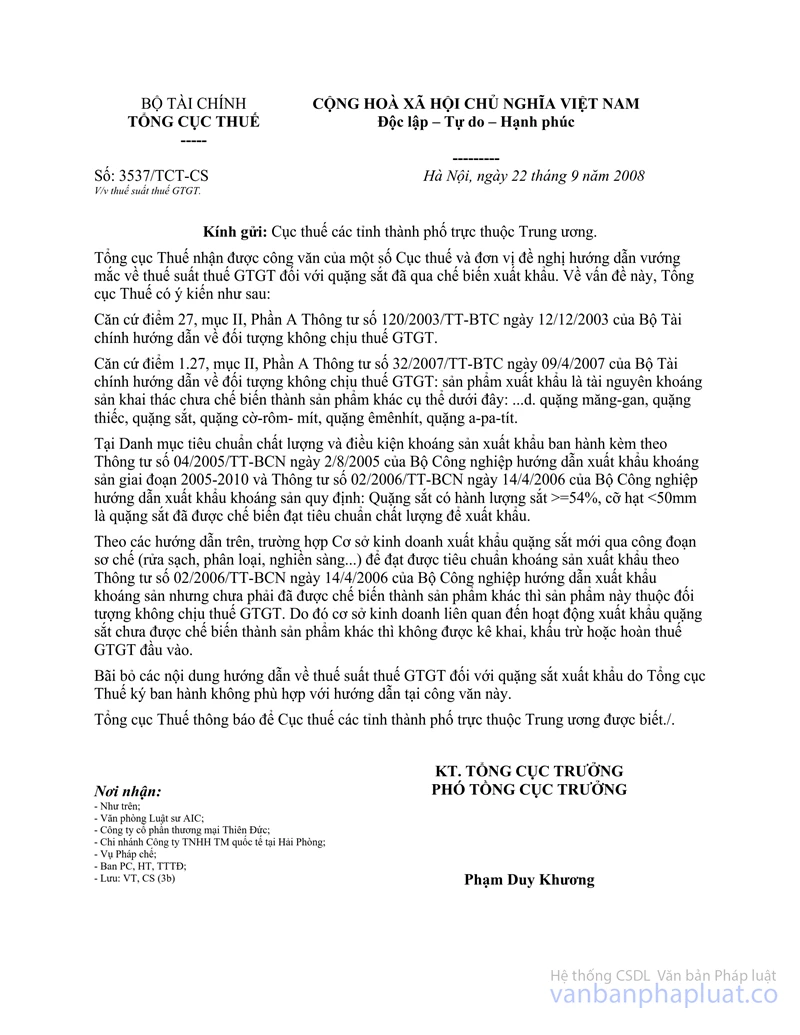

Nội dung toàn văn Official Dispatch No. 3537/TCT-CS, on value-added tax (VAT) rates

|

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 3537/TCT-CS |

Hanoi, September 22, 2008 |

To: Tax Offices of provinces and centrally run cities

The General Department of Taxation has received Official Letters from some Provincial Tax Offices and units, requesting the guidance on solving problems relating to VAT rates of iron ores processed for export. Regarding this issue, the General Department of Taxation gives the following opinions:

Pursuant to Point 27, Section II, Part A of the Ministry of Finance’s Circular No. 120/2003/TT-BTC of December 12, 2003, guiding objects not subject to VAT.

Pursuant to Point 1.27, Section II, Part A of the Ministry of Finance’s Circular No. 32/2007/TT-BTC of April 9, 2007, guiding objects not subject to VAT: exported products that are exploited mineral resources not yet processed into other products, specifically as follows: ....d/ Manganese, tin, iron, chromite, emenite and apatite ores.

The list of quality standards and conditions for export minerals issued together with the Ministry of Industry’s Circular No. 04/2005/TT-BCN of August 2, 2005, guiding the export of minerals during period from 2005 to 2010, and the Ministry of Industry’s Circular No. 02/2006/TT-BCN of April 14, 2006, guiding the export of minerals, stipulate: Iron ores with the iron content of >=54% and the granule size of < 50mm are processed ones that meet quality standards for export.

According to the above guidance, when business enterprises export iron ores, which have undergone the preliminary processing steps (cleaning, sorting, crushing and screening...) in order to meet standards for export minerals under the Ministry of Industry’s Circular No. 02/2006/TT-BCN of April 14, 2006, guiding the export of minerals, but not yet processed into other products, they are not subject to VAT. Therefore, business establishments involved the export of iron ores not yet processed into other products will not be entitled to VAT declaration, input VAT credit and refund.

All provisions guiding VAT rates of export iron ores promulgated by the General Department of Taxation which are not in accordance with the guidance in this Official Letter will be repealed.

The General Department of Taxation gives above guidance to Provincial Tax Offices for information.

|

|

FOR THE DIRECTOR GENERAL OF

TAXATION |