Nội dung toàn văn Official Dispatch No. 767/TCT-CS 2015 new contents of Circular No. 26/2015/TT-BTC

|

MINISTRY

OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

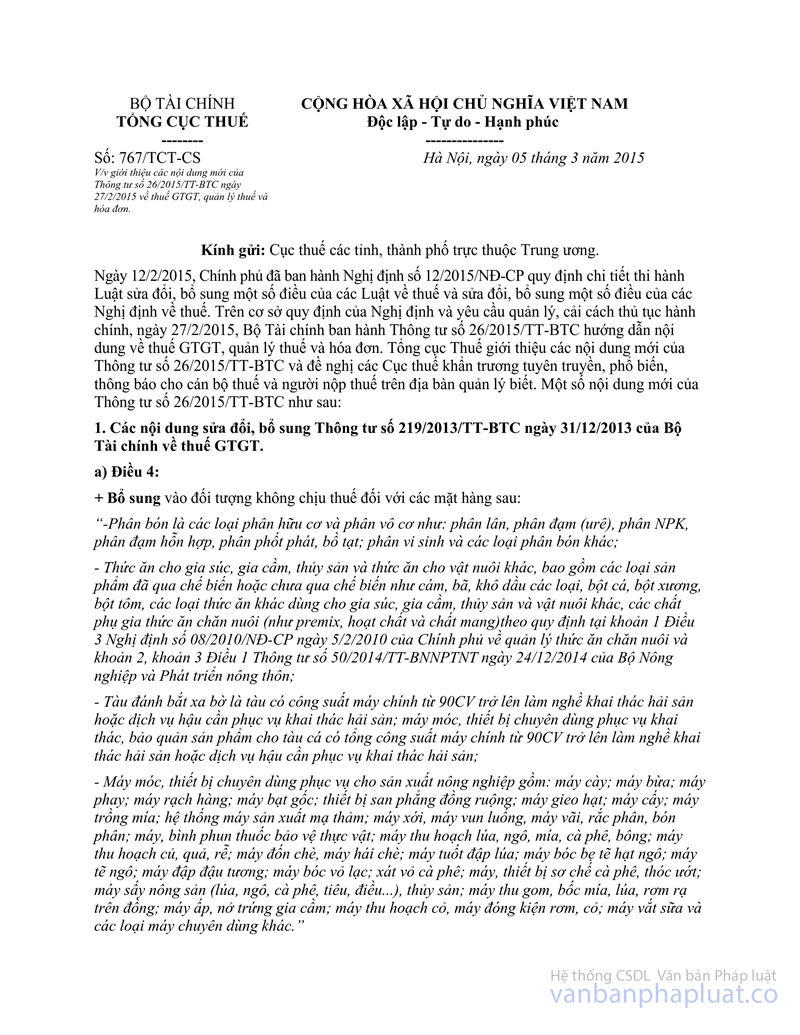

No. 767/TCT-CS |

Hanoi, March 05, 2015 |

To: Provincial Departments of Taxation

On February 12, 2015, the Government promulgated Decree No. 12/2015/NĐ-CP on guidelines for the Law on Amendments to tax laws and decrees on taxation. According to the Decree, in consideration of the needs for management and administrative reform, on February 27, 2015, the Ministry of Finance promulgated Circular No. 26/2015/TT-BTC on guidelines for VAT, tax administration, and invoices. General Department of Taxation hereby introduces some new contents of Circular No. 26/2015/TT-BTC and requests that Provincial Departments of Taxation disseminate such contents among tax officials and taxpayers. Some new contents of Circular No. 26/2015/TT-BTC:

1. Amendments to Circular No. 219/2013/TT-BTC dated December 31, 2013 of the Ministry of Finance on VAT

a) Article 4:

+ Addition: commodities not subject to tax:

"- Fertilizers are organic and inorganic fertilizers such as phosphate fertilizers, nitrogenous fertilizer (urea), NPK fertilizer, mixed urea, potash; biofertilizers and other fertilizers;

- Feeds for livestock, poultry, fish, and other animals (hereinafter referred to as animal feeds), including processed or unprocessed products such as mash, dregs, oil cakes, fish meal, bone meal, shrimp meal, and other types of animal feeds, animal feed additives (such as premix, active ingredients, and carriers) prescribed in Clause 1 Article 3 of the Government's Decree No. 08/2010/NĐ-CP dated February 05, 2010 on management of animal feeds, Clause 2 and Clause 3 Article 1 of Circular No. 50/2014/TT-BNNPTNT dated December 24, 2014 of the Ministry of Agriculture and Rural Development;

- Offshore fishing ships are ships ≥ 90CV and engaged in fishing or logistics services serving fishing; machinery and specialized equipment serving extraction and preservation of products on fishing ships ≥ 90CV engaged in fishing or logistics services serving fishing;

- Machinery and specialized equipment serving agricultural production, including: tractor; harrowing machine; milling machine; sowing machine; rootdozer; field leveling device; seeding machine; transplanter; sugarcane planting machine; rice-sowing machine; tiller, cultipacker, fertilizer spreader, pesticide sprayers; machine for harvesting rice, corn, sugarcane, coffee, cotton; machine for harvesting tubers, fruits, roots; tea-cutting machine, tea-picking machines; threshing machine; corn peeling machine; soybean crusher; peanut huller; coffee huller, equipment for preparing coffee, wet rice; dryer for agricultural products (rice, corn, coffee, pepper, cashew nut...), and aquaculture products; machine for collecting, loading sugarcane, straw on the field; machine for egg incubating and hatching ; forage harvester; straw, grass baler; milking machine, and other specialized machines."

Old document: 5% and 10% tax (on offshore fishing ships).

+ Addition: Cases in which borrowers are not required to issue VAT invoices when transferring collateral to the bank.

There were no instructions in the old document.

b) Article 7: Addition of Point a.8 and Point a.9 to Clause 10 on taxable prices of real estate transfer, particularly:

“a.8) When a taxpayer receives land use right from another entity, deductible land price when calculating VAT is the price written on the capital contribution contract. If the price for transfer of land use right is lower then the price of contributed land, the former shall apply.

a.9) Where a real estate company signs a contract with a household or individual who have a piece of agricultural land to convert it into housing land and such conversion is conformable with regulations of law on land, taxable price shall equal transfer price minus (-) deductible land price. Transfer price is the price for compensation corresponding to the area of agricultural land that is withdrawn under a plan approved by a competent authority."

There were no specific instructions in the old document.

c) Article 9: Added instructions: Guidance on application of 0% tax on tobacco, alcohol, beer that are imported then exported.

Tobacco, alcohol, and beer that are imported then exported shall not incur output VAT upon export. However, input VAT shall not be deducted.

d) Article 10: Application of 5% tax on supplies and chemicals for medical testing and sterilization "as certified by the Ministry of Health."

There were no specific instructions in the old document.

dd) Article 14:

+ Addition: Revenues on which VAT is not required to be accounted for when determining deductible input VAT, particularly:

"… The taxpayer must separate the deductible input VAT from non-deductible one. Otherwise, input VAT shall be deducted according to the ratio of revenue subject to VAT, revenue not subject to VAT to the total revenue from selling goods and services, including revenue not subject to VAT that cannot be separated."

+ Addition: Guidance on deduction of VAT on goods that are no longer subject to VAT:

"14a. Input VAT on goods, services, fixed assets serving manufacture of: fertilizers, specialized machinery and equipment serving agricultural production, offshore fishing ships, animal feeds that are sold domestically shall be included in deductible expenses when determining income subject to corporate income tax instead of being declared and deducted, except for VAT on purchased of goods, services, fixed assets that are incurred before January 01, 2015, written on VAT invoices or proof of VAT payment upon importation and satisfy conditions for deduction, tax refund, and are eligible for tax refund as prescribed in Article 18 of Circular No. 219/2013/TT-BTC dated December 31, 2013 and this Circular."

e) Article 15:

+ Addition: Cases in which proofs of non-cash payments for imports being gifts, donations from overseas entities are not required.

There were no specific instructions in the old document.

+ Addition: guidance on determination of supplier:

"In case the taxpayer has financially dependent stores that use the same TIN and invoice form, if the invoice shall have the text "Cửa hàng số:" ("Store No.") to differentiate the taxpayer's stores and bears the seal of each store, then each store shall be considered a supplier."

g) Article 16: Addition: Cases in which the foreign partner send money to a current account to pay a Vietnamese business establishment:

“b.7) …

When checking the deduction and refund of tax on exported goods that are paid for via the bank account, the tax authority must cooperate with the credit institution where the account is opened to ensure that the payment and transfer is made properly and in accordance with law. Any person who brings money across the border upon entry must declare that such money is for making payment for each particular sale contract and export declaration, and present the sale contracts and export declaration for customs officials to check and compare. In case the entering person is not a representative of the foreign company that directly signs the sale contract with the Vietnamese company, it is required to have a power of attorney (in English or translated into Vietnam together with the original version in the language of an adjacent country) made by the foreign entity that signs such sale contract. This power of attorney is only warrants one time of bringing money into Vietnam and the amount of money under the sale contract must be specified thereon."

h) Article 18:

+ Specific guidance on refund of VAT incurred by an operative business establishment having multiple projects of investment in the same province.

+ Specific guidance on determination of input VAT of exported goods/services eligible for VAT refund when a business establishment has both exported goods/services and goods/services sold domestically.

+ Addition: Delay in adjustment of VAT that was declared, deducted, or refunded in case a business establishment that has not been in operation is dissolved and has not incurred output VAT on the primary business, particularly:

"5. …If the business establishment that has not been in operation is dissolved and does not incur output VAT on the primary business according to the project of investment, such business establishment is not required to immediately adjust the VAT that was declared, deducted, or refunded. The business establishment must notify the supervisory tax authority of its dissolution, bankruptcy, or shutdown as prescribed.

After completing legal procedures for dissolution or bankrupt, refundable VAT shall be settled in accordance with regulations of law on dissolution, bankruptcy, and tax administration; unrefundable VAT shall not be refunded.

Where a business establishment is shut down and does not incur output VAT on the primary business, refunded VAT must be returned to state budget. If assets subject to VAT are sold, it is not required to adjust input VAT on the sold assets."

2. Amendments to Circular No. 156/2013/TT-BTC dated November 06, 2013 on tax administration.

a) Article 11:

+ Guidance on tax payment in case of extraprovincial construction, installation, or sale with the value of VND 1 billion or higher.

In the old document, there were no specific instructions on determination of value of extraprovincial construction, installation, or sale for the purpose of tax declaration in the province.

+ Addition: Guidance on tax payment by taxpayers having constructions that involve multiple provinces:

“e) Where the taxpayer has an extraprovincial construction project that relates to multiple localities such as roads, power line, water, oil, gas pipeline, etc. and thus is not able to determine the revenue earned from each province, the taxpayer shall include declaration of VAT on revenue from the extraprovincial construction in the VAT declaration at the headquarter and pay VAT in the provinces where the construction is project. VAT payable in the provinces is determined according to the ratio of investment in the project in each province, which is calculated by the taxpayer, multiplied by (x) 2% of revenue from the construction of the project (exclusive of VAT).

Paid VAT (according to tax payment receipts) on interprovincial construction shall be deducted from the tax payable on the VAT declaration (form No. 01/GTGT) submitted by the taxpayer at the headquarters’ locality.

The taxpayer shall make a Table of VAT distribution among the provinces where the project is present (form No. 01-7/GTGT enclosed herewith) and submit it together with the VAT declaration to the Provincial Department of Taxation to which tax is paid.”

+ The list of purchased and sold goods/services is removed from the declaration of VAT and special excise tax.

b) Article 27: Guidance on tax payment currencies; determination of revenues, expenditures, taxable prices, and amounts payable to state budget, particularly:

“...

2. If the taxpayer is required to pay tax in foreign currency but a competent authority allows payment in VND, the taxpayer and tax authority shall exchange the amounts payable into foreign currency according to the amount in VND on the receipt for payment to state budget and the exchange rates prescribed in this Clause, particularly:

If money is paid at a commercial bank, credit institution, or State Treasury, the buying rate announced by the commercial bank or credit institution where the taxpayer’s account is opened at the payment time shall apply.

Example: Company X has to pay some amounts in foreign currency and is permitted by a competent authority to pay in VND. Company X opens accounts at 3 banks which are Bank A, Bank B, and Bank C. On March 21, 2015, buying rate of USD is 21,300 VND/USD at Bank A; 21,310 VND/USD at Bank B; 21,305 VND/USD at bank C. On March 21, 2015, company X pays tax in VND at credit institution D or State Treasury in district E, company X may apply the buying rate of either Bank A, Bank B, or Bank C. If company X pays tax in VND at Bank A, the rate of 21,300 VND/USD shall apply.

3. If there are revenues, expenditures, taxable prices in foreign currencies, they must be converted into VND at the practical exchange rates according to instructions of the Ministry of Finance in Circular No. 200/2014/TT-BTC dated December 22, 2014 on corporate accounting practice:

- The practical exchange rate for revenue statement is the buying rate announced by the commercial bank where the taxpayer’s account is opened.

- The practical exchange rate for revenue statement is the buying rate announced by the commercial bank where the taxpayer’s account is opened when the payment is made.

- Instructions of the Ministry of Finance in Circular No. 200/2014/TT-BTC shall apply to other particular cases.”

c) Regulations on tax deferral in case the taxpayer has not received payment for fundamental construction written in the state budget estimate.

d) Rate of late payment interest:

- From January 01, 2015, late payment interest is charged at 0.05% per day on the amount of tax paid behind schedule.

- If the taxpayer’s insufficient tax declared before January 01, 2015 is found by the tax authority after January 01, 2015 during inspection or by the taxpayer, late payment interest shall be charged at 0.05% per day on the deficit of tax payable for the deferral period.

dd) Cases in which late payment interest is exempt

In case a taxpayer supplies goods/services paid by state budget but has not been paid the state budget user and thus fails to pay tax on time, such taxpayer is not required to pay late payment interest.

e) Determination of late payment interest exempt

- The late payment interest on tax debt at the time of occurrence of natural disaster, conflagration, accident, or epidemic shall be exempt. Nevertheless, the amount of exempted interest must not exceed the value of property or assets being damaged.

- Application for exemption of late payment interest: In case of a natural disaster, conflagration, accident, or epidemic, the application must be enclosed with a damage assessment report issued by a competent authority such as Valuation Council established by the Service of Finance or a valuation organization that provide valuation services under contracts, or Valuation Center of the Service of Finance.

- Procedures for processing an application for exemption of late payment interest: Within 60 days from the occurrence date of the natural disaster, conflagration, accident, epidemic, fatal disease, or another force majeure event, the taxpayer shall make and submit an application for exemption of late payment interest to the supervisory tax authority.

g) Documents about application of Double Taxation Agreement to foreign transport companies

g.1) The following contents are amended:

- Instead of being declared quarterly as prescribed in the old document, tax incurred by foreign transport companies shall be provisionally paid every quarter and finalized every year.

- Regulations on documents proving the operations of foreign transport companies (ship operation documents, cargo/passenger transport contracts, and bills of lading) are annulled.

The said old regulations are replaced with the following:

Such documents must be kept by the agent or representative office in Vietnam of the foreign transport company in accordance with the Law on Accounting, Decrees providing guidelines for the Law on Accounting, and Maritime Code, and shall be presented to the tax authority on request.

If the foreign transport company has multiple agents in different provinces of Vietnam, or the agent has multiple branches or representative offices in different provinces of Vietnam, the foreign transport company or its agent shall submit the original (or certified true copy) of the Certificate of residence that has been consularly legalized to the Department of Taxation of the province where the agent of the foreign transport company is situated, and photocopies of such document to the Departments of Taxation of the provinces where the branches are situated, specifying the place where the original is submitted. The foreign transport company or its agent is not required to submit the tax registration certificate (or Certificate of Business registration) to the tax authority.

g.2) Changes to application for tax refund: The application for tax refund according to International Agreements shall not include the tax payment receipt.

The application for tax refund made by a foreign transport company shall not include documents proving the ship operation, tax payment receipts, and certifications of Vietnamese entities who sign contracts about the practical time and execution of the contracts.

g.3) Addition: With regard to applications for tax refund according to Double Taxation Agreements submitted by foreign transport companies that are eligible for tax refund before inspection, the inspection must be carried out within 01 year from the day on which the decision to refund tax is issued:

3. Amendments to Circular No. 39/2014/TT-BTC dated March 31, 2014 on invoices for goods sales and service provision.

a) Article 4: Business establishments are no longer required to register the use of hyphen and Vietnamese text without diacritics on invoice.

According to the old document, a registration with the tax authority is required.

b) Article 6 and Article 8: Addition: Within 05 working days, if the supervisory tax authority does not make a written response, the self-printed invoices may be used.

c) Article 9: The quantity of invoices that may be published and used for 3 - 6 months in the notice of invoice publication of the enterprise is no longer determined by the supervisory tax authority.

According to the old document, the quantity of invoices that may be published and used for 3 - 6 months in the notice of invoice publication of the enterprise is determined by the supervisory tax authority.

d) Article 14. Added instructions: Connection of taxpayers engaged in hotel and restaurant business, supermarket business, and other business lines using cash register systems and shopkeeper software to receive payments with tax authorities to send information to tax authority according to their plans

There were not instructions in the old document.

dd) Article 16 and Appendix 4: Specific instructions on cases in which invoices for goods meant for internal use for proceeding business operation are not issued.

There were not instructions in the old document

e) Article 16: Added instructions: If the buyer’s name or address on an issued invoice is incorrect but the buyer’s TIN is correct, only an adjustment note is required instead of an adjusted invoice. Instructions of the Ministry of Finance in Article 20 of Circular No. 39/2014/TT-BTC shall apply to other cases of incorrect invoices.”

4. Effect

a) The aforementioned contents come into force from effective date of the Law No. 71/2014/QH13 on amendments to tax laws and the Government's Decree No. 12/2015/NĐ-CP on guidelines for the Law on Amendments to tax laws and decrees on taxation.

b) Notes:

- Clause 2 Article 1 of Circular No. 26/2015/TT-BTC shall apply to the contracts to buy agriculture machinery signed before the effective date of the Law No. 71/2014/QH13 (those mentioned in Clause 11 Article 10 of Circular No. 219/2013/TT-BTC which is amended in Clause 2 Article 1 of this Circular) under which the right to ownership, right to enjoyment are transferred after the effective date of the Law no. 71/2014/QH13.

- With regard to contracts to build offshore fishing ships signed before January 01, 2015 at VAT-inclusive prices, if the ships are not done and transferred by January 01, 2015, Clause 2 Article 1 of this Circular shall apply to the total value of such ships as instructed in Clause 2 Article 1 of Circular No. 26/2015/TT-BTC.

- For the purpose of simplifying tax formalities, regulations on List of invoices, receipts for purchases and sales, and regulations on exchange rates applied when determining revenues and calculating taxes in the following documents shall be annulled:

+ Circular No. 05/2012/TT-BTC dated January 05, 2012 of the Ministry of Finance, which provides guidelines for the Government's Decree No. 26/2009/NĐ-CP dated March 16, 2009 and Decree No. 113/2011/NĐ-CP dated December 08, 2011 on elaboration of the Law on special excise duty.

+ Circular No. 219/2013/TT-BTC dated December 31, 2013 of the Ministry of Finance on guidelines for the Law on Value-added tax and the Government's Decree No. 209/2013/NĐ-CP dated December 18, 2013 on guidelines for the Law on Value-added tax.

+ Circular No. 156/2013/TT-BTC dated November 06, 2013 of the Ministry of Finance on guidelines for the Law on Tax administration; the Law on Amendments to the Law on Tax administration, and the Government's Decree No. 83/2013/NĐ-CP dated July 22, 2013.

+ Circular No. 119/2014/TT-BTC dated August 25, 2014 of the Ministry of Finance on amendments to Circular No. 156/2013/TT-BTC dated November 06, 2013; Circular No. 111/2013/TT-BTC dated August 15, 2013; Circular No. 219/2013/TT-BTC dated December 31, 2013; Circular No. 08/2013/TT-BTC dated January 10, 2013; Circular No. 39/2014/TT-BTC dated March 31, 2014; and Circular No. 78/2014/TT-BTC dated June 18, 2014.

- Notices of tax exemption or reduction according to International Agreements submitted to tax authorities before this Circular takes effect shall be retained together with relevant documents in accordance with this Circular No. 26/2015/TT-BTC by agents or representative offices in Vietnam of foreign transport companies.

Provincial Departments of Taxation are recommended to report any difficulties that arise during the implementation of this Circular to the Ministry of Finance for consideration./.

|

|

PP DIRECTOR |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed