Nội dung toàn văn Official Dispatch No. 3929/TCT-CS 2012 regarding tax policy applicable to foreign contractors

|

THE MINISTRY OF

FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 3929/TCT-CS |

Hanoi, November 08, 2012 |

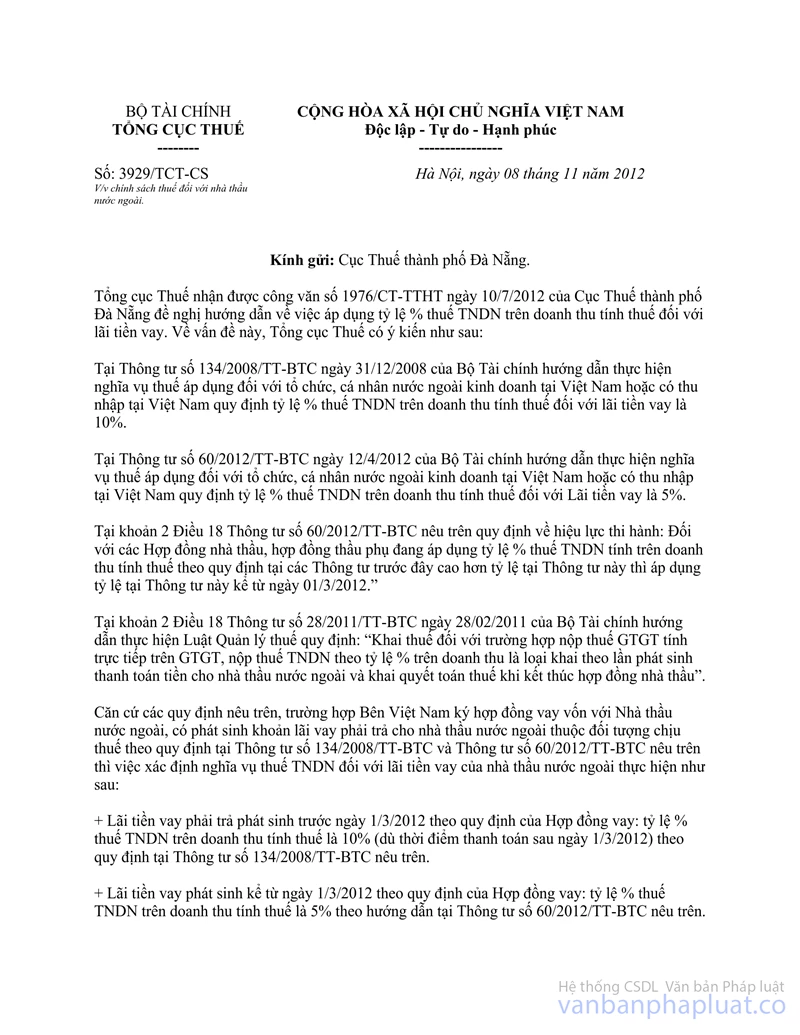

Respectfully to: The Taxation Department of Da Nang city.

The General Department of Taxation has received the official dispatch No.1976/CT-TTHT dated July 10, 2012, of The Taxation Department of Da Nang city suggesting to be guided in application of the EIT rate % on taxable revenues for loan interests. About this issue, the General Department of Taxation has opinion as follows:

At the Circular No. 134/2008/TT-BTC dated December 31, 2008 of the Ministry of Finance, guiding the performance of tax obligations applicable to foreign organizations and individuals doing business or earning incomes in Vietnam, prescribed the EIT rate % on taxable revenues for loan interests being 10%.

At the Circular No. 60/2012/TT-BTC dated April 12, 2012 of the Ministry of Finance, guiding the performance of tax obligations applicable to foreign organizations and individuals doing business or earning incomes in Vietnam, prescribed the EIT rate % on taxable revenues for loan interests being 5%.

At Clause 2 Article 18 of the Circular No. 60/2012/TT-BTC mentioned above, it has prescribed about effect as follows: For contractor agreements, sub-contractor agreements which are applying the EIT rate % based on taxable revenues in accordance with provisions in previous Circulars higher than the rate in this Circular, the rate in this Circular shall apply from March 01, 2012.”

At Clause 2 Article 18 of the Circular No. 28/2011/TT-BTC dated February 28, 2011, of the Ministry of Finance, guiding implementation of Law on tax administration, it prescribed: “Tax declaration in case of payment of VAT calculated directly on the added value and payment of EIT on a percentage of turnover tax shall be declaration for each time of payment to foreign contractors and finalized declaration upon expiration of contractor agreements”.

Based on the provisions mentioned above, in case where a Vietnamese party signs a loan contract with a foreign contractor, which arise a loan interest payable to the foreign contractor under taxable objects as prescribed in Circular No. 134/2008/TT-BTC and Circular No. 60/2012/TT-BTC mentioned above, the determination of EIT obligation for loan interest of the foreign contractor shall execute as follows:

+ The payable loan interests arising before March 01, 2012, as prescribed by the loan contract: The EIT rate % based on taxable revenues shall be 10% (although payment is executed after March 01, 2012) in accordance with Circular No. 134/2008/TT-BTC mentioned above.

+ The loan interests arising from March 01, 2012, as prescribed by the loan contract: The EIT rate % based on taxable revenues shall be 5% in accordance with guide in Circular No. 60/2012/TT-BTC mentioned above.

The General Department of Taxation replies to the Taxation Department of Da Nang City to base on provisions and actually-arising situations, for guiding the units in implementation.

|

|

PP. GENERAL

DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments