Nội dung toàn văn Official Dispatch No. 3859/TCT-CS on foreign contractor tax on overseas brokerag

|

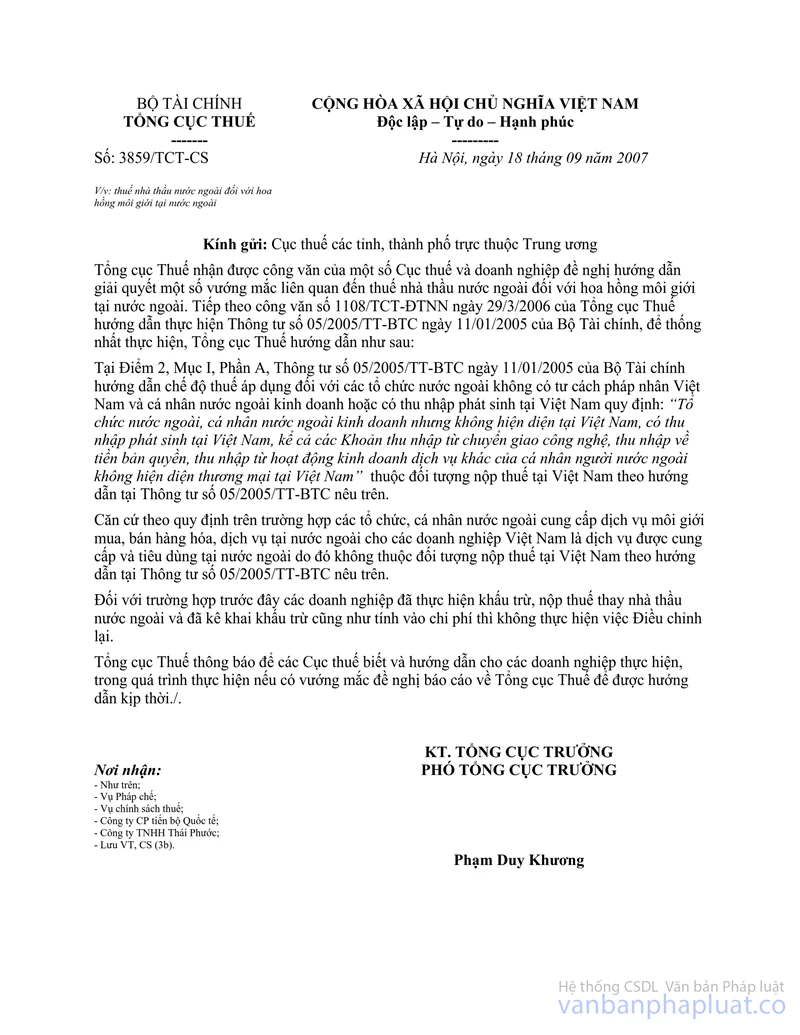

MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 3859/TCT-CS |

Hanoi, September 18, 2007 |

OFFICIAL LETTER

ON FOREIGN CONTRACTOR TAX ON OVERSEAS BROKERAGE COMMISSIONS

To: Provincial/municipal Tax Departments

The General Department of Taxation has received Official Letters of several Tax Departments and enterprises, requesting guidance on handling several problems related to foreign contractor tax on overseas brokerage commissions. Following the General Department of Taxation’s Official Letter No. 1108/TCT-DTNN of March 29, 2006, guiding the implementation of Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005, for uniform application, the General Department of Taxation gives the following guidance:

Point 2, Section I, Part A of the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005, guiding the tax regime applicable to foreign organizations without Vietnamese legal status and foreign individuals doing business or earning incomes in Vietnam stipulates: “Foreign organizations and individuals that do business but are not present in Vietnam, earn incomes in Vietnam, including those from technology transfer, royalties, or other business and service activities earned by foreign individuals without commercial presence in Vietnam” shall be liable to pay taxes under the guidance of Circular No. 05/2005/TT-BTC.

Accordingly, if foreign organizations or individuals provide overseas brokerage services of goods and service sale and purchase for Vietnamese enterprises, which are consumed in foreign countries, they are not liable to pay taxes in Vietnam.

In case enterprises had withheld or paid tax on behalf of foreign contractors and declared and included those tax amounts into their expenses, no adjustment shall be made.

The General Department of Taxation gives this notice to Tax Departments for information and guidance on implementation for enterprises; any problems arising in the course of implementation should be reported to the General Department of Taxation for timely guidance.

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |