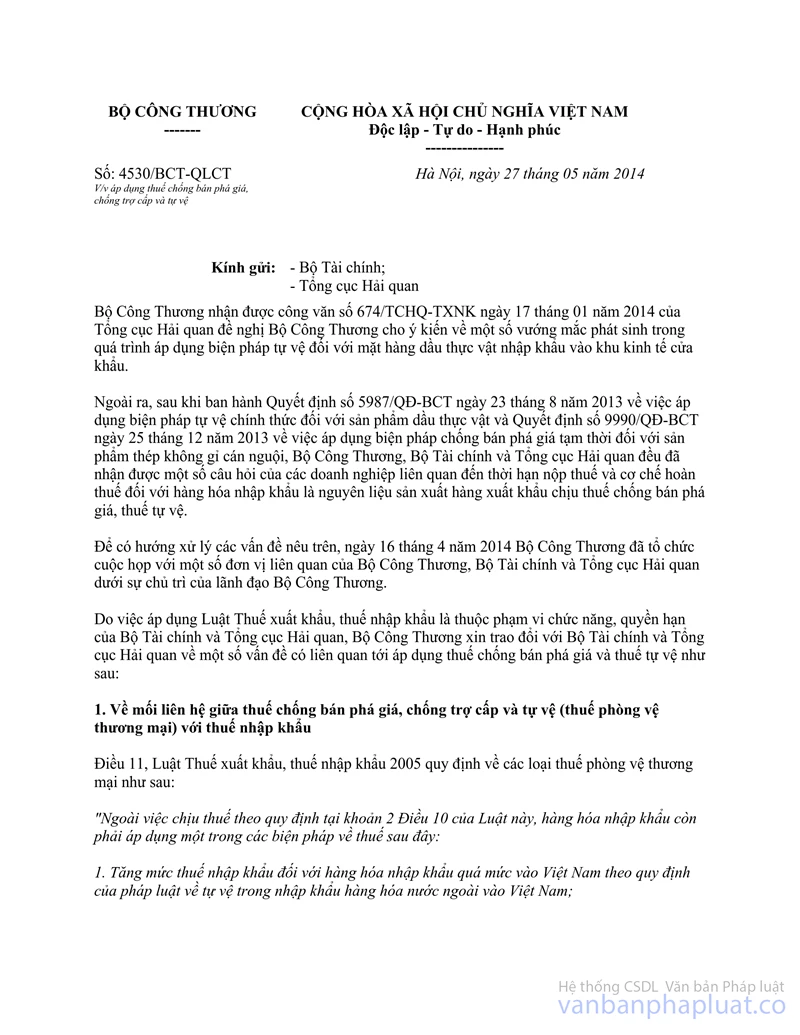

Nội dung toàn văn Official Dispatch No.4530/BCT-QLCT 2014 anti-dumping duty countervailing duty and safeguard duty

|

MINISTRY OF INDUSTRY AND TRADE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No.: 4530/BCT-QLCT |

Hanoi, May 27, 2014 |

|

To: |

- Ministry of Finance; |

The Ministry of Industry and Trade has received the official dispatch No. 674/TCHQ-TXNK dated January 17, 2014 of the General Department of Customs requesting the Ministry of Industry and Trade to give opinions about a number of problems arising during the application of safeguard measures against the vegetable oil product imported into border gate economic zones.

In addition, after having issued Decision No. 5987/QD-BCT dated August 23, 2013 on application of official safeguard measures against the vegetable oil product and Decision No. 9990/QD-BCT dated December 25, 2013 on application temporary anti-dumping measures against the cold-rolled stainless steel product, the Ministry of Industry and Trade, Ministry of Finance and General Department of Customs have received a number of questions of enterprises related to the tax payment deadline and tax refund mechanisms for imported goods as raw materials for the production of exported goods subject to anti-dumping duty and safeguard duty.

For settling the above problems, on April 16, 2014, the Ministry of Industry and Trade held a meeting with a number of units concerned of the Ministry of Industry and Trade, the Ministry of Finance and the General Department of Customs under the chairmanship of leaders of Ministry of Trade and Industry.

Because the application of Law on Export and Import Tax is under the scope of functions and power of the Ministry of Finance and the General Department of Customs, the Ministry of Industry and Trade would like to exchange opinions with the Ministry of Finance and the General Department of Customs about a number of issues related to the application of anti-dumping duty and safeguard duty as follows:

1. About the relationship between the anti-dumping duty, countervailing duty and safeguard duty (commercial safeguard duty) with the import tax

Article 11. The Law on Export and Import Tax 2005 stipulates the types of commercial safeguard duty as follows:

“In addition to being subject to tax as stipulated in Clause 2, Article 10 of this Law, the imported goods shall be imposed one of the measures of tax as follows:

1. Increase in import tax against excessively imported goods into Vietnam under regulations of law on safeguard in importing foreign goods into Vietnam;

2. The anti-dumping duty against dumped goods that are imported into Vietnam under regulations of law on prevention of dumping of goods imported into Vietnam;

3. Countervailing duty against the subsidized goods that are imported into Vietnam under regulations of law on prevention of subsidy of goods imported into Vietnam;…”

Therefore, according to the Law on Export and Import Tax 2005, the application of types of commercial safeguard duty shall be implemented as stipulated by regulations of law on safeguard, prevention of dumping and subsidy. Meanwhile, the law on safeguard, prevention of dumping and subsidy is regulated as follows:

- Clause 1, Article 3 of Ordinance No. 42/2002/PL-UBTVQH10 on safeguard measures stipulates that:

“The safeguard measures in importing foreign goods into Vietnam include: 1. Increase in import tax; 2. Application of quota of import; 3. Application of other measures stipulated by the Government”.

According to this regulation, if the safeguard measures are implemented in the form of tax, it is the import tax (increase in import tax);

- Clause 1, Article 2 of Ordinance No. 20/2004/PL-UBTVQH11 on measures to prevent the dumping and Clause 3, Article 2 of Ordinance No. 22/2004/PL-UBTVQH11 on the measures to prevent the subsidy stipulate that:

“Anti-dumping duty is the additional import tax which is applied in case where the dumped goods are imported into Vietnam causing or threatening to cause remarkable damages to the domestic production industry”.

“Countervailing duty is the additional import tax which is applied in case where the subsidized goods are imported into Vietnam causing or threatening to cause remarkable damages to the domestic production industry”.

According to these regulations, the anti-dumping duty and the countervailing duty are also the import tax and supplement the current import tax.

2. Direction to settle the problems arising in application of commercial safeguard duty

The regulations of law mentioned above demonstrate that the anti-dumping duty, countervailing duty and safeguard duty are regarded as import tax (addition or increase). Therefore, in the view of the Ministry of Industry and Trade, the application of these duties in some relevant cases (such as goods imported into border gate economic zone, imported from foreign countries into the non-tariff area of the border gate economic zone and only used in the non-tariff area, the goods carried from one non-tariff area to another non-tariff area, the goods as raw materials for production of exported goods v,v ) needs implementing as the import tax as stipulated by the Law on Export and Import Tax;

Above is the opinions of the Ministry of Industry and Trade on the way to settle a number of problems arising in application of commercial safeguard duty. We hereby request the Ministry of Finance and the General Department of Customs to consider and make a decision under the authority

|

|

PP. MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed