Nội dung toàn văn Official Dispatch No. 767/TCT-CS on tax policies applicable to transfer

|

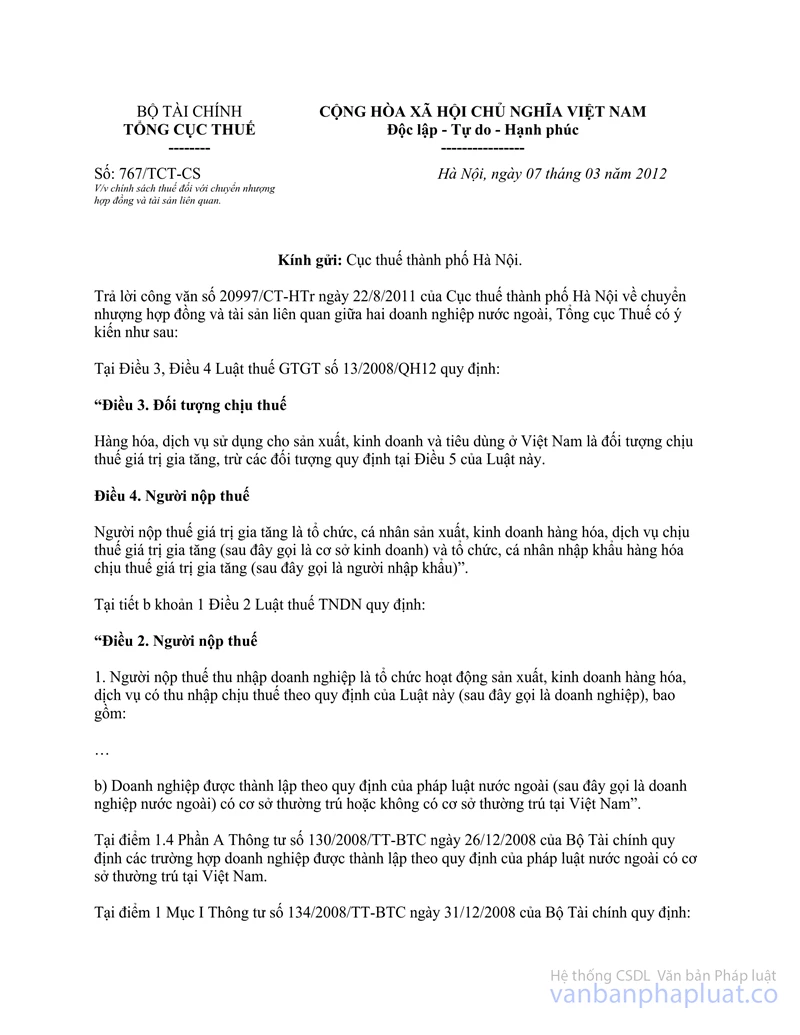

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 767/TCT-CS |

Ha Noi, March 7, 2012 |

To: Hanoi Tax Department

In response to Hanoi Tax Department’s Official Letter No. 20997/CT-HTr of August 22, 2011, on transfer of contracts and related assets between two foreign businesses, the General Department of Taxation gives the following opinions:

Articles 3 and 4 of Law No. 13/2008/QH12 on Value Added Tax provide:

“Article 3. Taxable objects

Goods and services used for production, trading or consumption in Viet Nam are subject to value added tax, except those specified in Article 5 of this Law.

Article 4. Taxpayers

Taxpayers include organizations and individuals producing or trading in goods or services subject to value added tax (below referred to as business establishments) and organizations and individuals importing goods subject to value added tax (below referred to as importers)”.

Item b, Clause 1, Article 2 of the Law on Enterprise Income Tax provides:

“Article 2. Taxpayers

1. Taxpayers are goods and service production and trading organizations which have taxable incomes under the provisions of this Law (below referred to as enterprises), including:

….

b/ Enterprises established under foreign laws (below referred to as foreign enterprises) with or without Vietnam-based permanent establishments in Viet Nam”.

Point 1.4, Part A of the Ministry of Finance’s Circular No. 14/2008/QH12 Nghị định 124/2008/NĐ-CP">130/2008/TT-BTC of December 26, 2008 also provides enterprises established under foreign laws with Vietnam-based permanent establishments in Viet Nam.

Point 1, Section I of the Ministry of Finance’s Circular No. 134/2008/TT-BTC of December 31, 2008 provides:

“1. Application of this Circular

The guidance under this Circular is applicable to the following subjects (other than those specified in Section II, Part A of this Circular):

- Foreign businesses with or without Vietnam-based permanent establishments in Viet Nam; and resident or non-resident foreign businessmen doing business in Viet Nam or earning incomes in Viet Nam under contracts, agreements or commitments between them and Vietnamese organizations and individuals (below collectively referred to as foreign contractors).

- Foreign businesses with or without Vietnam-based permanent establishments in Viet Nam; and resident or non-resident foreign businessmen doing business in Viet Nam or earning incomes in Viet Nam under contracts, agreements or commitments between them and foreign contractors to perform part of contractor agreements (below collectively referred to as foreign subcontractors)”.

The above provisions are applicable to the case of Emerging Market Solutions International Inc (EMSI Company), a foreign business, which signed in 2007, the contract on provision of equipment and services for lottery system to Capital Lottery State Single-Member Limited Liability Company (Capital Lottery Company). In May 2011, EMSI Company transferred the contract and the whole related assets to Cai Sheng Holding Limited Company (Cai Sheng Company), a foreign business. The tax obligation toward this transfer shall be determined as follows:

- In case EMSI Company is a foreign business without Vietnam-based permanent establishment in Viet Nam under regulations, the transfer is not liable to enterprise income tax and value added tax.

- In case EMSI Company is a foreign business with Vietnam-based permanent establishment in Viet Nam under regulations and the contract performance is attached to such permanent establishment, EMSI Company is obliged to pay enterprise income tax and value added tax under current regulations.

Above is the reply of the General Department of Taxation to the Hanoi Tax Department for examination and specific handling in conformity with reality and legal regulations.

|

|

FOR THE GENERAL DIRECTOR |