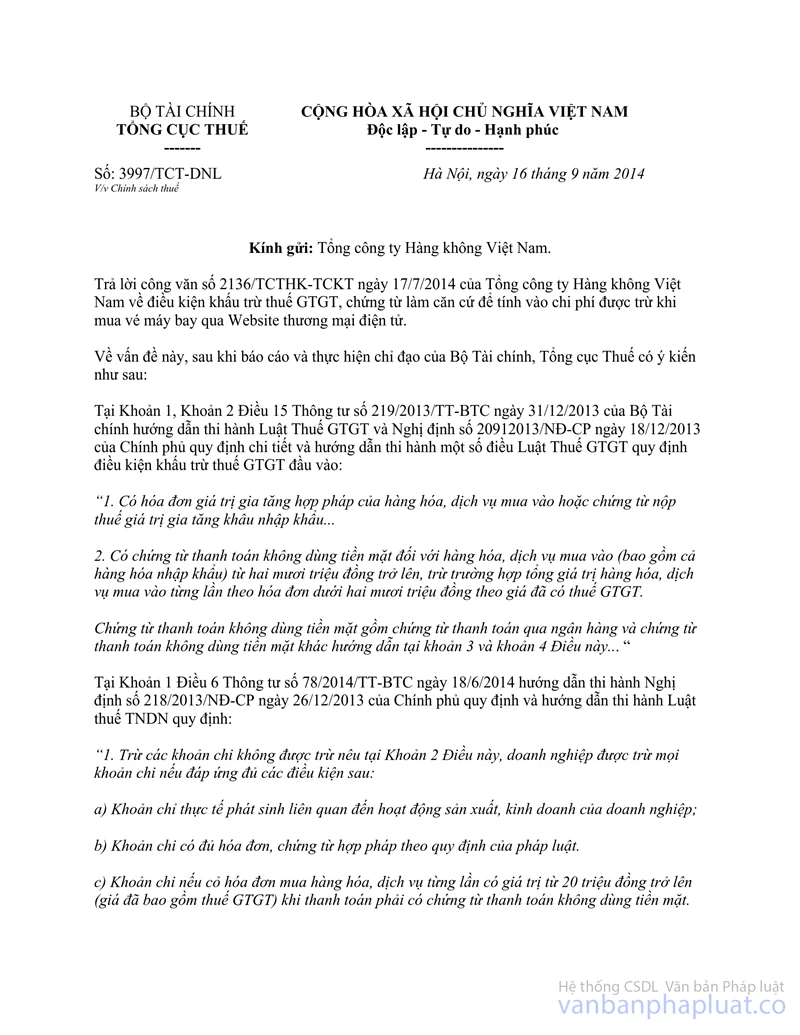

Nội dung toàn văn Official Dispatch No. 3997/TCT-DNL dated 2014 requirements for VAT deductions and documents being the basis

|

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

No.

3997/TCT-DNL |

Hanoi, September 16, 2014 |

To: Vietnam Airlines

In response to Dispatch No. 2136/TCTHK-TCKTdated September 17, 2014 of Vietnam Airlines on requirements for VAT deductions and documents being the basis for including online payments for air tickets to deductible expenses.

After receiving instructions from the Ministry of Finance, the General Department of Taxation hereby responds as follows:

Clause 1 and Clause 2 Article 15 of Circular No. 219/2013/TT-BTC dated December 31, 2013 of the Ministry of Finance on guidelines for the Law on Value-added tax and the Government's Decree No. 20912013/NĐ-CP dated December 18, 2013 on guidelines for the Law on Value-added tax prescribe the requirements for tax deduction as follows:

“1. There are legitimate VAT invoices for purchased goods/services or proof of VAT payment at importation stage...

2. There is proof of non-cash payment for purchased goods/services (including imported goods) that are of VND 20 million or above, except for the case in which the total value of multiple purchases is below VND 20 million (at VAT-inclusive prices).

Proof of non-cash payment includes bank transfer receipt and other proof of non-cash payment prescribed in Clause 3 and Clause 4 of this Article... “

Clause 1 Article 6 of Circular No. 78/2014/TT-BTC dated June 18 on guidelines for the Government's Decree No. 218/2013/NĐ-CP 2014 prescribes:

“1. Except for the non-deductible expenses prescribed in Clause 2 of this Article, all expenses may be deducted if all of the following requirements are satisfied:

a) The expenses incurred are related to the company’s operation;

b) There are legitimate invoices and receipts for the expenses.

c) There is proof of non-cash payment for every purchase that is VND 20 million or above (at VAT-inclusive price).

Proof of non-cash payments must comply with regulations of law on VAT...”

Point 8 Clause 2 Article 6 of Circular 78/2014/TT-BTC prescribes:

(“... Where the company buys air tickets online for its employees to go on business trips serving the company’s operation, the digital air tickets, boarding passes, and proof of non-cash payment shall be the basis for including the air ticket payments in deductible expenses. If the company fails to collect the boarding passes, then the digital air tickets, the dispatch orders, and proof of non-cash payment shall be the basis for including the air ticket payments in deductible expenses.”

Pursuant to the regulations above, in consideration of characteristics of the aviation services, international practice, and for the purpose of enabling companies to use air services flexibly to serve their business operation, General Department of Taxation hereby provides guidance as follows:

Point 8 Clause 2 Article 6 of Circular 78/2014/TT-BTC shall be complied with when the company buys air tickets online for its employees to go on business trips serving the its business operation.

In case the dispatched employees buy and pay for the air tickets themselves using their personal ATM cards, then get reimbursed by the company, the company may deduct input VAT and include the air ticket payments in deductible expenses when calculating corporate income tax if the company has adequate proof that such expenses are meant to serve its business operation, which includes: air tickets, boarding passes (if available), documents related to the dispatches certified by the company, the company’s regulations on permitting employees to pay for business trips using their personal payment cards and the get reimbursed by the company, proof that the employees have been reimbursed for the tickets by the company enclosed with proof of non-cash payment of the dispatched employees The company are responsible for the legitimacy of the aforesaid documents.

This Dispatch replaces Dispatch No. 2272/TCT-KK dated June 18, 201 4 of General Department of Taxation.

Vietnam Airlines is responsible for the implementation of this Dispatch

|

|

PP THE DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed