Nội dung toàn văn Official Dispatch No.755/TCT-KK 2015 Time limit for application for tax registration

|

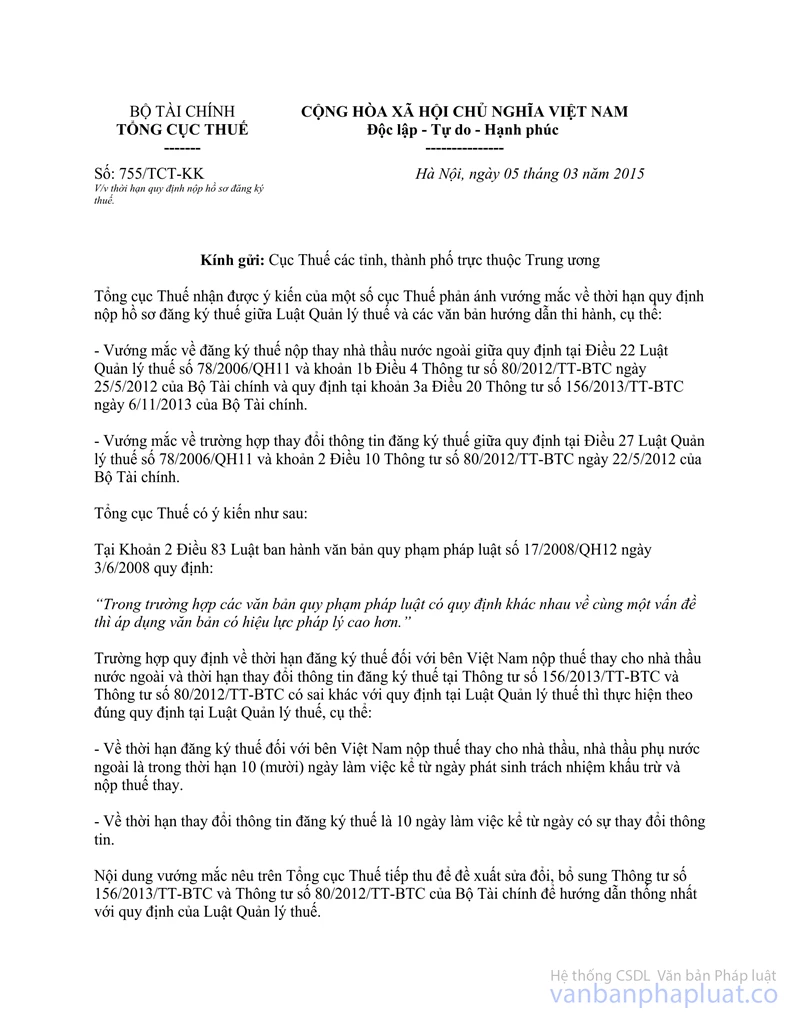

THE MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No.: 755/TCT-KK |

Hanoi, March 05, 2015 |

Respectfully addressed to: Department of Taxation of central-affiliated cities and provinces

General Department of Taxation has received opinions from some departments of taxation regarding time limit for application for tax registration between the Law on Tax Administration and guiding documents, specifically:

- Difficulties in application for tax registration on behalf of foreign contractors between the provisions set out in Article 22 of the Law on Tax Administration No. 78/2006/QH11 and Clause 1b, Article 4 of the Circular No. 80/2012/TT-BTC dated May 25, 2012 of the Ministry of Finance and the provisions set out in Clause 31, Article 20 of the Circular No. 156/2013/TT-BTC dated November 6, 2013 of the Ministry of Finance.

- Difficulties in changing tax registration information between the provisions set out in Article 27 of the Law on Tax Administration No. 78/2006/QH11 and Clause 2, Article 10 of the Circular No. 80/2012/TT-BTC dated May 25, 2012 of the Ministry of Finance.

General Department of Taxation has come up with the following opinions:

Clause 2, Article 38 of the Law on Promulgation of legislative documents No. 17/2008/QH12 dated June 03, 2008 regulates:

“In case legislative documents have different provisions on the same issue, a document issued by the superior authority shall prevail."

In case the time limit for application for tax registration made by Vietnamese side on behalf of foreign contractors and the time limit for making changes to tax registration information as prescribed in the Circular No. 156/2013/TT-BTC and the Circular No. 80/2012/TT-BTC deviate from the provisions set out in the Law on Tax Administration, the provisions set out in the Law on Tax Administration shall be applied, specifically:

- Time limit for application for tax registration made by Vietnamese party on behalf of foreign contractors, sub-contractors shall be 10 working days since liabilities for deduction and tax payment arise.

- Time limit for changing tax registration information shall be 10 working days since the occurrence of such change.

General Department of Taxation shall be open to the abovementioned difficulties and propose amendments and supplements to the Circular No. 156/2013/ TT-BTC and Circular No. 80/2012/TT-BTC of the Ministry of Finance to be in agreement with the Law on Tax Administration.

General Department of Taxation shall make notification to departments of taxation for providing guidance to tax payers./.

|

|

PP DIRECTOR GENERAL |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed