Nội dung toàn văn Official Dispatch No. 735/TCT/DNNN on tax policy towards insurance agents

|

THE

FINANCE MINISTRY |

SOCIALIST

REPUBLIC OF VIET NAM |

|

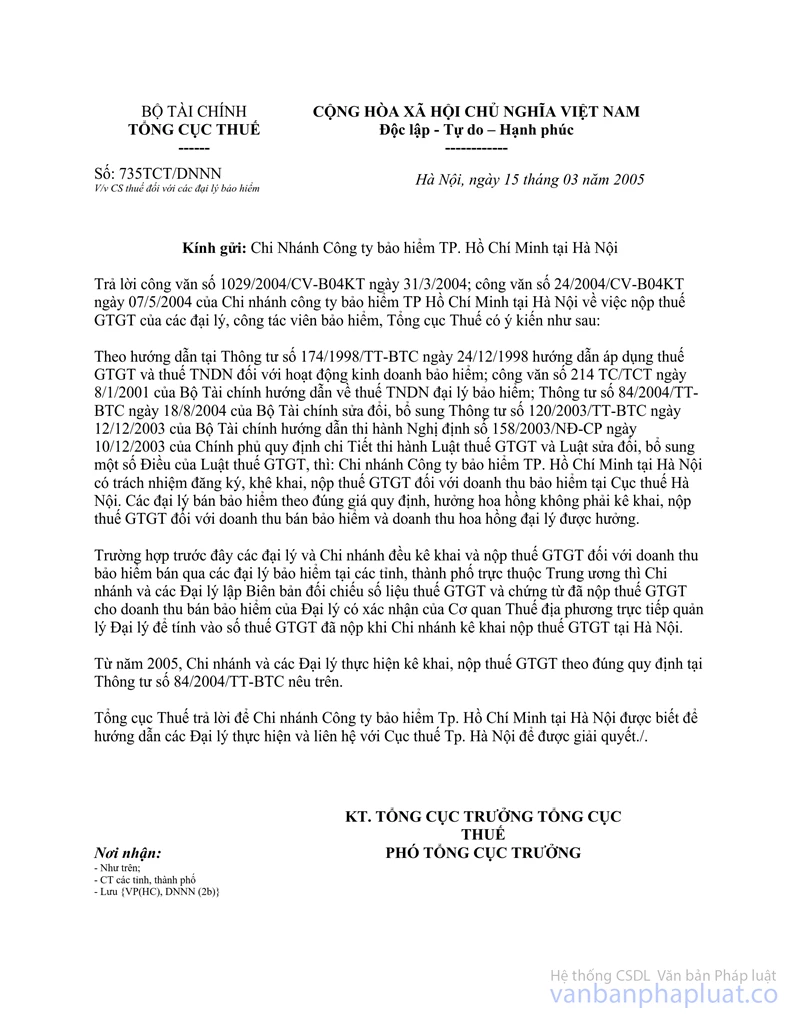

No. 735 TCT/DNNN |

Hanoi, March 15, 2005 |

OFFICIAL LETTER

ON TAX POLICY TOWARDS INSURANCE AGENTS

To: The Hanoi branch of Ho Chi Minh City Insurance Company

In reply to Official Letter No. 1029/2004/CV-B04KT of March 31, 2004, and Official Letter No. 1724/2004/CV-B04KT of May 7, 2004, of the Hanoi branch of Ho Chi Minh City Insurance Company, on the payment of value added tax (VAT) by insurance agents and collaborators, the General Department of Taxation gives the following opinion:

According to the Finance Ministry's Circular No. 174/1998/TT-BTC of December 24, 1998, guiding the application of VAT and Business Income Tax (BIT) to insurance business activities; Official Letter No. 214 TC/TCT of January 8, 2001, guiding BIT for insurance agents; and Circular No. 84/2004/TT-BTC of August 18, 2004, amending Circular No. 120/2003/TT-BTC of December 12, 2003, which guides the implementation of the Government's Decree No. 158/2003/ND-CP of December 10, 2003, detailing the implementation of the VAT Law and the Law Amending a Number of Articles of the VAT Law, the Hanoi branch of Ho Chi Minh City Insurance Company shall register, declare and pay VAT on insurance turnover at the Hanoi Tax Department. Agents that sell insurance at fixed rates for commissions shall not have to declare and pay VAT on insurance sale turnover and agency commission turnover they earn.

Where agents and the branch already declared and paid VAT on turnover arisen from insurance sold by insurance agents in provinces or centrally run cities, the branch and agents shall make records on comparison of VAT data with vouchers on VAT paid on agents' insurance sale turnover, with certification of local tax offices directly managing the agents, for inclusion in the paid VAT amounts when the branch makes VAT declaration and payment in Hanoi.

As from 2005, the branch and agents shall make VAT declaration and payment strictly according to the provisions of the above-said Circular No. 84/2004/TT-BTC.

The General Department of Taxation hereby gives the above-said opinion to the Hanoi branch of Ho Chi Minh City Insurance Company for providing guidance to its agents for implementation and contact with the Tax Department of Hanoi city for settlement.

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |