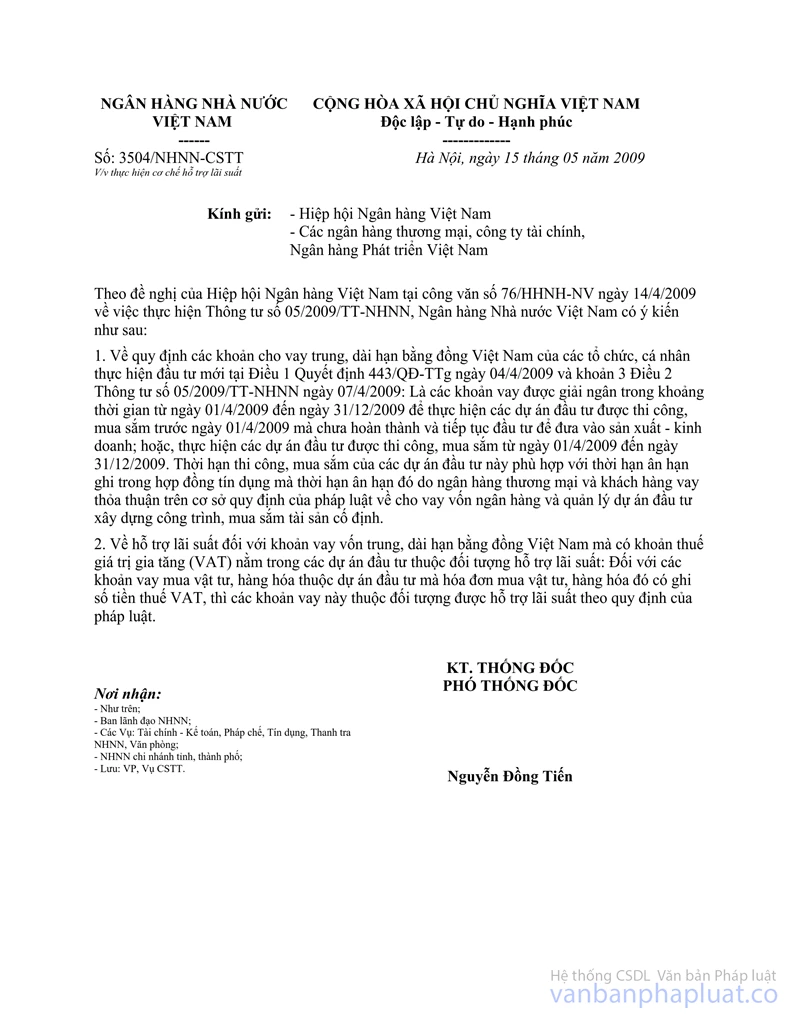

No. 3504/NHNN-CSTT |

Hanoi, May 15th, 2009 |

|

To: |

- Vietnam Banks Association |

Upon request of Vietnam Banks Association in the Official Dispatch No. 76/HHNH-NV dated 14 April 2009 on the implementation of the Circular No. 05/2009/TT-NHNN the State Bank of Vietnam hereby would like to give out its opinion as follows:

1. Regarding provisions on medium, long term loans in Vietnamese Dong of organizations, individuals for making new investment as stated in Article 1, Decision No. 443/QD-TTg dated 4 April 2009 and paragraph 3 Article 2 of the Circular No. 05/2009/TT-NHNN dated 7 April 2009: being loans to be disbursed during the period of time from 1 April 2009 to 31 December 2009 for implementing investment projects which were implemented, procured prior to 1 April 2009 and have not yet been completed and are still being invested to put into production- business; or implementing investment projects which are implemented, procured from 1 April 2009 to 31 December 2009. Duration of implementation, procurement of these projects are in line with the grace period stated in credit contract and that grace period is agreed upon by commercial bank and borrower on the basis of provisions of applicable laws on provision of loan funds and management of projects on work investment, construction, procurement of fixed assets.

2. Regarding interest rate support to medium, long term loans in Vietnamese Dong, of which value added tax (VAT) belongs to investment projects which are subjects entitled to interest rate support: For loans for procurement of materials, goods belonging to investment projects, of which invoice for materials, goods procurement states amount of VAT, such loans shall be considered as subject entitled to interest rate support in accordance with provisions of applicable laws.

|

|

FOR

THE GOVERNOR OF THE STATE BANK OF VIETNAM |