Nội dung toàn văn Official Dispatch No. 3651/TCT-CS, on Invoices for goods for sale promotion

|

MINISTRY

OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No.

3651/TCT-CS |

Hanoi, September 30, 2008 |

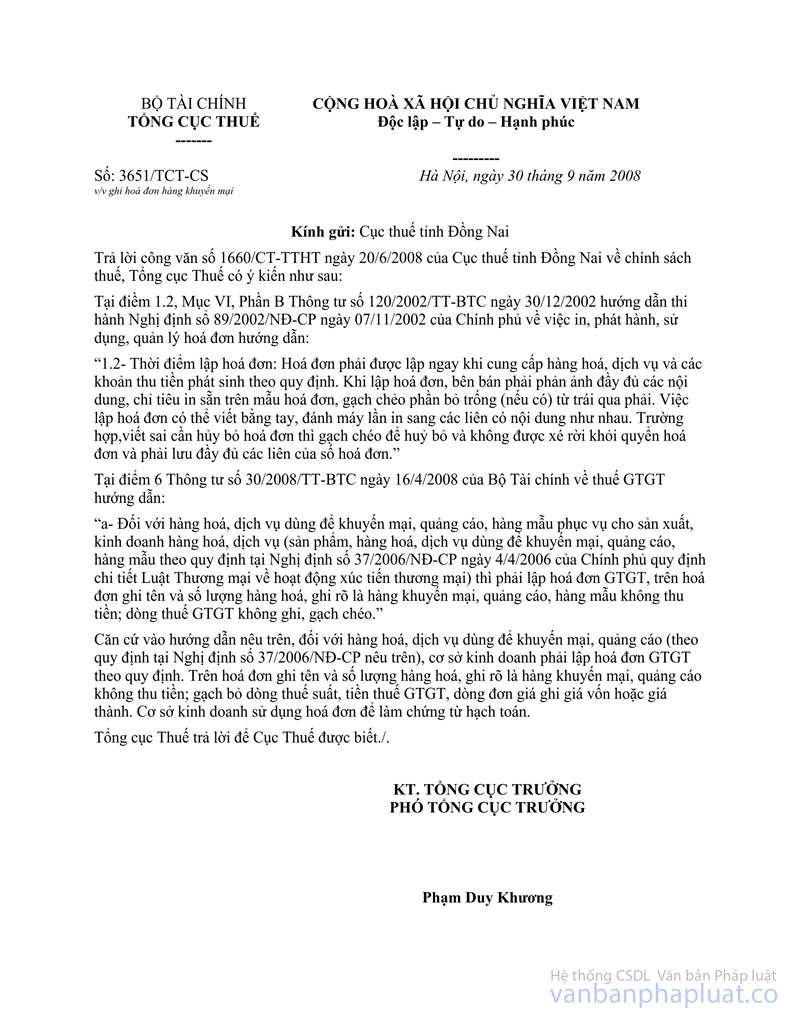

To: Dong Nai Provincial Tax Office

In response to the Official Letter No. 1660/CT-TTHT dated June 20, 2008 of Dong Nai Provincial Tax Office regarding tax policies, the General Department of Taxation gives the following opinions:

Point 1.2, Section VI, Part B of Circular No. 120/2002/TT-BTC of December 30, 2002, guiding the implementation of the Government's Decree No. 89/2002/ND-CP of November 7, 2002, on the printing, issuance, use and management of invoices, guides:

“1.2. Time of issuing invoices: Invoices must be issued according to regulations immediately when goods or services are delivered and receivable amounts arise. When issuing an invoice, a seller shall fully fill in pre-printed contents of the invoice form and cross out blank sections (if any) from left to right. An invoice may be handwritten or typed once with its copies having the same contents. When an invoice is mistakenly filled in and needs to be canceled, it shall be crossed out and may not be torn off from the invoice book and its copies must be fully kept.”

Point 6 of the Ministry of Finance's Circular No. 30/2008/TT-BTC of April 16, 2008, on value-added tax guides:

“a/ For goods and services used for sales promotion, advertisement or as samples serving the production of and trading in goods and services (products, goods and services used for sales promotion, advertisement or as samples are specified in the Government’s Decree No. 37/2006/ND-CP of April 4, 2006, detailing the Commercial Law regarding trade promotion), VAT invoices must be made, stating goods appellations and quantities and that goods are for sales promotion, advertisement or as free samples, with VAT lines left blank and crossed out”.

Under the above guidance, business establishments shall issue according to regulations value-added invoices for goods and services used for sale promotion or advertisement (under Decree No. 37/2006/ND-CP) Invoices must specify goods appellations and quantities, stating that they are for sale promotion or advertisement and free. The tax rate, value-added tax amount and unit cost price or production cost lines must be crossed out. Business establishments may use these invoices in cost accounting.

The General Department of Taxation informs the Tax Office for information.

|

|

FOR

THE DIRECTOR GENERAL OF TAXATION |